Note: this post was first published in May 2020 and updated in June 2021

One of the biggest problems of personal finance is that it’s just so damn hard to get started.

We all know saving and investing money is something we should be doing, but hardly anyone does it – or does as much of it as they should.

Ask a hundred people above the age of 30 and I guarantee you the vast majority of them will say “I sure wish I saved more money when I was younger”.

In other words, show me someone who wishes they saved less money when they were younger, and I’ll show you a unicorn.

One of the biggest reasons for this savings crisis is that the whole topic is so damn wishy-washy at times.

Putting money away with the objective of feeling good about it at some distant point in the future simply doesn’t work.

Setting a specific goal and working towards it does. Today, I want to give you that specific goal:

Save £100k

There is a bunch of reasons why you want to aim to save £100k in the first instance.

First of all, it’s a meaningful amount – and yet it’s very much within everyone’s reach (more on that below).

Secondly, while saving up £100k won’t necessarily make you financially independent, it will surely help you sleep better at night.

Most importantly, £100k is the magic number after which your net worth begins to snowball.

Take a look at the graph above.

In this example, getting to £100k took six years. The second £100k, however, only took 4 years. The third – 3 years.

On and on it goes, until you are essentially adding £100k to your net worth every single year – all thanks to the power of compounding.

So how do you get onto this proverbial wealth-building ladder?

The Fastest Way To Save £100k

The answer will depend on two factors only:

1. How much money you are putting away (duh), and,

2. Which savings vehicle you are using to put money away.

The second question is even more important than the first – because choosing the right way to save can accelerate your journey by years, if not decades.

The graph below shows the number of years it will take you to save £100k in a variety of savings vehicles.

Before you ask, it assumes that instead of keeping your money under the mattress, you will invest it in a low-cost index fund instead.

A few observations:

- Even if you only put £50 a month in your ISA, you can get to £100k in 34 years.

- Choose a Lifetime ISA instead? You’ve just shaved four years off your journey, thanks to the government’s 25% bonus.

- Opting into a workplace pension? Even better – you now get both a tax break and an employer match. A higher-rate payer can save £100k 11 years faster by using a pension instead of an ISA.

Let’s pause here for a second because this is the most vivid illustration of the power of your workplace pension.

For those who need a reminder on how much free money you get with a UK workplace pension, here it is:

Here’s another example for you:

As a basic rate taxpayer putting away £250/month, you’ll clear your first £100k in just over ten years.

Want to use your ISA instead? You’ll need to double your contributions to £500/month to get to the same outcome.

I know which one I would choose.

The tradeoff, of course, is the ease of access to your ISA versus other investment vehicles.

Doubling the clip at which you are building wealth is a good choice for most people, but you’ll have to make up your own mind on this one (here’s a good guide to examining the tradeoffs).

It Only Gets Easier With Time

I was about to wrap this post up, but now that I’ve created this fancy chart I’m so proud of, might as well get some mileage out of it!

So here comes:

Once you’ve managed to save £100k, here’s how many years it would take to double that amount:

That’s right. Even if you contribute just £50/month, you’ve got the first hundred grand working away for you.

As long as you keep contributing even the bare minimum, you are guaranteed to clear two hundred thousand in less than a decade.

Want to keep cracking on? Once you’ve socked away £200k, you’ve really got the wind in your sails:

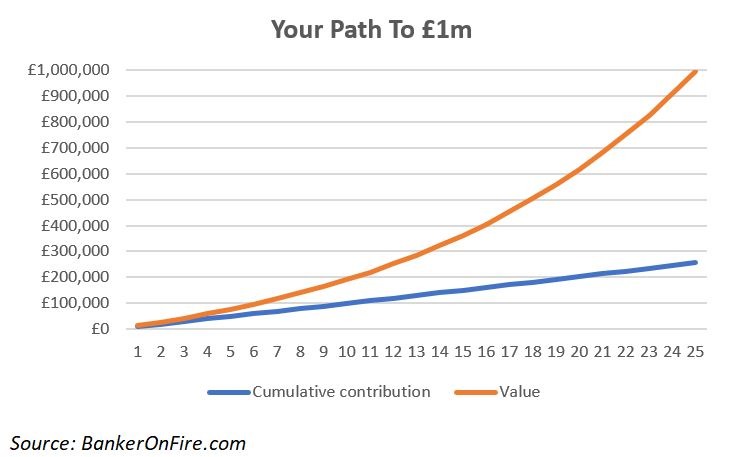

You get the point now, so I’ll leave you with one final graph – the time it takes to save £1m.

