When it comes to stock market investing, do you ever feel like the people in the picture above?

Chances are, you do. After all, the fear of losing money is the #1 reason so many people remain on the sidelines.

As a result, we are now more than a decade into the most-hated bull market in history.

Scarred by the Great Recession, a record number of retail investors continues to be underweight (or zero-weight) equities.

In the meantime, economic progress marches on, productivity keeps increasing, corporate earnings go up and guess what? Share prices follow.

In other words, this happens:

Ahh, if only we hadn’t been so damn scared of losing our money back in 2008. Or 2001. Or 1995…

Of course, there is no need to blame yourself for being scared of losing money.

However, what might be helpful is a slight reframing of the argument. Instead of asking the question “Am I wrong to be scared of losing money?” (hint: you are not), let’s ask ourselves a different question today:

“What is the likelihood of losing money in the stock market?”

To answer that question, we are going to analyze historical stock market returns for the past 93 years.

For those of you who are impatient and just want to get the answer, here are the key findings based on historical data:

- Making a lump sum investment into the S&P 500 and holding on for 10 years lost money less than 5% of time

- At the same time, there was a 25% likelihood that the strategy above would yield an annualized return of 15% or more

- The odds get even better when you replace lump sum stock market investing with regular contributions

- If you increase the time horizon to 15 years, investing in the S&P has never led to a loss of principal

Want to know more? Let’s dive in then – but we need to get two simple concepts out of the way first:

Concept #1: Properly Gauging Historical Stock Market Returns

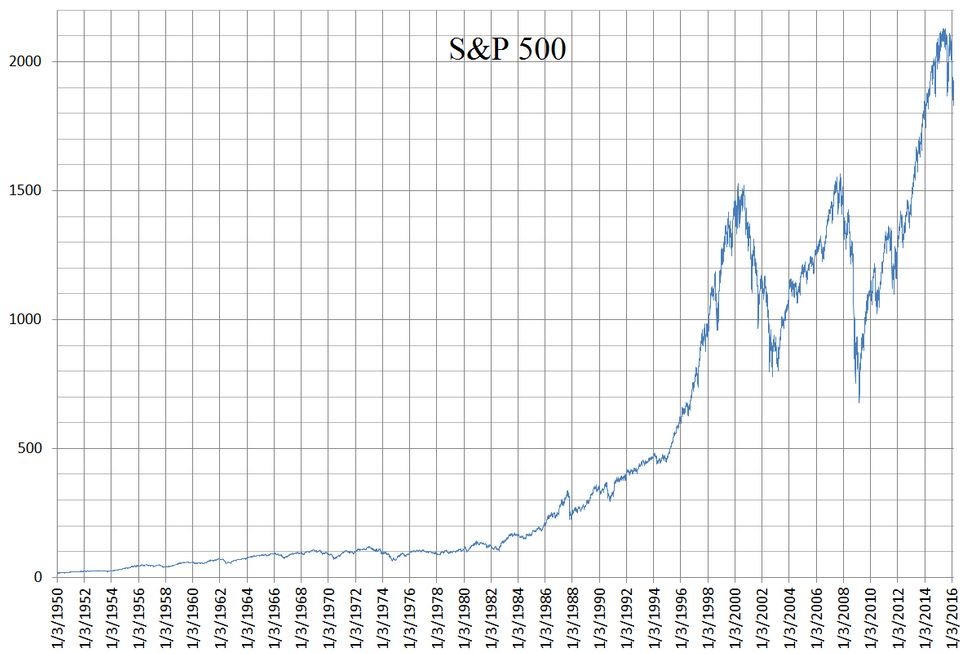

Part of the problem with using charts like the one above is that they don’t accurately represent returns achieved at the beginning of the time period.

For example, the chart above gives off the impression that the S&P hasn’t really gone anywhere between 1985 and 1995.

This, of course, isn’t true. In January 1985, the S&P stood at about 170. By January 1995, it was at about 460, a 2.7x increase (excluding dividends – more on that below).

