Note: This post was first published in June 2020 and updated in January 2022

In the past, I’ve published posts on the best ways to build wealth in your twenties as well as your thirties.

Much as we hate to admit it, there will come a time when our glorious twenties and happy thirties will be well behind us.

Yours truly is a case in point.

If you are fortunate enough to have focused on personal finance matters early on, you may be entering the next decade with a sense of optimism and self-satisfaction.

For others, it may be an overwhelming desire to reach back through time and punch your younger self in the face.

Why-or-why didn’t we make the right decisions back then?

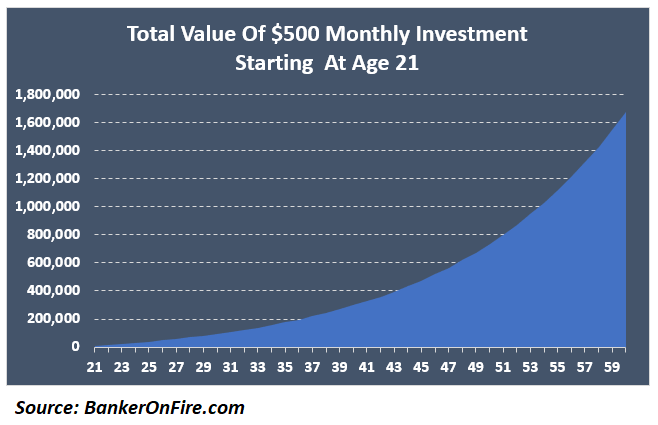

Oh, just how helpful it would have been to have the benefit of two decades’ worth of saving and compounding.

In other words, this:

Thankfully for your twenty-year-old self, time travel hasn’t yet been invented.

Which is just as well. Because if you don’t start building wealth right now, your sixty-year-old self is going to pull out all stops, and actually find a way to go back and give you the bollocking of your life.

Silver Linings

The good news about being in your forties is that while you might be late getting off the start line, there are advantages too.

You are probably further along in your career – with an increase in earnings to boot.

By now, your kids may well be out of those eyewateringly expensive early years, what with the daycare and everything.

And while some people will unfortunately start their forties with high levels of debt, many others will have accumulated some assets already.

Perhaps some equity in your house. A bit of a nest egg in your workplace pensions or 401(k) plans.

Most importantly, one would hope that by your forties, you will have developed enough self-esteem to stop caring about keeping up with the Joneses.

If you have a clear sense of your true priorities in life, building wealth becomes a much easier exercise.

Let’s get on with it:

1. Get Up To Speed On The Basics

Just because your younger years are behind you does not mean you get a pass on personal finance basics.

So start by learning everything you can about personal finance. Re-evaluate every single one of your expenses. Prioritize investments.

Most importantly, stay healthy. Early on in life, you can get away with just about any self-destructive habit. Not anymore.

Remember – an investment in yourself is the best kind of investment you could possibly make. Without it, your wealth-building journey is doomed from the start.

2. Get Rid Of Your Debt

Just do it. No ifs and buts (unless it’s mortgage debt, in which case see below).

Yes, you could really use that holiday. And it would sure feel nice to indulge in your hobbies.

But if you are using debt for any kind of non-essential spending, you are just putting on a nice pair of cement shoes.

That sixty-something version of yourself? He or she doesn’t care about a holiday. No, they just want to have the option of retiring in a comfortable and dignified way.

And if you don’t give it to them, they might just whip out the brass knuckle.

So do whatever it takes. Pay it off. Get on with life.

3. Focus On Deferred Savings Vehicles

Let’s face it – if you are just starting out, retiring early may well be out of the question. But that’s not necessarily a bad thing, as it can actually simplify the task at hand.

Here in the UK, one of the biggest issues presented by early retirement is figuring out how to allocate investments between your pension and your ISA.

Thankfully, that’s not something you have to worry about. Now is the time to go full throttle on your workplace pensions – and get the wonderful employer matching and tax breaks.

If you happen to be in a higher tax bracket by now, that helps juice your returns even more.

What also should help is the fact that retirement is actually not that far away. Many younger people dismiss workplace pensions / 401(k) plans because they don’t feel comfortable locking up the money for such a long period of time.

Well, you no longer have that problem.

With retirement just a decade or two away, there’s no reason not to pile into whatever deferred savings vehicle that may be on offer.

In other words, give them all the love free money can buy.

4. Stock Market Is Still Key – But Don’t Forget Bonds

It might not seem like you’ve got a lot of runway, but you do.

With retirement still a decade or two away, you simply can’t afford to miss out on the compounding superpower of the stock market.

That being said, perhaps there’s a place in your portfolio for a sprinkling of bonds.

