If you look across the pond, it’s clear that becoming a dollar millionaire simply doesn’t hold the same allure that it used to.

Cost of living increases, especially in housing and education, have eroded the real purchasing power of a million dollars.

At the same time, the bar for a “good” life (whatever that actually means) has been reset even higher thanks to social media.

Thankfully here at home, being a “sterling” millionaire still seems to carry some weight.

It also seems we have quite a few millionaires.

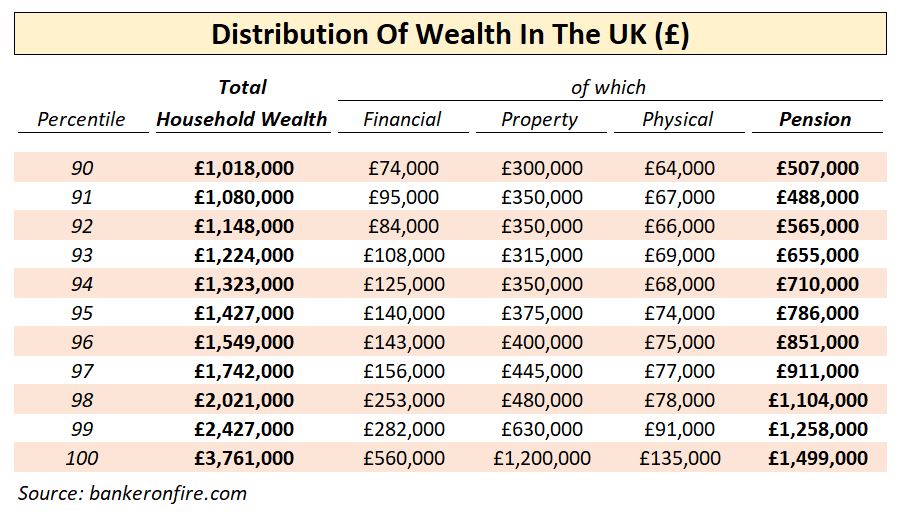

According to the ONS, the top 10% of the households in the UK have a net worth exceeding £1m.

It might not seem like much, but given there are roughly 27m UK households in total, that’s a cool 2.7m millionaire households – in excess of 5m people.

On average, a household in the top decile of the wealth distribution has a net worth of c.£1.4m.

If you work your way even further up the spectrum, the top 2% of households have a net worth exceeding £2m. That’s roughly 540,000 households around the country.

And as it turns out, pensions are one of the key components of household wealth for the wealthiest UK families. For example, those in the top decile have about 55% of their household net worth in pensions.

And for those in the top 2%, the value of the household pension pot easily exceeds £1m.

The message is clear – if you want to get wealthy, you better pay attention to your pension. But how hard is it to become a pension millionaire?

Some people will tell you that it is an artefact of the days gone by, when gold-plated defined benefit pensions were aplenty and annual allowance limits didn’t exist.

But if you look at the facts, it’s actually the opposite.

If anything, becoming a pension millionaire may have gotten easier than ever in this era of mandatory workplace pension enrollment and the ubiquity of index investing.

Let me show you why.