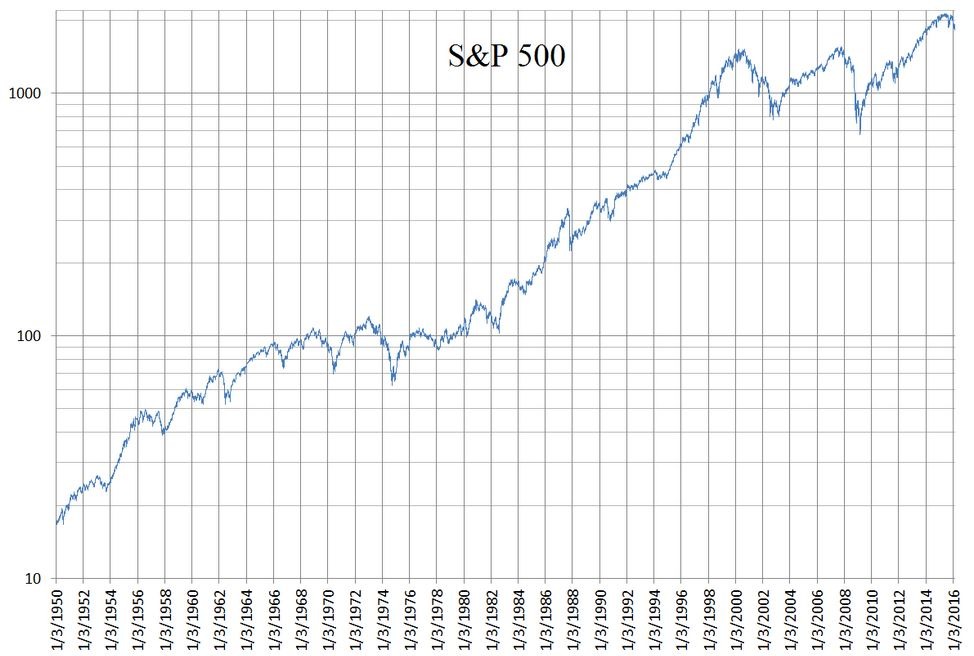

For a more appropriate visual representation of returns over long time horizons, its better to use log scale charts, as evidenced below.

Linear chart – can’t really see what was going on in the past:

Log chart – I can see clearly now the rain is gone stock market has gone up:

Please don’t let the mathematical name confuse you. Simply put, “log” refers to the way the scaling is adjusted in the chart above. That’s all.

Concept #2: Price Return versus Total Shareholder Return (TSR)

This one is very important so please pay attention.

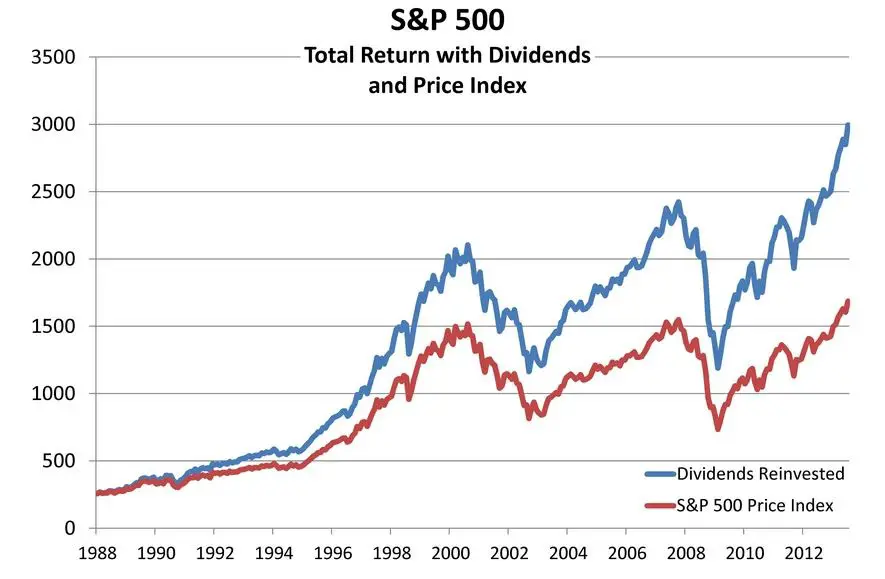

The biggest mistake retail investors make when it comes to stock market investing is comparing the headline index numbers.

