Over the past few months, I have been spending a fair bit of time on the topic of investing in bonds.

For some people, bonds represent an excellent way to soften the inevitable volatility of the stock markets.

For others, it’s a way to exercise full control over the timetable of their retirement.

And as today’s post proves, in addition to the benefits above it can also be a very attractive investment strategy on its own.

So let me turn it over to Colin – a long-time reader of the blog who kindly volunteered today’s guest post on the topic.

Low Risk Corporate Bond Investing

Much has been written about portfolio allocation and the ratio of equities to bonds you should hold.

There are many documented rules around this. Probably the most well-known one is that the percentage of equities should be 100 minus your age.

Thus, if you are aged 20 then your portfolio should consist of 80% equities and the remainder in bonds.

If you are aged 60 then hold 40% in equities, and so on.

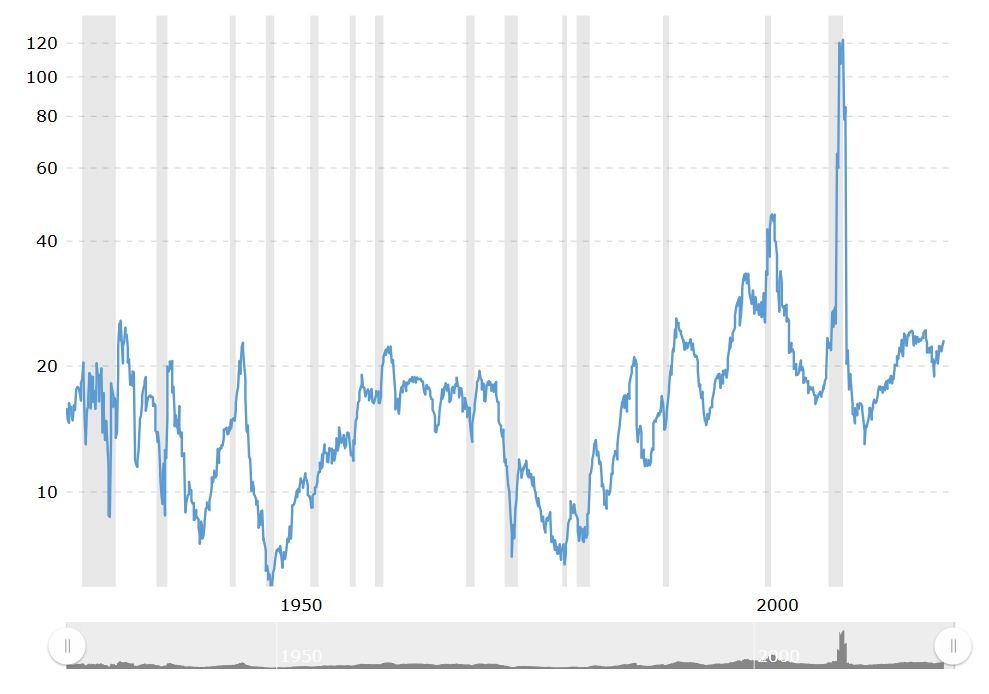

Not a bad rule of thumb but it does not take into account stock market valuations.

After all, sometimes the stock market is expensive – and sometimes it’s cheap.

Evolution of the S&P 500 P/E Ratio

So let’s say we are aged 50 and we therefore choose to allocate half our portfolio to equities and the other half to bonds.

We then have to choose which equities and which bonds to buy.

The bond aspect of the question is the subject of today’s post. I’m not going into the basics of bond investing since Banker on Fire (BOF) has done an excellent job of it already.

Back To Basics

The basic choice is between government bonds (called gilts in the UK) and corporate bonds. The latter are issued by companies to raise finance for their business activities.

Gilts have the advantage of maximum safety since they are guaranteed by the UK government and therefore they can be repaid simply by raising taxes.

The downside is that interest rates on gilts are very low at the moment (typically less than 2%).

Corporate bonds are generally riskier – but provide higher returns.

Personally, I’m a fan of corporate bonds in specific circumstances. To understand why we need to spend a bit of time talking about bond yields.

Bonds generally pay a coupon or payment on a regular basis, typically twice a year but it can also be more or less often.

It’s useful to think of this as an interest payment. The rate is often identified in the name of the bond issue.

Here’s an example:

Ladbrokes Group Finance PLC 5.125% STG BDS 16/09/2022 (WI) (LAD2)

This is a bond issued by Ladbrokes, the well-known bookmaker, and it pays 5.125%.

There is other information in the bolded listing above.

Corporate bonds also have a redemption date which is the date when your capital is returned to you. In this case, the redemption date is 16th September 2022.

These types of bonds are redeemed at “par” which is the price they were originally sold at. This price is typically set at £100.

On the redemption date, bonds are redeemed (swapped for cash) at the par value.