Meet Three Pension Millionaires

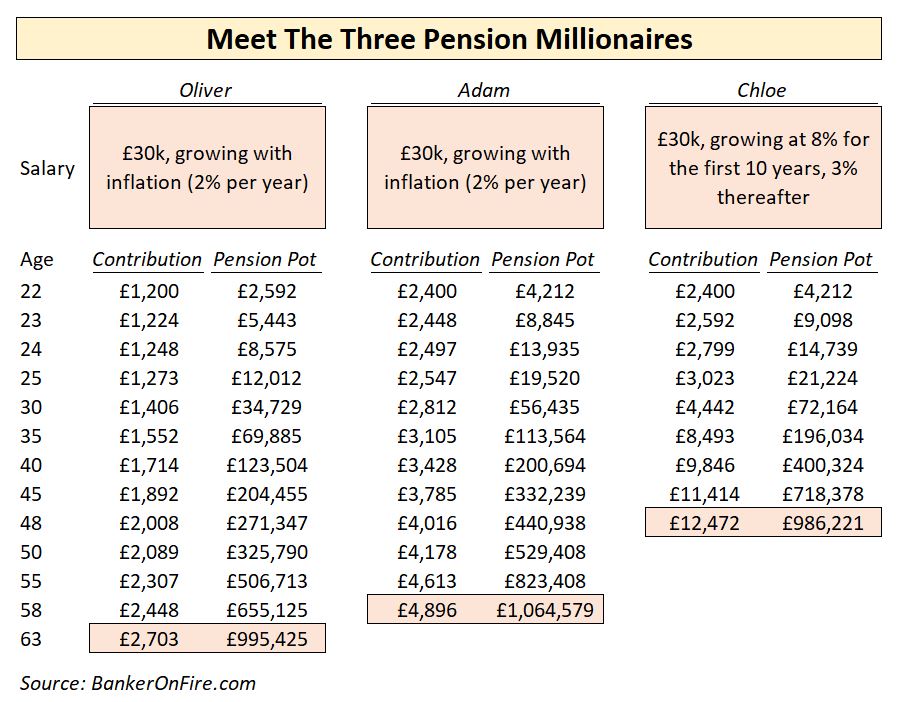

1. Ordinary Oliver

As the name suggests, Oliver is an ordinary guy in every single respect. After graduating from university aged 22, he started working at a medium-sized company in his home town.

Oliver’s starting compensation was £30k per year, the average UK annual salary based on the latest available UK income distribution data.

Oliver never gets ahead of the crowd. Therefore, his earnings simply rise with inflation at about 2% per year. And if Oliver feels his pay with the current employer has been stagnating, he resets the bar by finding a new job.

When Oliver starts his job, he is automatically enrolled in a workplace pension scheme. Oliver contributes the minimum of 4% of his pre-tax salary (£1,200/year), which his employer and the government top up with another 4%.

In other words, Oliver’s annual contribution of £1,200 is doubled to £2,400.

Oliver chooses to invest his pension in a low-cost, diversified index tracker fund. Based on historical stock market data, he knows that assuming an annualized return of 8% isn’t unreasonable.

Yes, there will inevitably be bumps along the ride, but Oliver will stick the course.

His patience will be rewarded. By the time he turns 63 he will have exactly £995,425 in his pension.

Add another month of stock market returns and Oliver retires a pension millionaire, four years ahead of the state pension age.

For reference, Oliver’s out-of-pocket contributions worked out to exactly £23 per week.

Not too shabby!

However, presumably one reason you are reading this blog is that you don’t exactly want to wait until you are 63.

If that’s the case, you’d probably get along with the chap below.

2. Ambitious Adam

Adam is also working an average job with an average salary that never gets ahead of inflation. Unlike Oliver, he wants to quit the rat race ASAP.

With that in mind, he jacks up his contributions to 8% of his salary. That’s £2,400/year or about £46/week.

His employer’s matching is set to a minimum of 3%, working out to £900/year.

There’s another £600 from the government in the form of a tax break. Total annual contributions – £3,900.

Guess what? Adam’s devious plan to escape his corporate overlord works out. The value of his pension pot is likely to exceed £1m shortly after his 57th birthday.

Adam hands back the corporate ball and chain a full six years before Oliver does.

The cost of getting six years of his life back? Increasing his contributions by £23/week.

I’ve got to say, Adam’s plan holds much more appeal to me than Oliver’s. But what if you could you do even better? Let’s meet Chloe.

3. Career-minded Chloe

Chloe doesn’t think there’s anything wrong with being average.

However, she realizes that pursuing above-average financial goals (like becoming a pension millionaire) on an average income isn’t easy.

It will take time to let compound interest work its magic and discipline to stay the course while that magic bears fruit.

But what about people who are dedicated to getting wealthy AND work in well-paid professions like accountancy, finance or consulting?

Chloe has always had an eye for numbers and her sights on a well-paid career. Out of university, she got a Big 4 gig paying £30k/year and progressed relatively rapidly up the ranks until she was making £65k just 10 years later.

With the hard yards behind her, Chloe took her foot of the gas a little. She still put her hours in but stopped chasing promotions as hard. However, her reputation and the momentum she has built up continued to serve her well.

As a result, Chloe’s pay only grew by about 3% per year from that point onwards.

However, because her earnings were higher, Chloe was able to afford to contribute 12% to her pension. The higher rate tax break of 40% on her pension contributions also helped.

She watches the value of her pension pot cross £1m by the time she turns 48.

It only took her 26 years – time to pack it in and enjoy life!

There you go. Three ordinary people becoming pension millionaires – simply through recognizing the merits of compound interest, tax-efficient investing and tracking the stock market.

Is there anything I am missing? Sure I am. Let’s take a look at a few potential shortcomings of my analysis.

Your Earnings Won’t Evolve On A Linear Path

Valid challenge. While there are quite a few professions that start new graduates on £30k/year (as Chloe’s example illustrates), some people’s earnings will have a very different trajectory.

