To reach financial independence, you need to overcome three key hurdles.

The first one is spending less than you earn. Inheritance or lottery winnings aside, this is the only way to eliminate debt and grow your savings.

Unfortunately, it seems that saving money is something more than half of us Brits are incapable of. I happen to have spent a big chunk of my life over in the States, and the picture isn’t any different there.

For those who manage to buck the trend, the second step is crossing the Rubicon and investing that savings pot you’ve built up.

History shows that as long as you stick to some very simple rules, it is practically impossible to lose money investing in the stock market.

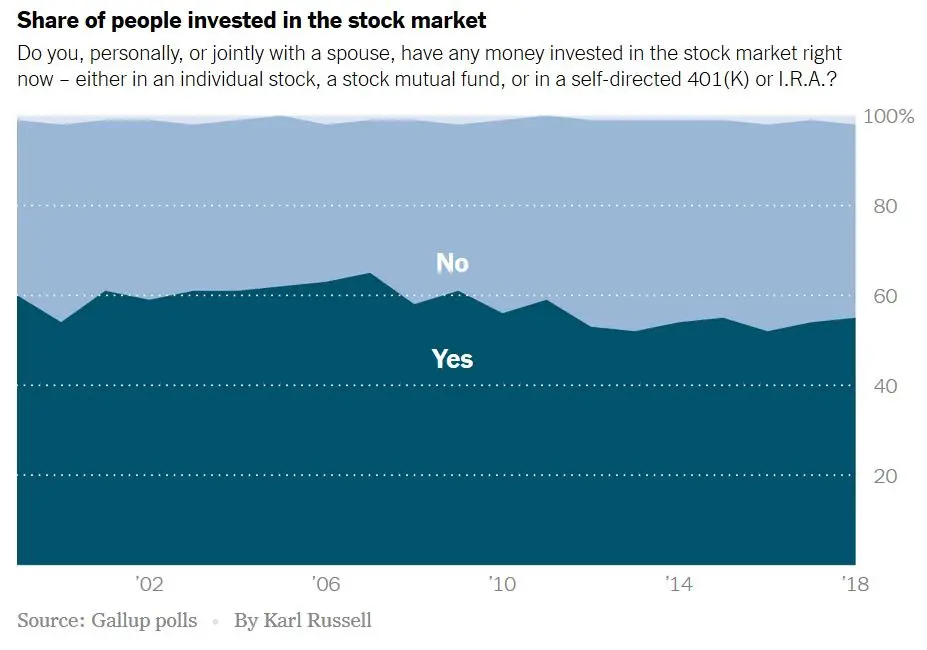

However, as you can see in the graph below, the proportion of people invested in the stock market today is at its lowest level in two decades:

They watch the stock market reach new highs while inflation is eating up the purchasing power of their hard-earned (and saved) cash.

After all, there is a good reason they call the current stock market cycle the most hated bull market in history.

But assume for the moment you’ve managed the feat of both saving AND investing money. Does this mean you can now set things on autopilot and rest easy?

ABSOLUTELY NOT.

The third – and final step on your journey is to minimize the investment fees you are paying.

This step might well be the easiest – but it is also the most crucial. If you aren’t careful, investment fees will wipe out many years of diligent saving and disciplined investing.

And the last thing you ever want to happen to you is to make sacrifices for years on end – just to see someone else reap the rewards of your hard work.

So what exactly are investment fees? And how do you protect yourself from people and organizations who are constantly trying to reach into your pocket and get their hands on your hard-earned money?

Understanding Investment Fees

If I had been writing this as recently as 10 years ago, the list of possible fees would easily fill a few pages.

Thankfully, it has gotten significantly shorter since then.

Front-end charges are finally becoming history. So are exit fees. And trading fees are steadily declining towards zero.

However, others remain. These days, the three investment fees you have got to watch out for as a hawk are:

- Ongoing Fees

- Investment Management Fees

- Platform Fees

Let’s look at them in detail.

1. Ongoing Fees

These fees are also known as Ongoing Charge Figures – you will often see them denoted as “OCF” in the investment marketing materials.

They are typically comprised of two components:

The first one covers the direct costs of managing the investment product itself, such as buying and selling stocks and administrative charges.

