This post was first published in February 2020 and updated in March 2021

Are you looking for advice on how to build wealth in your 30s?

Not too long ago, I updated the blueprint on how to build wealth in your 20s.

When I first wrote that post, it was partially intended as a letter to my younger self, outlining all the things I wish someone told me 15 20 or so years ago.

Your twenties are the perfect time for exploration, growth, and calculated risks.

The way I look at it, you are about to get on to the highway of life and gear up for a long and rewarding journey.

But you still have the option of making a U-turn, heading to the airport, and jumping on a supersonic jet instead.

Once you’ve hit your thirties, that opportunity is probably gone. You are now firmly on the highway.

And while it might be too late to get off, that doesn’t mean you can’t switch your Honda Civic for a Ducati, rev up the engine – and fast forward to the life you are dreaming of.

You, riding this baby all the way to FI!

Some of the points below should be no-brainers – and you may well be doing them already.

In that case, feel free to give yourself a big pat on the back.

Some others, however, might not even be on your radar (and yes, you’ll have to read on to see what I mean).

How To Build Wealth In Your 30s In Five Simple Steps:

#1: Develop A Career Strategy

Some of us get lucky and find meaningful, rewarding careers early on. Most people (myself included) don’t.

So if you chose a field of study or a profession you ended up disliking, your 30s are the time to be honest with yourself – and act quickly.

If you are just starting out the decade, there is still time to go back to school and pursue an advanced degree in order to re-invent yourself.

I graduated from my MBA program when I was 31. At the time, some people told me it’s too late to make a career change.

At times, I’ve felt that way as well.

But with the benefit of hindsight, it turned out to be one of the best decisions I’ve ever made.

If you are past your early 30s and still want to change your career trajectory, going back to school full time is probably no longer the best option.

Instead, you may want to consider a part-time degree or specialized courses/certifications that will help you augment your skill set and allow you to accelerate your career progression.

Quite often, employers will help you along the way by moving you to a different department or giving you a different role.

Such lateral moves can serve as a great launchpad for moving into a different industry or function.

But whatever you do, please make sure the program you are considering does what it says on the tin.

Very often, advanced degrees are just high-margin products for institutions that offer them.

Your money, effort, and time are better off spent elsewhere.

#2: Focus On Family

Unlike many other things in life, this one is at least partially outside of your control.

No one knows when they will meet that special person – or if that will ever happen.

Many people go through life in happy solitude while others prefer having someone to share the inevitable ups and downs.

If you happen to be in the latter camp and think settling down with that special someone is on the cards, you’ve got two key things to consider.

Firstly, make sure that you and your partner are fully aligned on financial matters.

You don’t need to see eye to eye on everything, but you need to make sure you’ve got the right ground rules that will help you prosper as a family.

Secondly, have a plan regarding children.

Whether you will have them, how many you would like to have, and what is your ideal setup once you have them.

Do you want to continue living centrally? Move out to the suburbs? Does one person want to stay at home?

Do you want to send them to private schools or will a state education do just fine?

The biggest reason you need to have a plan for children

Raising children can be one of the most expensive (and exhausting) endeavors you will ever undertake.

But if you have a solid plan, financial independence and children are not mutually exclusive.

Just make sure you develop that plan before you actually have children.

For most people, the first few years of childrearing is basically a misty fog of endless running around while being severely deprived of sleep.

It’s tough to make rational decisions in that state of mind.

#3: Get On The Housing Ladder

If you haven’t yet, your thirties are the time to get on the housing ladder.

It doesn’t matter whether it’s the cheapest place in town and you need five roommates to help you pay the mortgage.

It’s going to be hard. You’ll need to scrimp and save and borrow and maybe even take a part-time job.

But it’s a must.

If you are going to build serious wealth, real estate will play a big role and this first property is the cornerstone of your future empire.

Make sure to google “house hacking” – there are plenty of great resources out there to help guide you.

Remember – you don’t need to live in your ideal family home before you have kids.

While they are small, a one- or a two-bedroom place will do.

Instead of looking to upgrade at the same time as you have a new addition to your family, try to build as much equity in your home as possible.