“Hey, the S&P was at about 1,500 in 2000 and back at 1,500 in 2008. That means stock market investors didn’t make any money!”

Right? WRONG

The logic above excludes dividends paid by the S&P constituents in the meantime. If those dividends were reinvested into the stock market, the picture would be very different.

Take a look at the chart below for illustration:

Note: You will notice that I am using the S&P 500 as a representative stock market index. When it comes to other indexes, individual performance may differ but all of the concepts still apply. In either event, if you are new to stock market investing you would be well advised to stick to the S&P 500 or a global index tracker.

Now – back to the exam question.

Will I Lose Money Investing In The Stock Market?

Thanks to some helpful folks over at Slickcharts, we are able to access historical S&P 500 return data for the past 93 years.

As mentioned above, this is total return data – i.e. it captures both price and dividend returns over the 93 year time horizon.

Let’s now take a trip back in time and analyze the probability of losing money under one of the typical stock market investing scenarios:

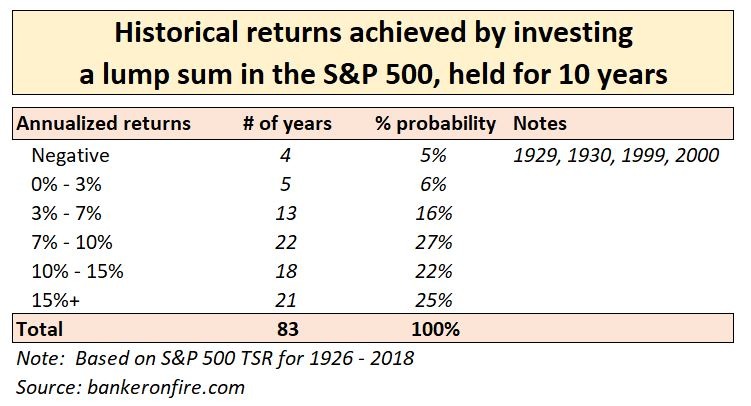

Scenario #1: Make a lump sum investment into the S&P 500, hold for 10 years

Let’s say we had $10k to invest. Let’s also assume we were smart patient enough to keep that money invested in the stock market for ten years before withdrawing it.

Guess what? In the eighty-three years since 1926 (because the last time you could make a ten-year investment and see how it pans out is 2009), we would only lose money four times.

In other words, the probability of losing money when investing a lump sum in the S&P and staying invested for ten years is only 5%.

Not only that, but the biggest loss we would bear is 1.4% (annualized). Incidentally, this would have happened had we made the investment back in 1999, shortly before the dot-com bubble.

Now don’t get me wrong. Losing money hurts. Your $10k would shrink to $8,685 at the end of the ten-year period, which is a ~13% total reduction.

Then there’s the forgone opportunity cost of having that $10k invested in a low-risk, low-return instrument.

But are we talking about a catastrophic, we are off to the poorhouse kind of loss? Certainly not.

The other three years in which our investment would have yielded negative returns are:

2000: -1.0%

1929: -0.9%

1930: -0.1%

Now let’s look at what happened the other 95% of the time:

The chart above is striking for a number of reasons.

First of all, it shows that in five out of 93 years, we would have realized below-inflation returns of less than 3%. That’s a 6% likelihood.

The reason that’s important is because not keeping up with inflation implies a loss of principal in real terms.

However, what it also means is that investing in the S&P would only lead to nominal or real losses 11% of the time.

In other words, there was an 89% probability of making a positive real return on your stock market investment.