Yes, they do eat into your returns. But in return, they provide a cushion against near-term volatility, reducing the likelihood of you doing something silly – and losing even more money along the way.

If the market selloff over the past few weeks has had you reaching for the “SELL” button, remember this – it’s much better to sacrifice a few points of long-term returns than to panic, sell in a correction, and crystallize a loss.

And as you gear up for actual retirement, having a portion of your investments in bonds can ensure you get to dictate the timetable, not the stock market.

So read up on investing in bonds. They are guaranteed to be a good, reliable friend on the journey.

5. Focus On Longevity Of Work

It can be appealing to try and do everything you can to shorten the time to retirement.

Unfortunately, the numbers don’t lie. Getting from zero to hero (where hero means leaving your job behind) in 10 years is a tall ask. It requires diligence, discipline, and a pretty punchy savings rate.

Doing so in 20 years is much, much easier – and enjoyable.

So as you plan your career going forward, you may well be better off in lower-pay, lower-impact jobs.

Much better to do something enjoyable for 20 years than to spend the next 15 hating your boss – and your life.

6. Mind Your Mortgage

For most people (myself included), retiring with a mortgage can be the biggest anathema of them all.

It simply doesn’t feel right. And so the temptation may be to channel every free pound / dollar / euro into repaying your mortgage ASAP.

Unfortunately, this strategy can often be highly counterproductive, especially in today’s world of ultra-low interest rates.

One of the first posts I wrote on this blog was on this very topic.

I’ve also subsequently written a post on some advanced considerations regarding early mortgage repayment.

Sure, there are advantages to clearing your mortgage. But if you are starting out late, you really need to consider all the pros and cons.

You may well be better off investing all the extra cash – and downsizing to a fully paid-off house at some point.

There’s also the option of using the equity in your home to buy a place in a lower-cost location (Spain or Costa Rica, anyone?).

As nice as it feels to have a fully paid off home, you don’t want it to be the only asset in your name. That sixty-year-old version of yourself will not be happy.

Happy… Beginnings?

Starting your journey to financial independence in your forties can feel like a tall ask. In many ways, it is.

But make no mistake: it’s not too late.

You still have plenty of time to move the dial in your career.

To take chances in and outside of work. To try and fail – until you finally succeed.

Time is still your friend. You’ve got decades and decades of runway to let compound interest work its magic.

You are no longer shackled by unhelpful preconceptions you may have held earlier in life. You know where your priorities lie – and what it will take to achieve them.

Most importantly – you are not alone. Plenty of people have walked this path before – with amazing outcomes.

And plenty of others (at least in the personal finance blogosphere) are there to help support you along the way.

So press on the gas – and enjoy the journey!

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

Nice, finally a post for me (45y, learned about FIRE early this year, planning now to RE in 10 years, after having done my imaginary face-punching to my past self thoroughly ) 🙂

I struggle a bit with putting my money in bonds though, because of the expected lower returns that would derail my 10-year-plan. I understand this makes sense if a stock crash would make me panic-sell and/or I need to start RE at a fixed date even if the stock market is low. But what if it does not really matter that much for me if I actually retire after exactly 10 years of saving or postpone this for 2 or 3 years if needed. Usually after stock market crashes, the market bounces back after some years, right? Would you still use bonds?

Glad to hear it hit the spot!

You are right, to the extent you have flexibility on the timing of retirement and are confident you won’t panic sell in a period of volatility, equities represent a much better option.

Also, the point most people miss is that equities have a very meaningful role to play in your portfolio even after retirement. After all, retiring at 55 leaves most people with another 30 odd years of time. That’s an awfully long time to be missing out on stock market gains.

Really pleased to see a FIRE article aimed at the over 40’s. Last year i finally took an interest into pensions and how to get to FIRE (after years of seeing pension statements land on the mat and feeling depressed at the suggested annuity values). I thought i had to work until i was 68 (state retirement age) and that was that.

Thankfully over the years we didn’t let lifestyle creep set in and combined this with a relatively good savings ethos. Investing was the probably main piece that had been neglected. More luck than judgement but thankfully have been paying into pensions for the past 25 years and now feel i have more control of the situation (aim is to retire in 10 years but utilize stock market gains for hopefully the next 40).

I’m surprised however at the number of friends (many in well paid employment) who have no interest in how they will reach a point at which they will no longer need to work or avoiding even avoiding lifestyle creep.

Keep up the good writing.

I think the mandatory conversion to annuities did more to discourage people from contributing pensions than anything else. Nothing more demotivating than staring at the equivalent of a sub-2% SWR rate…

By the way, I’ve got plenty of colleagues who don’t even know what their pension balance is – or how it’s invested. Always perplexed me as well, particularly as some of these colleagues don’t look too excited by their jobs.