These charges typically add up to 0.05% to 0.15% of assets under management and they are usually quite legit.

The second, far more egregious category, represents the cost of actively managing your investments. On average, active management fees run at about 1% of assets under management.

But because active managers rarely outperform their benchmark indexes over extended periods of time, this fee is typically a waste of your hard-earned money.

Here’s a simple example.

Assume you invested £1,000 into an actively managed stock fund with a combined OCF of 1.25%.

By the end of year 1, the stock fund returns 10% or £100. However, you will also incur £12.50 of fees (1.25% * your £1,000 investment).

Net of fees, your return will only be £87.50, or 8.75%.

Compare this to a low-cost index fund with an OCF of 0.05%. You would only pay 50 PENCE in charges and get to keep £99.50 of the returns.

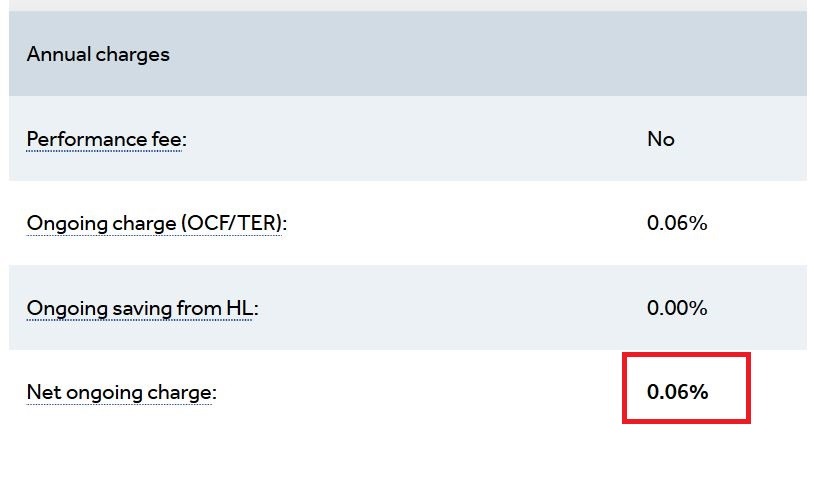

See below for an example of OCF for a S&P 500 index tracker fund from Fidelity:

As you will see further down, incurring excessive OCFs can make an absolutely astounding diffrence to the value of your investments down the road.

2. Investment Management (or Financial Advisor) Fees

OCFs are levied by the organizations managing the actual investment (i.e. running an actively managed stock fund or managing a passive index fund).

In contrast, Investment Management/Financial Advisor Fees are charged by financial advisors who tell you which funds to buy. It can be a private bank, a wealth management firm or any other person/organization that manages your money for you.

The pricing can vary widely, but it isn’t unusual for financial advisors to charge upwards of 1% of total assets under management.

To continue with the example above, what this means is they would charge you another £10/year for every £1,000 you had invested.

All of a sudden, your £87.50 gain has shrunk further to £77.50, or just 7.5%.

3. Platform Fees

Because the vast majority of financial advisors add zero to little value (and can often be counterproductive), Investment Management fees are a total rip-off.

You are much better off educating yourself on passive investing, forgoing a financial advisor altogether and buying low-cost index funds through an online brokerage.

However, the necessary evil here is going to be incurring what is called a Platform Fee. This fee is designed to cover the costs of managing the online “storefront” for the online brokerage you are using.

As an example, I have recently transferred my pension to a Hargreaves Lansdown SIPP. The platform fee for a SIPP is 0.45% of total investments under management.

While this is a punchy number on a headline basis, HL caps the fee at £200/year (if you hold shares, bonds, investment trusts or ETFs). Much more palatable.

When it comes to platform fees, it is good practice to choose providers with fixed absolute fees. As your investment pot grows in size, the platform fee will keep declining in percentage terms.

So now that we know what investment fees you need to watch out for, let’s take a look at how they impact your investments.