And while making less than 7% annualized is nothing to write home about, generating a 15%+ return a quarter of the time is nothing short of a home run.

Let that sink in. You make a one-time investment in the stock market. You let it sit there for 10 years. You have a 25% chance of making an annualized return of 15% or more.

But it gets better still.

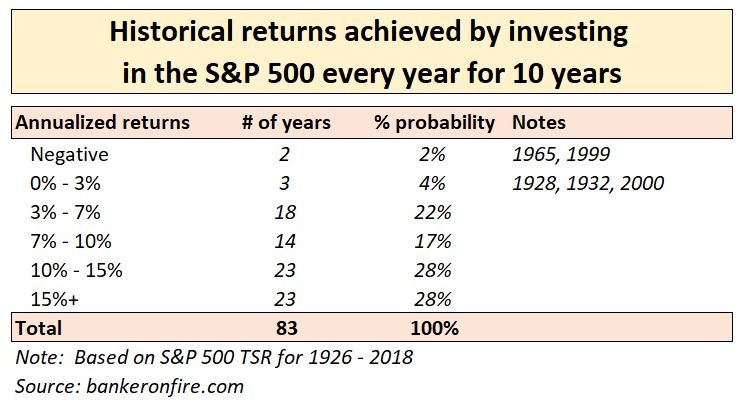

Scenario #2: Invest in the S&P 500 every year for 10 years

Assume you are one of those weird people with a habit of spending less than you make, which leaves you with excess savings every single year.

What if you were to invest those savings in the S&P every year, for 10 years straight?

Guess what? The probability of losing money, whether in nominal or real terms, is now down to 6%.

The probability of realizing an annualized return of 7% or more is 72%.

Still salivating over those 15%+ returns? Well, there was a 28% likelihood of hitting that home run.

Want to go even further down the rabbit hole?

Because I had the data sitting there in my spreadsheet, I decided to extend the time horizon to 15 years and see what that does to the returns.

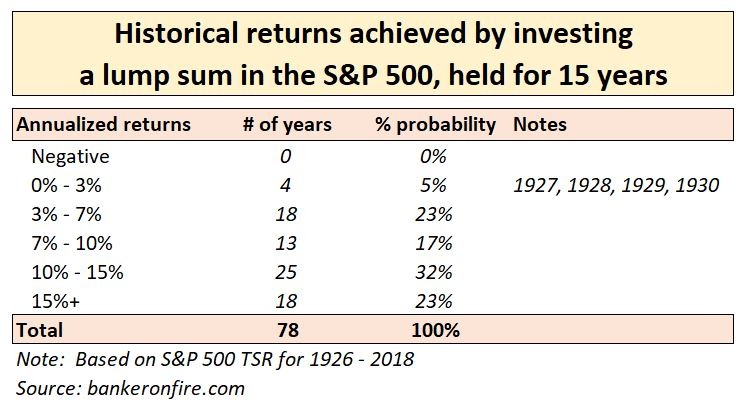

Scenario #3: Make a lump sum investment into the S&P 500, hold for 15 years

Here we go:

Yes, you read that right. This strategy had a zero probability of losing money in nominal terms and only a 5% probability of losing money in real terms.

And at the top end of the distribution, there’s hardly any change to the likelihood of returns of 7% or more.

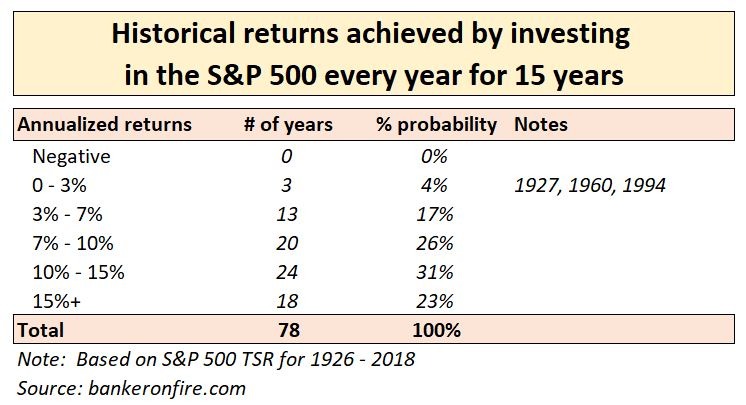

Scenario #4: Invest in the S&P 500 every year for 15 years

Once again, the probability of losing money in nominal terms? Zero. In real terms? Only 4%.