Ideally, you keep your first place and use it as a rental property when you buy a bigger home.

#4: Start Investing

In addition to real estate, stock market investments account for the other cornerstone of your financial strategy.

This is why:

If you are in the UK, your employer is required to enroll you in the workplace pension scheme – and to kick in 3% of your salary.

If you happen to be self-employed, you need to open up a self-invested pension plan.

You won’t get the employer match (which doesn’t really matter, as you ARE the employer) but you will still get the tax break from the government.

Then there’s the Lifetime ISA. This is essentially free money from the government, and you can only open up an account until you are 39.

You snooze, you lose – so get on with it (but keep in mind that in most cases, a workplace pension will give your money more oomph).

As with many things in life, the most important thing is to start investing, even if the amounts themselves are trivial.

Once you’ve got the habit in place, you can use a nifty mind trick called save more tomorrow to increase your contributions as your pay goes up.

Most importantly, remember – your pension and Lifetime ISA are just investment vehicles, not investments themselves.

Think of them as envelopes. You can use them to hold anything you want – cash, gold, stocks.

But of course, nothing will ever beat the good old low-cost, well-diversified index tracker.

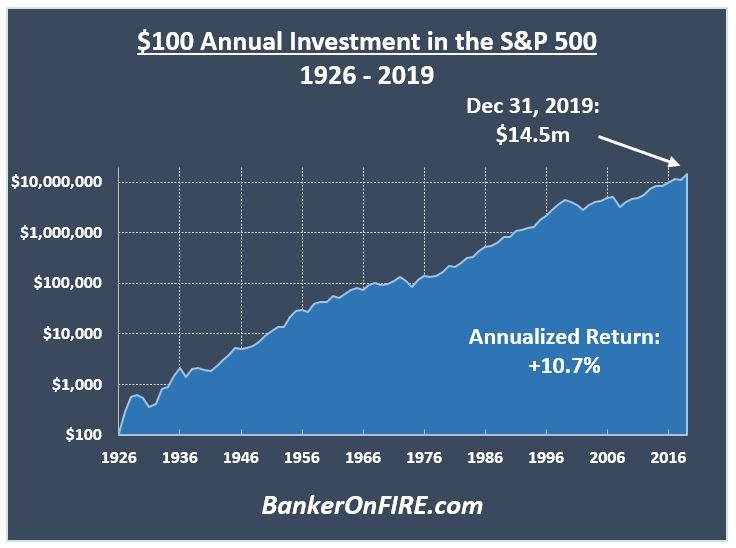

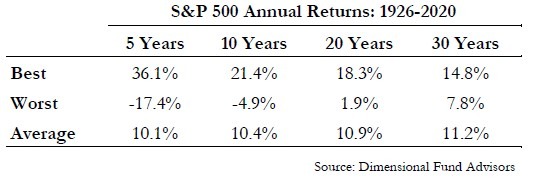

Worried about investing in the stock market? Then please do yourself a favour and read this – or just stare at the chart below:

#5: Build Your Network

This is the bit that I think is missing from most, if not all articles on building wealth out there.

And yet, it might be the most important.

As you enter your thirties, your personal and professional network begins to shrink.

Life gets busy. People move around. High school and university buddies fade into the background.

You don’t keep up with former colleagues as much as you used to.

And now that you have family commitments of your own, you probably don’t spend as much time socializing and getting to know people at work.

In the long run, this will cost you dearly.

Like it or not, but life is a team sport. You won’t be successful trying to make it on your own.

Whether it’s advice, support in tough times, help in finding a job, or debating that bright idea you have, having a group of people to lean on will be your trump card.

NOT the way to go about it…

The best way to establish that group of people is by being helpful to others – a.k.a. creating something from nothing.

Helping a colleague who is getting downsized line up a lateral move or a new job.

Being there for your friends who are going through tough times.

Supporting that brave person in your circle of contacts who quit her job to start a business.

Mentoring a university graduate who joined your department and is still finding his feet.

In fact, helping others is the most underrated component of happiness.

It also happens to be a crucial component of your success.

And unfortunately, far too many people miss a beat on this one, much to their own detriment.