Hi @Tommi

Similar to me, I didn’t discover FIRE until I was 44 and in an attempt to try to ‘catch up’ on my lost years, I was initially 100% in stocks.

Six years later, I now have just under 30% in bonds, which has done well to balance out some of the volatility experienced recently and which has provided me with some comfort (and not led to any panic!).

I think it’s what you’re comfortable with – balancing risk (and possibly higher growth) with stability (and possibly lower growth).

I think I’ll be happy with the 30% going into retirement at 55, maybe shift it to 40% when I get older and seek more stability.

Weenie, if you don’t mind me asking – which bond investment vehicle do you use?

Hi BoF

By ‘bonds’, I mean Bond ETFs, mostly VGOV but also VUCP and these I just buy via my usual providers (AJ Bell and Freetrade). Oh, I also have a bit in Vanguard UK Long Duration Gilt Index in my HL account.

I don’t hold any actual bonds, apologies for any confusion.

No, that’s exactly what I meant by “vehicle”. Thanks Weenie.

I think in point two you meant to say: But if you are using debt for any kind of DISCRETIONARY spending

Ahh, the perils of proofreading your own posts…

Thank you for highlighting – have fixed now.

Great post BoF. And a shout out to the tables you produce. I appreciate how much time goes into them to make them so intuitive

Thank you sir, appreciate the kind words. Got to put those modeling skills to good use I guess 🙂

PS: I finally have a blogroll page – hope you don’t mind the inclusion. Look forward to reading your next piece!

Wow – thank you for including us and even more for the very kind words. I’m blushing, or possibly sunburnt…. But seriously, thank you

You clearly dont need it, but if you want an interesting read on presenting data in tables, graphs, etc, then Jon Moon’s book Clarity and Impact is worth a read. Goes beyond just how to layout tables and gets into the best way to deliver a message.

My favorite story he tells is about unsuccessfully lobbying for a bigger budget for staff training for years – despite illustrating how little was spent per employee, etc. He finally convinced his bosses to up the spend on training when he gave them a graph showing that spend on watering and maintaining plants at head office was higher than spend on staff training

Great tip, thank you. Have popped the book onto my reading list.

He seems to have a newsletter as well so I’m going to give it a try in the meantime.

Another great article.

I am ultra-ultra lucky that I discovered investing at 18. I am pumping a pretty solid four figure sum in each month and provided I can maintain, my thirties are looking like they could be a pretty good period. Get that compounding snowball working as soon as possible!

I think if you continue at your current pace you’ll be long retired by the time you hit 40!

Pingback: 40 isn't old if you're a tree - Apex Money

Love the post! People in their 40s have a real opportunity to set themselves up for a great retirement by following what you outlined above. I’m about to turn 43 and just started learning about FI over the last couple of years. Like many people I wish I had started earlier, but I’m excited to be on the right path now. This type of content is really valuable and I hope more people my age discover this. I’ll be sharing on social! I have a blog and podcast geared towards this age group, so it fits right in with my mission as well. Thanks!

Thanks Ben.

Somehow, when you are twenty or even thirty, hitting 40s seems like hitting old age.

Then you get there (in my case, almost there) and realize you feel great and it’s just the beginning 🙂

Hi Ben, what are your blog and podcast called please? Keen to check them out. Thanks!

ps BOF – a great article, as always.

Recently starting following your blog and really enjoying it, thank you.

I have a question about pension contributions. I understand the tax efficiencies, but my understanding was that once you are at a point where you are likely to hit the lifetime allowance, those efficiencies start to massively tail off.

I’m 40, with about £350k in my pension, which I think puts me on track to hit the £1m(ish) limit in 15+ years time. With that in mind, I’ve stopped contributing to my pension and instead started filling up my ISA (primarily), with anything left over going into GIA/taxable investments.

Is this the right strategy?

Thanks in advance,

Cheers Stuart.

Yes, it is the right strategy and that’s exactly what I am doing as have a similar balance in pensions and don’t want to trigger the LTA.

There is a case for going over the LTA (which I’ve been meaning to explore for a very long time) but if you want to retire early, much better to start filling up the ISAs / GIAs to be able to pull the trigger.

Hi BoF,

Great article! I have a question about the “How to lose a job in 20 years” though.

For the income part, is that net of taxes or gross income you are referring to there?

Br,

Steve

Thanks Steve

I looked at it as % of net income (which is on the vertical axis of those charts).

That being said, you can also look at it as % of gross income, it’s just that you’ve got to account for a certain % of the gross income to go towards taxes etc.

Last but not least, pre-tax savings vehicles like pensions and 401(k)s muddle the picture somewhat.