Not because I think everyone should aim for £1m or that having a piggy bank of that size will make you the happiest person in the world. I don’t.

Rather, because I think it’s a goal too many people find too lofty.

I disagree. Challenging – yes. But for someone with enough energy, consistency, and most importantly – time, it’s well within reach.

This is why:

Provided you start early enough, you can clear £1m in the course of your working career by simply contributing £200/month into your workplace pension.

And if you are a higher or an additional rate taxpayer, you really have no excuse. Becoming a pension millionaire is well within your reach.

But you will never get there if you don’t save that first £100k. So you better get started now.

Happy investing!

PS: By popular request, I’ve uploaded the underlying excel file. You can download it here and play around with the assumptions.

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

This is awesome, I love your graphs. It’s interesting that you chose to cut it off at £500pm and I wonder what the numbers would look like for someone saving £1000, £1500 or even more per month. But I do remember when I first started my FI journey, even saving 10-20% on a regular basis seemed like a lot.

Thanks Kat. You are spot-on, the reason I initially cut the charts off at £500pm is that early on, most people’s savings are probably south of that number.

That being said, your comment makes a lot of sense, so I’ve extended the charts all the way up to £2k/month.

Enjoy!

Awesome, thank you! I love charts and graphs, they’re so interesting. Wow, with £2000 pm you can really get ahead so fast!!

Everyone always says the first £100k is the hardest and your graphs really illustrate that.

As Charlie Munger once said the first $100,000 is a bitch, but you gotta do it. I don’t care what you have to do – if it means walking everywhere and not eating anything that wasn’t purchased with a coupon, find a way to get your hands on $100,000. After that, you can ease off the gas a little bit.

I love that quote. Unfortunately, I think old Charlie said that a while ago.

$100k is still a solid pot of cash, but not nearly the same as it was back in the 90s.

The £2k/mo sacrifice calculation is a bit of a nonsense.

You’ve based the 9.7 years to reach £1M figure on an employer matching an unlimited amount at 60%, for a total gross contribution of £5818/mo.

For starters ~£5800/mo is £70K/year, so it’s outright impossible for a single earner because of the £40K annual allowance.

A more realistic scenario is a professional earning £200K/yr having their contributions matched 100% up to, say, 10% of their salary. In this case they could sacrifice £20K/yr gross and max out their pension allowance. Take home without the sacrifice would be ~£9,763/mo, with sacrifice £8,880/mo, for a net cost of £883/mo.

At 8% it will take this person around ~14 years to reach £1M.

A couple earning £100K each, each shooting for £500K, each could do it far more cheaply but it would take the same duration.

Hi and thanks for your comment.

Correct, if you are a single earner you won’t be allowed to contribute more than £40k p.a. to your pension (unless you are using your carryforwards).

However, a married couple sure could – and it makes a ton of sense to think of pensions at a household level (as you can better optimize for taxes and LTAs that way).

I also worked for two employers who matched up to 20% and 25% of salary respectively, so these plans (while generous) certainly exist.

Ultimately, everyone’s situation will be different which is why I uploaded the spreadsheet so that folks could tinker with the assumptions.

Cheers

Damian

Thanks for your calculations. It really does put things into perspective. One thing though- how can you calculate return for work place pensions. For example i contribute to a public sector pension but i dont think they give any returns. They just sit there and accumulate. They are locked to grow with inflation though. Can you clarify please.

Hi there. Unfortunately tough for me to comment without knowing how your scheme operates. The way the calculations above work is as follows:

Start with your contributions

Add employer match (minimum mandatory level of 3%, many employers go above and beyond this)

Add tax break (will differ depending on your tax bracket)

Add an 8% return per year assuming your pension is invested in a low cost index tracker

Hope this helps!

This gives me a huge amount of comfort (although 8% might be punchy) 100k in my Isas 200k in my pensions and contributing 2k to my pension and 1100 to my isa so I’m really looking forward to the snowball now

Sounds like you are in an awesome place – likely on track to clear £1m even with minimal contributions from here onwards. Nicely done!