So whatever you do in your thirties, don’t forget to keep an open mind and an open heart.

Your life will be so much better – and your success so much greater.

Thank you for reading!

PS: Not in your 30s anymore? No, you are not too old to build wealth.

Here are some thoughts on how to build wealth in your 40s.

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

At 30-ish years old, this article speaks to me! Your first point is especially timely; I’ve been working in my field for 8-9 years, and I think it’s time for a change. I’m trying to do what I can to formulate a career strategy and figure out what I want to do for the next 10-20 years. Going back to university full-time is definitely not an option, but I may end up taking advantage of online courses.

That’s a very sensible approach. The biggest problem with going back to school full time is that even if everything works out career-wise post-graduation, the significant monetary + opportunity cost means you end up working much longer.

It’s fine if you really love what you do, but going back to school or re-training part-time can be a much better option.

I hope I reap the benefit of being a broke part-time graduate student reluctant to get a job in the field I left lol

Somebody recently suggested I read a book called “So good they can’t ignore you”. It’s a careers book but I think not just for those either looking for change or just starting out, but also those of us who have been in a career for a long period of time.

I’m just at the tail end of the book now. I have no intention at all to change my career path as I still get a kick out of what I do 18 years later (have of my life has been spent doing what I do).

However, there are some great sections in that book that resonated with me and may also with you.

Many thanks for the recommendation. Have checked the reviews and it looks very interesting.

On the reading list now 🙂

I’ll second the recommendation. “Deep Work” by the same author, Cal Newport, is also very good

Hi, nice article. We are in the position where we’ve outgrown our current property and are looking to size up, but a big problem with living in Scotland like we do is that the devolved parliament have set putative stamp duty rates for buying a second property. This effectively removes the option of keeping our first property as a rental, which is a real shame.

That is a shame indeed.

I’ve always wondered, any way to buy the property in just your or your partner’s name? Is that a realistic workaround at all?

I’m not sure, unfortunately (or fortunately really, but unfortunate in this particular circumstance), my wife already has an inherited property in her name in the South East and the flat we live in is under my name.

So there isn’t a work around and we may even make a loss on my flat. Outside of the South East and other areas of “guaranteed” increasing population buying can often be a gamble and not always the right move with hindsight. Luckily we’ve been hitting our ISAs and my pension pretty hard so have other assets that are doing well.

Got it. Interesting about the loss – is that after you consider mortgage paydown as well?

In my experience, it takes a meaningful price decline to actually crystallize an equity loss given you are paying roughly 2-3% of your mortgage principal per year.

The real challenge is the transaction fees, which is why I absolutely HATE selling real estate.

Yes including everything: mortgage paydown, interest (essentially rent), not paying rent to live in an equivalent property for the same amount of time, insurance and transaction fees either end; our break even price is £21,500 less than I payed for the property. Equivalent properties are going for a bit less than that. Also that’s in nominal terms I’ve not calculated the break even in real terms as it would be too depressing.

Great article bof. The only thing I’d say is I think you can reinvent yourself at any age though accept its probably harder after 30. I’m currently studying for exams to be an ifa at age 40.

The only potential benefit I can see in starting at my age is I’ve got huge bandwidth to take risks and change careers that I simply wouldn’t have had even 5 years ago

Hadn’t realized you pulled the trigger on the IFA. Congrats!

You are right – there are silver linings to everything. That being said, I’d venture to say that becoming an IFA is not (entirely) a financial decision for you, is it? Given where you are in terms of savings and investments.

Really appreciate the focus on the last one – also worth saying that going into your 30s and having a family you’ll be less willing to have whole weeks to prepare for interviews (if you’re in a career like Software where the preparation required is ridiculous), so a network will be very important.

I’m a bit surprised about the “getting on the housing ladder” part given that you’re renting your own place IIRC.

Yes, well-spotted regarding our primary residence.

We still practice what we preach, being massively long real estate. That being said, there are specific reasons for renting at the moment. Too long for a comment but I’ve laid them out in one of the previous posts:

https://bankeronfire.com/buy-or-rent

Spot on advice about networking. Definitely course the last six years I had my head down and was focussed on running my business.

