Not too long ago, I published the “Silly Things Active Stock Market Investors Say” post. In it, I recounted some of the most popular excuses explanations people make when they try to justify an active investment strategy.

As expected, few of the popular excuses stand up to scrutiny. Low-cost, passive index trackers continue to outperform actively managed funds and the degree of outperformance continues to rise.

The hips numbers don’t lie

Ignoring the overwhelming evidence in favour of passive investing is like taking a butcher knife to your portfolio.

It may survive, but it sure won’t be better off.

At the same time, I’ll be the first one to admit that in a limited number of circumstances, active investing could well make sense. Let’s take a look at some specific situations where active money management has a higher chance of paying off.

1. Company Share Purchase Plans

As a general rule of thumb, you shouldn’t own shares in the company you work for. The reason for this is simple – if your employer ever fell on tough times, the value of your holdings would plummet – all while you are running the risk of losing your job.

Bad combination.

However, many employers recognize this risk – and try to sweeten the deal. It can be done through reducing the effective price employees pay for the shares, or eliminating the tax liability on the capital gains.

Here in the UK, participating in a Save As You Earn scheme allows you to capture all of the upside on your employer’s share price – without the downside risk.

This is as close as you will come to a free lunch in investing

This is as close as you will come to a free lunch in investing

Alternatively, you could also choose to participate in a Share Incentive Plan. A SIP is different from a SAYE in that you are fully exposed to the downside risk on your employer’s share price.

However, when you are offered two or three shares for the price of one, it may well be worth it.

2. International Equities

When it comes to US large-cap equities, outperforming the index is hard. There are literally millions of professional and individual investors making real-time decisions on the basis of readily available information.

What are the chances you can do a better job than highly trained professionals with access to cutting-edge IT infrastructure and potentially access to inside information? Slim to none.

However, the probability of outperformance increases as you turn to the less liquid markets with a lower degree of transparency.

Bring on the international equity markets. The reporting rules aren’t standardized (and typically less onerous). Quality information is tougher to come by and takes longer to filter through.

Most importantly, there are fewer people chasing the same buck.

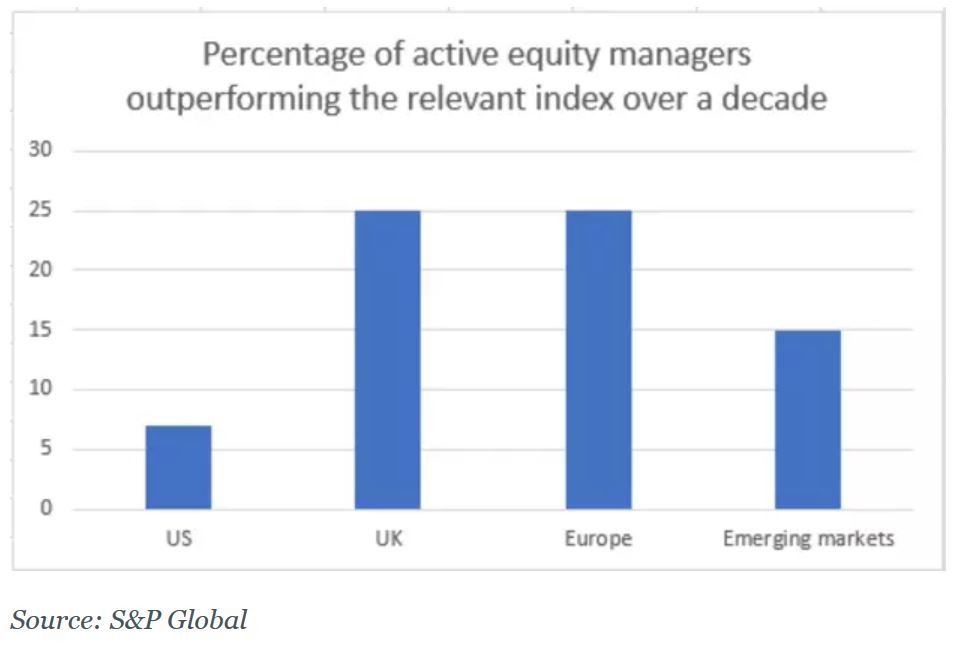

Therefore, it’s not a surprise that international equity funds underperform their benchmark index less frequently than those in the US.

Don’t get me wrong – the key takeaway from the chart above is that passive beats active across geographies. Only 25% of UK and European fund managers outperformed their benchmark over a decade.

When I put my own money to work, I’d much rather take a 100% chance of getting the returns on an index than a 25% chance of beating it by a smidge.

But if you are hell-bent on trying active investing, might as well do it in the UK, Europe or elsewhere outside the US.

3. Small Cap Equities

Many of the same factors above apply to small cap equities as well. In the US, these are defined as companies with a market capitalization of between $300 million and $2 billion.

These companies are typically too small to be on the radar of big, active money managers with billions of capital to deploy*. They also aren’t as well covered by the research community. This leaves more upside for those who are willing to do the work.

Finally, some very smart people came up with a theory that small-cap stocks outperform large cap stocks on a risk-adjusted basis.

Unfortunately, while active managers specializing in small cap stocks have had a decent run recently, their long-term performance is dismal. On a ten-year basis, they’ve done even worse than their large cap counterparts.

Talk about a lost decade!

So when it comes to small-cap equities, the best active management approach is to be a “closet” active investor and put your money in a small-cap ETF.

4. Investing For Fun

I hear this one quite often from active investors, which is why I am including it here.

Some people simply find the process of identifying, analyzing and investing in shares a lot of fun – which is an entirely valid approach.

Many of the same people recognize that the odds are stacked against them, so they put the majority of their funds into a passive index tracker and treat 5-10% of their portfolio as “funny money”.

To me, there’s absolutely nothing wrong with the approach above – just like there’s nothing wrong with going to the casino.

Just make sure to remember the odds, limit the downside and leave your credit card at home.

*The reason for this is that big money managers typically can’t hold more than a specific percentage of a company’s market cap (usually 5%). 5% of a $1bn company is $50m. If you have billions of dollars to deploy, you simply can’t do it in $50m chunks. This creates a possible market inefficiency in small-cap equities, though there are smaller money managers trying to fill the gap.

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com