What Investment Fees Do To Your Investments

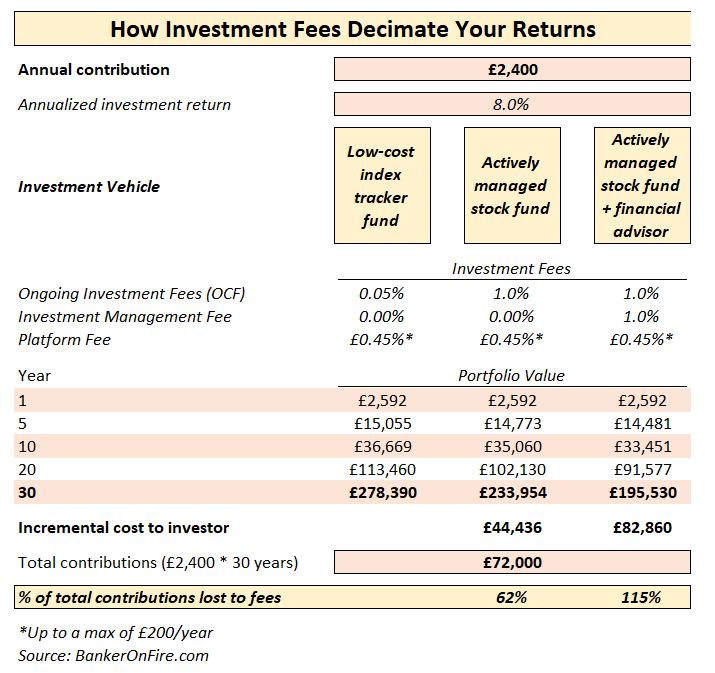

The chart below summarizes the returns an investor would achieve from three different investment vehicles.

In all three scenarios, the investor contributes £2,400/year and achieves an annualized return of 8% before fees.

In the first instance our investor sticks to a low-cost index tracker fund with an OCF of 0.05%. In the second instance, she chooses an actively managed stock fund with an OCF of 1%.

And in the third scenario, she also has a financial advisor who charges her an annual fee of 1% for the “service” of suggesting which actively managed stock fund to choose.

The impact on returns couldn’t be more dramatic.

Over 30 years, our investor will contribute £72k of her hard-earned cash. Had she invested in an index fund, she would close to quadruple her money over 30 years.

Choosing an actively managed stock fund costs her £44k in fees. You will notice I am being generous here by assuming the actively managed fund will perform in line with the index, which is rarely the case.

And in scenario 3, a combination of an actively managed fund with a smooth-talking financial advisor costs her an extra £82k in total.

Reflect on that number for a moment. Staggeringly, that’s more than the value of contributions she would make over 30 years.

How could that be? Well, not only you are losing the fees you are paying every single year. In addition, you are also forgoing all the returns you could have made on that money over the subsequent years.

This is exactly why simply investing in the stock market just isn’t enough. You should be watching your investment fees as a hawk.

So as we wrap up, let me leave you with the following advice.

Three Simple Steps To Avoid Excessive Investment Fees

-

Know what they are – and care about them

After reading this post, you should be sufficiently informed to avoid getting fleeced

-

Don’t touch active management with a ten-foot pole

Passive investing beats active. Even if an active manager manages to match or beat the benchmark index, the fees will most likely wipe out all the gains.

Sticking to a low-cost, passive index fund is one of the best investment decisions you could ever make.

-

Don’t hire a financial advisor

Take the time to educate yourself. Keep reading all the excellent personal finance blogs out there.

These days, buying a low-cost, passive index tracker fund is no harder than doing your weekly shopping on Amazon.

And if you must hire a financial advisor, hire one who charges an hourly fee. Have them reach into your pocket once as opposed to every year for decades on end.

Happy investing my friends!

Readers – do you feel like you are paying too much in investment fees? Or did you manage to reduce them by firing your financial advisor and switching to passive investing?

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

The ongoing charges figure includes the annual management charge and some admin costs, but it doesn’t include the manager’s trading costs. They go on top.

I think you should call ‘investment management fees’ ‘financial advice fees’, or something like that. Otherwise it sounds like the first category of fees.

The Hargreaves Lansdown cap of £200 doesn’t apply to open-ended investment companies.

Thanks Tim, good points. I’ve made the clarifications above.

Pingback: Six Reasons High Earners Fail to Get Rich - Physician on FIRE