I also did focus on getting to know folks better who I wanted to build better relationships with, but this was also perhaps at the detriment of my entire network.

So during my accidental retirement I’ve been spending the time trying to touch base with folks who I haven’t spoken with in quite a while.

Anyways, for anyone currently in the midst of a lot of life changes try to keep this in mind. Take some time to keep in touch with folks in your network.

I really like the networking part you wrote.

However, I am not certain that it will always result in favour being paid back.

Personally I have seen too many ungrateful people that I stop being helpful. I want to build a network of people who help each other too but i just seem to have such a bad luck of doing so, the ones coming to me for help tend to disappear afterwards.

Have you ever experienced this and what would you do?

Happens to me all the time.

I find that the 80-20 rule applies here. I.e. only 20% of folks you help will help you back – but the impact of that help can make all the difference in the world.

What you should also consider is that while people might not reciprocate with you, they could well go on and help others. I’ve had multiple individuals who helped me along the way and I wasn’t able to reciprocate.

However, their efforts weren’t wasted as I, in turn, helped many others down the road.

So while it makes sense to cut off the obvious freeloaders, I wouldn’t skimp on paying it forward.

Great article BOF.

The importance of networking cannot be overstated. In my line of work people hire on the strength of reputation and recommendation all the time. I’d say after competence, maintaining your network is one of the most important aspect to both new employment and promotion. I don’t think there’s ever an age where this isn’t true but I think that your 30’s is often the first time most of us can really benefit from the power of it.

I know you touched on this in other articles but I’d add to the list the power of market knowledge i.e. where you and your current employer stand in terms of training, benefits and pay compared to others within your industry. Importantly also people which may sit just outside your industry but possible share relevant skills. Who is hiring at what rates etc etc is invaluable.

Thanks Rosario.

I used to work for a team that (for reasons outside of our control) basically disintegrated in a period of 24 months.

At the time, all of us had to be very nimble to line up other gigs, ultimately scattering around 5+ different organizations.

It was a short-term loss for all of us, but the long-term gain from having a network of trusted contacts at each of those 5+ banks has paid incredible dividends in the years that passed. You simply can’t underestimate the ability to understand what’s going on in the broader marketplace.

Interesting considering my current dilemma. I’m 37 and have worked in the utilities industry for 12 years until being put at risk of redundancy January 2020. I managed to secure alternative employment in my multinational corporation but it was in a completely new industry.

My package is fantastic, £60k salary including my car allowance, 10% employer pension contribution, Salary sacrifice up to 45% of your pay (I max this so with the employer contribution £30k is being saved annually), monthly share investment plan with 1 free for every 3 purchased, annual share incentive plan (max £1800) with 50% discount due to same company matching and additional taken from gross pay. The company pays my car insurance also.

The problem is i’ve gone from heading up my own department with two teams in an industry where my gained knowledge adds value to what is essentially extremely expensive admin support with no management responsibilities or understanding of the industry to add value. Couple that with Covid meaning i haven’t met any of my colleagues to learn via interaction. I’m between a rock and a hard place. I’m aware my development and recent skills and experience will stagnate/diminish in my current role, but also cant match my current package by a long shot with other companies (I am looking). Part of me thinks, ride it out whilst its available, but then worries about the future should the job be lost. If I was at the start of my 30’s it would be a no brainer to leave and take a pay cut, but saying that there is still at least 15 years of work life ahead (planning on saving enough to go part time in any job I like in my early 50’s). It feels im too far along to take the big hit and give up the sweet rewards (golden handcuffs) but also not far along enough to risk riding it out.

I guess the question here is: how sustainable is your current role?

Is the job “safe” (as much as any corporate job can be) and does it take you into retirement in 10-15 years?

Or are you at risk of being made redundant again (once someone picks up on the “extremely expensive admin support” point) at which point you need to look for a job again?

If it’s the latter, I think the answer might well be to bite the bullet now and reposition before your skills go stale.

If it’s the former, riding it out might not be a bad strategy.

Pingback: How To Build Wealth In Your 20s: Updated For 2022 - Banker on FIRE