Been reading your blog for a while, been enjoying it a lot! Thank you 🙂

I live in a country where investment vehicles like ISAs don’t exist. Over here there’s no way that I know of to minimize tax on capital gains when you invest by yourself

Would love your thoughts and advice for folks like me who don’t have easy access to tax-efficient schemes

Glad to hear that you’re finding the blog useful!

Whereabouts do you live? Tough to give a view on investment options without having more information. At a high level, in the absence of tax-sheltered vehicles two possible options are:

1. Invest through “regular” accounts, focusing on capital appreciation (to avoid triggering a tax on dividends received along the way). Once in the withdrawal phase, the pot can be used to fund living expenses by selling a portion (i.e. 4% a year). This could minimize the tax liability as most people are in a lower tax bracket by that point in time.

2. Real estate – but differs MASSIVELY depending on country etc.

The best thing you can do is speak to a local financial adviser to understand whether there are any tax-deferred options.

I live in Portugal. We do have a thing called PPRs where capital gains are taxed at 8% if your investment horizon is 8+ years.

Problem is that all of them are actively managed, charge ridiculous fees and need to comply to silly portfolio rules like >50% allocation to bonds no matter what. And you can only touch them under very restricted conditions.

Been doing #1 for a while, although at first I did buy a bunch of distributing ETFs… ?

Anyway, I guess we have plenty of sunshine so can’t complain too much!

PS: ah, this is interesting — just learned the EU is working on legislation for european-wide pension funds: https://en.wikipedia.org/wiki/Pan-European_Pension

It’s frustrating that the government won’t do more to encourage people to save – even though they will struggle to fund everyone’s pensions in old age.

Hopefully changes soon – and the pan-European Pension initiative is very interesting!

Love your blog, keep it up! I may be being pedantic but surely you can only save £1667 pcm into an ISA?

Thank you!

Indeed – if you’re single, you are capped at £20k. But if you are looking at it from a household perspective, you can do twice that amount, so really depends on the situation.

Ps: Same applies to LISAs though so in all fairness my table is not entirely consistent!

Hi BoF – Just started reading your blog and have really enjoyed the posts so far.

Wondered whether you can post projections for using a SIPP rather than Workplace pensions? Unfortunately, I don’t have access to a workplace pension with employee contributions (public sector worker – very good defined benefits scheme though so cannot complain).

Thanks

Thanks Ben, appreciate it.

You are right – I’ve excluded the SIPP option as otherwise the tables would become unwieldly.

Let me update the tables when I get a moment – might end up doing a dedicated post on the SIPPs as I think helpful to a lot of people.

Thanks so much – I’d be really interested to read it.

I’ve been enjoying reading through back posts of your blog. Great stuff. Keep it up.

Maybe it’s a naive question regarding pension contributions – but what about the question of trust that the money you are putting away now will indeed be accessible to you in 30 years time? I guess knowing how some other governments operate, some people might be reluctant to contribute to pensions as they are afraid they will never see their money again. It might sound crazy for someone from the UK I believe 🙂 But is there any possibility that the government/some other institution might ‘borrow’ your money to fight some crisis etc, and you will not see your savings after sacrificing for 30 years?

Hi there. This is a sensible question to ask and no, it’s not naive at all. Any time you are locking money away, you need to be comfortable that it is safe in whatever vehicle you are using.

I cannot make a blanket comment about all governments, but I have strong doubts the UK (or any other developed country) government will go down that path.

First of all, they already “have” your state pension to play around with in the form of the budget. Secondly, the way the government “borrows” money to fight crises these days is by issuing bonds, which are bought by investors and the Bank of England. So it doesn’t necessarily “need” your money.

Instead, the real risk is that the government will tweak the pension withdrawal rules. Perhaps push out the pension age further or put a higher tax rate on withdrawals. It would be a massively unpopular decision that would kill all confidence in the pension system.

My guess is that the likelihood of draconian changes is minimal as eroding trust in the pension system will mean people will save less – and the government will thus need to provide a higher level of support via the state system. This is clearly not something it wants to do.