Instead, there was a 79% probability of realizing an annualized return of 7% or more.

No expensive financial advisors needed. No complicated strategies (which are only complicated to confuse you and make money for the advisors). Just a regular direct debit into your low-cost brokerage account.

Does Stock Market Investing Still Scare You?

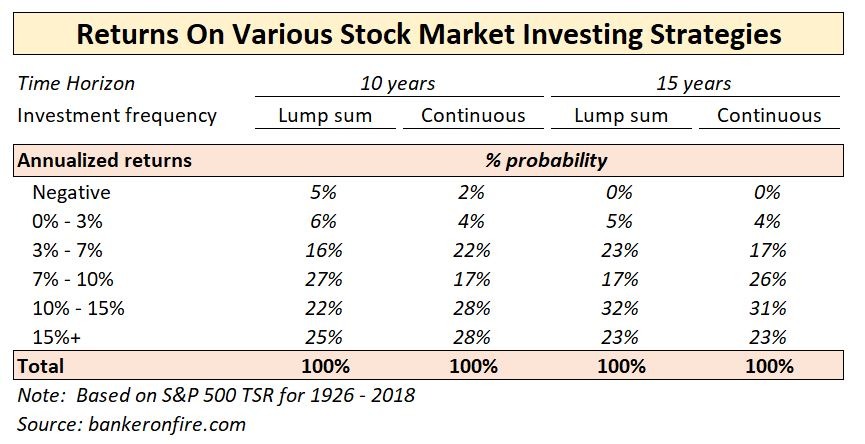

For convenience, let’s recap the findings in a summary table below.

Now, repeat after me:

If you have a time horizon of 10+ years and invest in a passive S&P 500 index tracker, the probability of losing money is extremely low

So low, in fact, that it would take something very stupid to actually lose money. Like not having a long term investing horizon. Like actively trading. Or like using a financial advisor.

Yes, But…

Yes, the past does not predict the future. Yes, we had an astounding bull run in the stock market.

Yes, everyone keeps saying the stock market is about to crash. Including this guy:

Yes, Trump, Brexit, trade wars, China, Russia, Iran, etc etc etc.

I get all that.

Of course, there’s a non-zero probability of a material correction in the stock market at some point. As a matter of fact, it’s pretty much a certainty.

You know what else is a certainty?

If you sit on your cash, inflation will eat away the purchasing power of your money. That’s a certainty.

If you try to time the market, you will fail. That’s a certainty.

If you place your money with an active money manager, they will underperform their benchmark index over the long run. That’s a certainty.

So let me leave you with my favourite quote from Warren Buffett:

“Someone is sitting in the shade today because someone planted a tree a long time ago”

Happy investing my friends.

And if you have relatives or friends who are afraid of losing money in the stock market, please do them a favour and send them this article.

Readers, are any of you scared of losing money in the stock market? Does anyone feel like they’ve been sitting on the sidelines for too long? I would love to hear from you in the comments below!

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

Great post! The best thing to do is to invest and go to sleep… best to hybernate. Then, one fine day, wake up a wealthy individual! Most people are so herd-driven, all they do is focus on 24/7 market coverage on CNBC and take action ALL THE TIME.

Thanks Matt. One of the reasons I wrote this post is because I wanted to have hard evidence next time I hear a “but you can lose money” argument. Glad you liked it.

As you say, stock market investing has got to be the one area of our lives where taking action all the time is actually counterproductive.