I never cease to be amazed at how much misinformation and bad advice exists out there when it comes to building wealth.

Sometimes the bad advice is given in good spirit and with the best intentions. In other situations, people are trying to capitalize on others’ lack of financial knowledge to take advantage of them.

Either way, the effects can be disastrous.

Instead of growing their net worth, leaving the jobs they hate and living their best lives, people lose years and sometimes decades dealing with the results of their financial mistakes.

At best of times, they reach financial independence far later than they should.

Some of the worst advice I have seen relates to the mortgage on your primary residence.

Time and time again, we are being told that paying off your mortgage as soon as possible is a great idea. Those who manage to do so often parade around as if they had won a gold medal. Those who don’t envy the ones who did.

There are, of course, situations when you should try to pay off your mortgage early. The reality, however, is that it can also be a very bad idea.

The value of primary residence forms a key net worth component – and therefore a key lever for building wealth – for the majority of people. Paying your mortgage off early will often rob you of optionality and can have an outsized negative effect on your wealth.

To avoid falling into this trap, read on so that you can figure out the right decision for you.

Mortgage As A Wealth Building Tool

Imagine for a moment that you have received a one-time lump sum windfall of £500k. The reason I picked £500k is simple – it is a nice round number and it is also pretty close to the average house price here in London (though unfortunately not where I live).

After the initial euphoria subsides, and assuming you don’t do anything stupid with the money, you begin to contemplate the various ways to use it.

To make things simple here, let’s assume there are two things you could do:

Option 1: Solve your housing situation once and for all by using all the cash to buy a nice terraced house for £500k, mortgage free.

Option 2: Buy the same £500k house but take out a 50% LTV mortgage at 2% interest. Use the remaining £250k to invest in the stock market.

If you are like most people, you are probably going to be mightily tempted by option 1.

After all, who doesn’t want to live mortgage-free for the rest of their lives? Your wife / husband / parents / friends might also be encouraging you to lose the mortgage shackles forever!

Unfortunately, going this route is also likely to leave you significantly worse off financially.

Let’s look at both options in detail to see how they compare 10 years out.

Option 1: Buy Your House And Live Happily Ever After

Let’s play this one out to see what happens 10 years after that momentous event.

House equity: you fully own a house worth £500k.

Because house prices tend to move with inflation, let’s assume that over the next 10 years, the annual price growth will average out to 2.5%. In 10 years, your £500k house will be worth £640k. Well done to you!

That’s not where it ends. After all, because you no longer have a mortgage, you have extra money sitting in your bank account every month.

If you hadn’t been so lucky to get a £500k windfall, you would have used this money to make your mortgage payments. You no longer have a mortgage but being a financially responsible, forward-looking person you decide to invest them in the stock market.

Stock portfolio: Mortgage payments on a £250k mortgage (to be consistent with option 2 below) will run you about £924 per month or £11,089 per year.

Assume you have the discipline to consistently invest them in the stock market. If the stock market returns ~6% per year (as it has done historically), you would be sitting on a nice stock market portfolio of £146k at the end of 10 years.

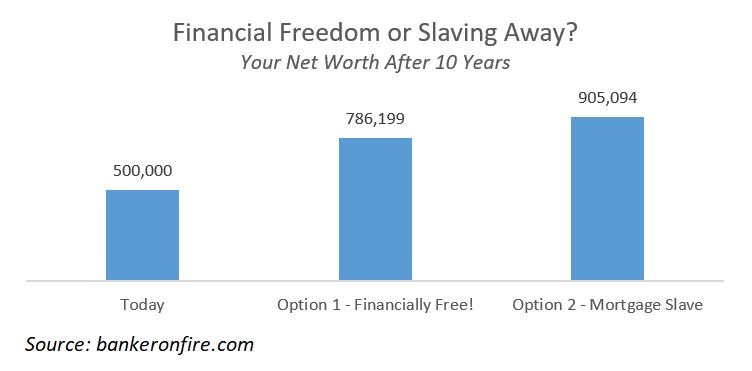

Total net worth: combined with the £640k of equity in your house, you are now sitting pretty with £786k of equity in your house and your stock market portfolio.

You are up 57% on your original £500k investment, implying a 4.6% annual growth rate. Job well done, you think… but is it?

Let’s now look at the alternative.

Option 2: Remain A Mortgage Slave For A While Longer

You manage to ignore all the noise and financial misinformation and decide to go against the grain.

You use £250k to make a down payment on that same dream terraced house, and take out a £250k mortgage. Interest rates are low and your credit quality is high, so you get a nice 2% rate on a 30-year mortgage. Your annual payments run £11,089 (same as in example above).

You then use the other £250k to invest in the stock market. It’s a big amount of money, but you are an astute student of financial history and you know that despite the fluctuations, the market typically delivers at least a 6% annualized return over the long run.

You gird your loins and buy yourself a nice, low-cost index tracker.

So what happens in 10 years?

House equity: your house is now worth £640k, just like in option 1 above.

However, being a mortgage slave and all, you are not yet debt-free. The balance of your mortgage is £183k and the equity in your house is therefore £457k.

Stock portfolio: despite some uncomfortable ups and downs, you do the right thing and avoid the temptation to trade.

As a matter of fact, you barely log on at all, other than reinvesting your dividends once a quarter.

Then, at the end of year 10, you log into your brokerage account. Voila – due to the magic of compounding your stock portfolio has grown to £448k.

