I strongly believe that real estate is one of the most (if not the most) powerful tools retail investors can use to build true, sustainable wealth. Think of the well-off people you know or have come across in your life. Chances are, not only the majority of them own their principal residence, but they also have multiple other real estate investments in their portfolio.

There are different ways to play the real estate game. Over and above buying your principal residence you can invest in home builder shares and buy REITs. That being said, owning physical real estate for investment purposes remains one of the most effective wealth builders. This is the topic I want to cover off today – and I am going to use my own real estate investment as a case study to show how you can make 18% on your money over an extended period of time.

Back in 2009, my wife and I were a few years out of undergrad and lived in a large North American metropolis. At that point in time, we had been renting for about two years and our monthly outlay on rent was $1,600. Truth is, we didn’t know whether we will continue living in that city but we had some money saved up for a down payment and were tired of paying rent, so we decided to buy a 1 bedroom + den condominium in the same area we lived in at the time. We found a cozy new apartment in a newly built tower and managed to buy it for $339,000.

As luck would have it, exactly two weeks after we closed on the flat, I was accepted into one of the top graduate programs in the country. Coming from a state-school educational background, the opportunity to attend one of the most prestigious private universities in the world was too attractive to turn down, so soon thereafter, we packed our bags and moved south. Before we did that, we rented our place out to a nice professional couple in their late 20s. At the time, we had no idea that this sequence of events would result in one of our most lucrative investments so far.

I won’t bore you with the details but below is a summary of what has transpired over the next 8 or so years:

- We moved around a bit, first living in the city where I did my grad program and subsequently ending up in London

- Our initial tenants stayed with us for almost 4 years. We then rented the place out to another professional couple who stayed for 3 years. Since 2017, we have a new tenant – a single woman in her 40s

- While we have had to do some upkeep between tenants (including repainting the place and having it professionally cleaned), it required very little effort on our behalf. As my parents still live in the same city, my wife and I would visit the property every time we would be over there

- On average, our rental income fully covered our expenses (condo maintenance fees and property taxes, as well as vacancy and vacancy-related upkeep expenses) and our mortgage payment of c.$1,100 a month

- Most importantly, thanks to a growing population and decent economic growth, the rents have continued to increase, growing by about 48% in absolute or c.4.7% on an annualized basis

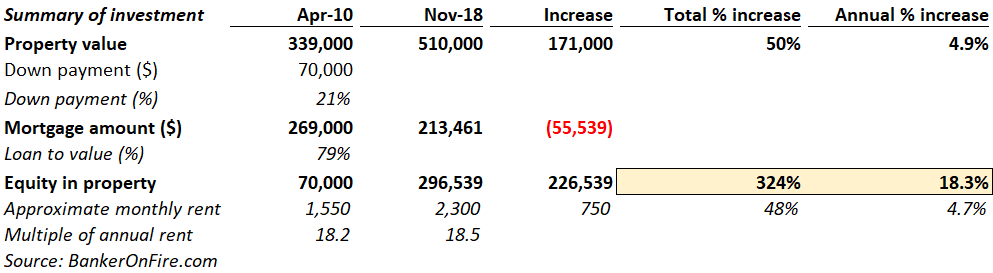

Because I was too busy working 80+ hours / week, I did not give too much thought to the property as an investment, though I did recognize that we are building up a substantial equity cushion in the flat. It was not until last year that I have finally decided to take stock of the situation and look at various equity release options. But before we go there, see the chart below for a summary of how things evolved over c.8.5 years:

Here are some key observations on the above chart:

- The property value has gone up by about 50% over 8.5 years. While the headline increase is punchy, the reality is that when you break it down by year, the annual growth was about 4.9%

- The key driver for the increase in property value was the increase in rental rates. When we had first rented the place, the going rate was c.$1,550 per month. In November of last year, it was $2,300. One of the key lessons in real estate investment is that over the long run, property values closely track the value of cash flows they generate

- As a result of making regular mortgage payments (100% funded by my tenants), the mortgage outstanding on the property has declined from $269k to $213k – a $56k reduction

- As a result of the factors above, our equity in property has gone up from the initial $70k down payment to $297k. This is about 4.25x the amount originally invested. Alternatively speaking, it represents absolute increase of about 324%, or c.18% when you annualize it

Have you made 18% on any of your investments recently? I sure haven’t! My stock market portfolio yields about 6%. My cash yields 1% on a good day. And even if I was able to invest in private equity funds, I suspect my return would be well south of 18% after all the fees and transaction costs.

Having generated so much equity, my mind turned to finding the best way to take some cash off the table. I quickly dismissed the idea of selling the place for a couple of reasons:

- I didn’t want to trigger a capital gains tax

- I didn’t want to incur a 3-5% fee for the real estate agent (which would work out to be anywhere between $15k and $25k)

- Most importantly, I felt that this investment will continue yielding good returns going forward. Why stop when you’ve got a good thing going on?

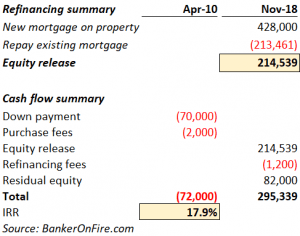

Having weighed all the pros and cons, I ended up refinancing the place. My bank extended a healthy $428k mortgage to me (more on this in part 2). The low equity investment implied by the c.84% loan-to-value means I can continue making outsize returns on my property. See below for a summary of the refinancing:

Once you factor in the fees, my 18.3% return on equity turned into a 17.9% IRR. Not bad for an investment that required about 5 days of work in total over 8+ years!

There’s much more to it than the simple summary above – after all, there’s only so much you can fit into a single post. Over the coming weeks, I will share much more detail and analysis with you. My hope is that you can use my experience and toolkit to amplify your own net worth using real estate.

Key takeaways for those of you who want to accelerate their wealth growth:

- If done well, it is hard to beat real estate as a vehicle for wealth generation

- Unlike private equity, venture capital, hedge funds or other investments in private vehicles, real estate is incredibly democratic. After all, how else could a middle-aged pair of schoolteachers make a £250m+ fortune?

- Real estate is a long-term game. Do not invest in real estate unless you have a 5+ year (ideally 10+ year) investment horizon

- Buy properties that let you minimize your transaction costs. If I needed to sell my flat instead of refinancing it, my fees would have been much higher – and my returns would be much lower. More on this in part 2.

- Make sure you have adequate liquidity to deal with any emergencies. At any point in time, you should have sufficient cash in the bank to fund at least 3 months of outgoings (mortgage principal and interest, property taxes, maintenance and upkeep etc.)

- Understand the numbers. The worst thing you can do is not to invest the time and effort to understand every single number that underpins your real estate investment. If you don’t, your chances of failing (i.e. losing money) go up exponentially

Stay tuned for part 2 where I will cover off the following topics:

- How property appreciation supercharges your equity returns – and how you can lose money

- What will happen going forward? Here is how I expect this property to make money for me in the future – and how much

- Why you should always seek to minimize your transaction costs

- The best book for real estate investment everyone should read

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

Thanks for the detailed post and an interesting read for anyone looking to get into real estate investing. I’ll be interested to read the next part and leant about potential pitfalls as well. Could timing play a part?

Thanks Paul.

I’ve done a few more posts on real estate investing since. One on the challenges you will likely encounter along the way: https://bankeronfire.com/the-challenges-with-real-estate-investing

And the next one on why it’s still one of the best ways to build wealth: https://bankeronfire.com/how-people-get-rich-with-real-estate