In between the issue date and the redemption date, the bond varies in value, just as share prices do.

Making Money With Bonds

Let’s continue using the above Ladbrokes bond as an example.

It was issued on the 4th June 2014 at a par value of £100. It pays two coupons per year at the stated rate of 5.125%.

Now assume that the bond dropped in value to £95. As bond prices decrease, bond yields increase and vice versa.

In this case, the price has fallen slightly so we would expect the yield to increase. The simplest way to calculate a bond yield is to divide its coupon payment by the face value of the bond.

If we do that we get:

5.125/95 = 5.39%

As expected, the yield has increased. This sounds great but it does not take account of the time value of money invested, the coupon payment frequency, and the maturity value.

To take all these factors into account, we need to use a measure called the Yield to Maturity (YTM).

The calculation is more complex but a simple internet search will reveal several online calculators without the need to calculate YTM yourself.

For the bond highlighted above the price was £99.50 on the 12th March 2020, meaning the yield would be slightly higher than than the listed 5.125%.

It gets much more interesting when the markets crash.

In late February, the equity markets started dropping due to the effects of Covid. This was the time to start monitoring the price of corporate bonds.

On 17th March the price of the Ladbrokes bond dropped suddenly to £68.63. At that point, it represented amazing value.

Here’s why:

We can enter the current value, the par value, the years to maturity, and the annual coupon rate into any on-line YTM calculator to derive the YTM.

Using the values above we get a YTM of almost 24%.

In other words, we could buy the bond for £68.63, hold it to maturity and receive the par value of £100 for each bond.

It’s like buying a share – all while knowing its exact future value.

But that’s not all there is to it.

Hidden Dangers

There are three important factors to consider before you even think of snapping up this apparent bargain:

1. You must hold the bond to maturity

The bond’s price may drop even further. The Ladbrokes bond dropped to around £65 a short time after the £68.63 price but if you hold to maturity it will be redeemed at par (£100).

Today the price is actually above par at £102.425 (this is called trading at a premium).

2. You must be confident that the issuer will remain solvent

In the case of the company becoming insolvent you’ll join the normal queue of creditors to get any money back. The good news is that bondholders take priority over equity holders.

3. You should examine other characteristics of the bond

Many bonds allow the issuer to recall the bond before the redemption date. Others give them the option of redeeming them for more bonds or even shares rather than cash.

You don’t want either of these if possible since they represent an uncontrolled risk to your investment returns.

In other words, you have to do your research.

In the case of Ladbrokes, I researched the company in depth and concluded there was a low risk in them going to the wall.

The fundamentals looked reasonable and they have a significant online presence, so they are somewhat protected from the effects of Covid-19.

Other investors seemed to agree. You can see the rebound in the price of the Ladbrokes bond below:

I took the decision to make an investment, buying in at £72 on the 24th March. I’m very happy with the return so far and that’s without yet receiving a coupon (the next coupon is paid on the 18th September 2020).

It’s not for everyone, but for me buying corporate bonds in a stock market crash is a strategy with an excellent risk-reward profile. That is, it has high potential reward and controlled risk.

[BoF: bond investing isn’t straightforward – and it won’t be everyone’s cup of tea.

Active bond investing is even more complicated (akin to active investing in the stock market).

That being said, Colin’s post above represents an excellent vantage point for those who may be inclined to dabble in bond investing – and take a view on a specific company as opposed to opting for a well-diversified bond fund.

As for me, the formula will remain 100% equities for a while – with a view to revisiting once I am closer to financial independence.

What I do know is that when revisit the topic, I better take the time to pick Colin’s brain!

Big thanks to Colin for the post – and a wonderful day to everyone else.]

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

Which platform would you recommend for bespoke corporate bonds Colin ?

i do my research using Sharepad……….there are some very useful filters built in which saves me a ton of time!

sorry I meant where can you buy individual corporate bonds ? Do you have a view on if it is worth investing in bond index funds when yields could increase ?

Ah, well I use AJ Bell as the dealing platform and buy them in either my SIPP or my ISA. it’s simply a matter of finding the bonds that interest you and then ringing them up to buy the bond. They’ll offer you an “at best” price or you can specify the price you are willing to deal at.

In terms of bond funds, I think they have their place in a portfolio but it depends on your individual circumstances. For example, are you wanting to grow your fund and have many years to retirement? is the stock market over or under-valued?

aS an example, in 2009, just after the financial crash, the markets were certainly good value and I would have decreased bond holdings and increased equity holdings as a result. I’m a great believer in risk based asset allocation in a portfolio.

Will have a look into this never purchased a corporate bond before, I like 100% equity. But will have to see if there are some bargains about!

I’ve not done it either but find the concept very interesting, especially as I approach my “bond investing” years.

Always good to take advantage of market dislocations like the one we’ve just gone through.