Finally, remember – if the government wants to tap your savings for something, it will – and there’s no need to do it via the pension system. Remember the time Greece has “collected” 10% of all bank deposits? The only alternative is to keep your money under a mattress and we all know that isn’t really an option…

Hey there! I read a lot of personal finance blogs and yours is one of the best I’ve come across in a long time. So thank you!

Just FYI. I started a thread on Reddit seeking clarification around some of the calculations that you make in this post. If you have a moment, it would be cool if you could respond to some of the points raised?

Again, many thanks for all your amazing content!

https://www.reddit.com/r/FIREUK/comments/hmzckw/fastest_way_to_1m/

All the best,

Redpillfinance

Hi there – thanks for the kind words. I’ve responded to your post – let me know if anything is unclear.

I usually try to put up my excel files as well but don’t always do it as takes a bit of time to cleans all the private info. If I have a moment I’ll upload my file above.

Yes, many thanks for your reply! Really, really appreciated.

And yes, an Excel file would be amazing!

Keep up the great work 🙂

Hi, again great post. Does the total value of s pension not need to be discounted by tax paid on money withdrawn from the pension? So 20% minus the personal allowance. Which if we assumed a withdrawal of £40,000 per year and an allowance of £12,000 per year would mean a 14% overall tax on funds withdrawn.

Yes, but tough to generalize as everyone’s tax situation will differ.

For example, a family of two may gun for withdrawing 12k each from their respective pensions and paying zero tax.

Its interesting comparing Canada, the UK and our plans in the US. The terminology and acronyms are different but the opportunities to leverage your savings and investments are more alike than they are different. Most of today’s retirement accounts did not exist when I entered the workforce, it was almost ten years before I was eligible to invest in a tax deferred account but by maximizing my contribution each year I was able to build a seven figure retirement account by the time I retired slightly early. And the best part was I never really noticed not having that money to spend because it came out of my pay before I received it. At the same time I worked beside people that did not contribute at all to retirement accounts, I wonder how they are doing now?

I think automatic enrolment and paying yourself first are two of the most powerful behavioural hacks when it comes to financial planning.

Sadly, they weren’t really employed (at least here in the UK) until about 15 years ago, when Thaler was involved in setting the UK workplace pension agenda.

At the end of the day, the responsibility for saving lies with the individual, not the state. That being said, I can’t help but feel sad for those who haven’t taken the opportunity to do so.

It’s amazing just how important the first 100k is but I would argue that the second most important milestone is around the $300-$500k mark. That’s when you’ve actually put in a lot of work to get there and when you actually have the most chances of feeling *impatient* and *burnt out* unless you work a job that you love where the time passes by VERY quickly.

However, every journey starts with a single step and 100k is a great step to get into.

That’s an interesting observation. I guess it depends what your end goal is.

For some folks, knowing there’s a long road ahead might actually be helpful in focusing them on the process. Then, when you get closer to the goal (let’s say 2-3 years out) you can get much more impatient.

Certainly has been mine experience and I had to actively self-moderate it!

Hi,

I have perhaps a silly question… I’ve got a current workplace pension with £50k, plus an old very secure (council) pension which I don’t currently contribute to with about £60k then finally an active vanguard SIPP with £100k (over 2 funds) that I drip feed a little in to each month.

I like the diversity of all this as they are all invested in different passive index funds and I figure it gives me options on when to take each so I can span it out before dipping into the largest and can let it grow.

However, say I took the vanguard SIPP, I have £45k in LS100 and £55k in global all cap for historical reasons. Would I be better in terms of compounding to have it all in one £100k fund? In my head it’s going to be compounding anyway and should all add up, but trying to understand if I’m missing a trick here.

Hi there.

No you are not. You get the same compounding on one $100k pot, two $50k pots, 10 $10k pots and so forth.

However, I do think it makes sense to consolidate your pensions under one or two platforms for asset allocation / simplicity of management reasons.

Hope this helps!

That does help thanks, good to get a sense check here. I already did the consolidation but and the current spread just makes sense for now. I’ll keep an eye out as things progress as realistically I’ll not be dipping in to any for 20 years yet.

Pingback: Career choice doesn’t matter: anyone can become a millionaire

Pingback: Can You Become A Millionaire in 10 Years? - MoneyGrower