It’s not unusual to start below the average earnings and progress into the above-average territory as you build up your skills and experience.

What that means is that your contributions will be back-end weighted, with less time to compound in the stock market.

However, there are multiple solutions to this conundrum.

The beauty of being in your 20s is that you rarely have any family obligations. This means you can either reduce your living expenses by staying at home for as long as possible or house sharing with friends.

Alternatively, you could take on a side hustle.

Ordinary Oliver is only making pension contributions of £23/week. Slam the gig economy all you want but even if you make a fiver an hour (well below the minimum wage of £7.50), that’s only 4.5 hours out of your weekend. Easily done on a Saturday afternoon – and you can be home by 8pm.

For Ambitious Adam, pension contributions are £46/week. That’s an extra day of work on Saturday or Sunday. Perhaps not as much fun – but it buys Adam 10 years of freedom.

I’d say the price is worth it.

What’s The Point Of Becoming A Pension Millionaire? The Government Will Move The Goalposts Anyway

Another valid one. Our beloved government has indeed changed the pension rules more than once. I’m dead certain there are more changes ahead.

With the lifetime allowance (LTA) currently at £1.05m, becoming a pension millionaire is dangerously close to the penalty box.

However, don’t assume that you are powerless to protect yourself from the tax grab.

First off, the LTA is designed to grow with inflation. Chances are that by the time you retire with £1m in the piggy bank, the LTA is well north of its current limit.

Secondly, there are pension pot hacks you can follow to avoid an LTA penalty. One of these is contributing to your spouse’s pension.

Another (albeit an extreme one) could be getting divorced to get a sharing order on your LTA (and subsequently re-marry).

Most importantly, remember that once you are on track to hit £1m in your pension, work becomes an optional activity.

And if you are like Chloe and hit £1m before you turn 50, there are ways to “bridge” the seven-year gap before your pension pot becomes available.

I Won’t Ever Get An 8% Return

I have far less sympathy for this one. While historical stock market returns don’t predict the future, they do point to 8% as a relatively achievable target.

If you refrain from doing stupid things trying to time the market, selling after every correction and investing in anything but low-cost, diversified index tracker funds, an 8% return shouldn’t be out of reach.

£1m Won’t Go Nearly As Far In 30 Years

Another valid one. Sure it won’t – inflation will eat the real purchasing power of your cash.

But guess what – hopefully you won’t be alone then! And provided your partner has the same values as you do when it comes to money, they could well have a £1m pension pot of their own.

As it turns out, becoming a pension millionaire is not so hard after all. All you need is time, discipline and a low-cost index tracker fund.

Remember – those who really want something, find a way. Those who don’t – find an excuse.

Readers – are any of you gunning for £1m in your pension? Where are you on that journey? I’d love to hear from you in the comments below.

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

Pingback: 7 facts you need to know about Hong Kong’s Mandatory Pension Fund (MPF) - MoneySaveGeek

Pingback: Weekly Acta #1 - Ad Otium

Really enjoyed this article, not least because it confirms my own long held belief what great value based pension saving is. I remember feeling incredulous when I first totted up the tax savings and “free” money on offer. And later amused when my HR team got in touch because their new system would no longer allow me to be paid under the minimum wage because I was salary sacrificing so much of said salary into my pension. I’m about 2/3 of the way to being a pension millionaire.

I also appreciate a millionaire ain’t what it used to me, but for a kid that grew up in an underclass household, it still has a certain cache to it.

Glad you enjoyed it!

I think any way you cut it, a million (especially in sterling terms) is still a massively serious chunk of money.

For a while, we did something similar with my wife’s pension contributions. Once I got tapered out, we channeled our combined contributions into her vehicle for a while which took her into pretty silly territory as a % of salary.

Very glad we did that and are now sitting on two fully funded pension plans.

As I understand it, Chloe will have to wait 7+ years to access the pension (about to go up to min 57 years old) which is the main reason I’m not squirreling any extra contributions on top of my pension: having a chunk of money large enough to retire on isn’t much good if you can’t use it for maybe ten years! Instead an index fund in a share ISA is the best I can do, at least there is no tax payable on withdrawing: the plus side of missing out on a tax break when contributing.

Yes fair enough. Exactly what I am doing now that we are pretty much guaranteed to hit the LTA in mine and my wife’s accounts.

Step one – build up a proper pension balance

Step two – figure out a way to bridge the gap to that pension:

https://bankeronfire.com/pension-vs-isa-settling-the-debate

Pingback: Six Reasons High Earners Fail to Get Rich - Physician on FIRE