Total net worth: between the house equity and your stock market investments, you have £905k combined.

Your initial £500k has grown by 81% in total or by about 6.1% every year.

Most importantly, you are a whopping £119k better off than you would be if you paid off your mortgage in full.

So What Exactly Is Going On Here?

If this is all a little counterintuitive, don’t feel bad. After all, the conventional wisdom is that owning your own house is the best way to build wealth.

That, however, is only part of the wealth building equation. The other key cornerstone of making money in real estate is using leverage, and unfortunately this bit of the money-making secret sauce is missing in option 1 above.

You end up tying up all of £500k in an asset that barely protects you from inflation at 2.5% per year.

In reality, you may end up in an even worse place financially if you go with option 1.

Human willpower is a limited resource and chances of you diligently reinvesting your mortgage payments into the stock market are low.

Sure, you may end up putting some money into the stock market. You may also end up taking a very nice holiday, doing up your bathroom, buying a new car or even leaving your job.

None of these are bad things to spend your hard-earned money on, but wealth builders they are not.

With option 2, you employ leverage on your primary residence to increase the returns on your home equity from 2.5% to 6.2%.

You invest the other half of your £500k windfall in a 6% yielding instrument – the stock market. Your blended return works out to 6.1%, which adds up to an additional £119k of wealth over a 10 year period.

The Advantages Of Not Paying Off Your Mortgage

- Discipline. Nothing like a threat of repossession to keep you working hard and making your mortgage payments as opposed to blowing your budget on unnecessary expenses

- Diversification. Instead of having most of your equity tied up in your primary residence, you can buy other properties – or diversify into across asset classes (stocks, savings, REITs etc.)

- Liquidity. In theory you could release some equity by remortgaging but it’s much easier to sell a portion of your stock portfolio to realize some liquidity

Note: you will notice that I have once again ignored taxes in the examples above.

The first reason I did this is that everyone has a different tax rate and I wanted an example that everyone could use.

More importantly, there are multiple ways to get a tax break on your stock market investments (i.e. through pension contributions, ISAs, LISAs, CGT exemptions etc.), which will more than offset your tax liability.

The path to wealth and financial independence can be long and hard. Unfortunately, conventional wisdom often makes it much longer and harder than it has to be.

There are some situations where it may make sense to accelerate your mortgage repayments. More often than not, there are better things to do with your money.

As always, I am uploading the spreadsheet that details the calculations above – you can get it here.

Have a play around and post any thoughts or questions you have in the comments section below.

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

100% agree with you but sometimes the extra guaranteed ‘cash flow’ is nice after paying off debt.

I have a lot of rental houses and I paid off 2 mortgages this year. I still have plenty of mortgages left but damn that cash is nice sometimes.

Nice – and makes a lot of sense when it comes to managing your overall leverage position across a number of mortgages.

Are your rental properties mostly in Toronto / GTA or did you venture outside Ontario as well?

I’m 25 and bought my first flat 5 months ago. Due to the front end loading of interest and the age that I’ve bought my flat, I’ve decided to do a 5 year fixed repayment mortgage, with the aim to throw pay rises & bonuses at the mortgage. The idea isto become mortgage free in 7-9 years. This will then serve as a mortgage free rental property. In this scenario would you advise to pay off the mortgage or still keep it as leverage?

It depends on your objectives. Given you are 25 I assume you want to build your net worth as quickly as possible and don’t need the cash flow to sustain your current lifestyle.

If that’s the case, I wouldn’t overpay the mortgage. Save up the extra money and you have two options:

1. Invest in the stock market (ideally through a low cost index fund) to diversify your exposure across asset classes (real estate and stock market)

Make sure you read this first though: https://bankeronfire.com/stock-market-investing-whats-the-worst-that-could-happen

2. Refinance the mortgage on your flat in a few years to release some extra equity, add it to your savings and buy another property. You’ll have a concentrated exposure to real estate but it works for many people.

Of course if you just want pure cash flow in 7 years then you should keep paying off the mortgage. Your net worth probably won’t be as high but you’ll have cash coming in at a decent clip each month.

Most importantly, well done on buying a flat so early on! It’s a massive step towards financial independence.

Interesting post once again. I thought it would be interesting to run the numbers again around a similar tact I am considering , interest only. I don’t think it’s as balls out a proposition as most do, so:

£500k windfall

£375 interest only mortgage

£125k deposit/equity

£375k lump sum into stocks

£301 per month into stock (saving on mort repay)

10 years time

£731601 stocks value

£640000 house value

Minus

£375000 original loan

£996601 equity, up around another 9% of option 2 and house paid off.

I’m considering remortgaging , releasing equity to buy back past 3 years in SIPP. Will get the 25% top up also. I’m a late arrival at the FI world unfortunately. Any flaws in calculations please highlight. Also any suggestions on proposal? I am aware obviously returns could be lower but I can’t see myself being any worse off taking this route.

As ever, not financial advice (and I don’t have the benefit of seeing the underlying maths), but looks directionally correct.

As you point out, getting a 25% boost on 3 years of pension contributions makes a massive difference.

Ultimately, boils down to being mentally comfortable with carrying a mortgage and having a sufficient cash reserve to withstand any temporary wobbles (a stretch of unemployment, an illness, a market correction)

Best of luck and would love to hear how you get on!