As I write this post, my stock app is flashing green all around.

S&P is up almost 4.6%, which apparently is its 11th best showing ever. Stocks, mutual funds and ETFs are up across the board.

The only exception is the VIX. Down about 17%, it denotes a significant reduction in volatility after last week’s heart-wrenching ride. And what a week it was.

Riding The Donkey

Imagine you are riding a donkey somewhere in the mountains of Croatia. It’s all great fun and the donkey seems nice and controllable as it takes you ever further up the path.

Then, all of a sudden, it gets unruly and begins moving in fits and starts. As you try to figure out what’s going on, it breaks into a gallop – and heads straight for the cliff edge.

Now, we all know that donkeys don’t typically commit suicide by jumping off cliffs. That being said, you could sure be forgiven for double guessing yourself when it happens.

What’s a sensible person to do? Trying to jump off it will sure look silly – and you will probably hurt yourself. However, it’s still much better than the alternative of careening off the mountaintop together with a crazed animal.

And that’s exactly what it felt like to be a stock market investor last week.

The Benefits Of Clarity

There’s a multitude of reasons why stock market downturns can be tremendously unsettling.

I’ve previously written about loss aversion, which makes us do all kinds of silly things that end up costing us money.

There’s also herd mentality. No one wants to look stupid in front of others, so we would rather participate in a modern-day equivalent of the buffalo jump.

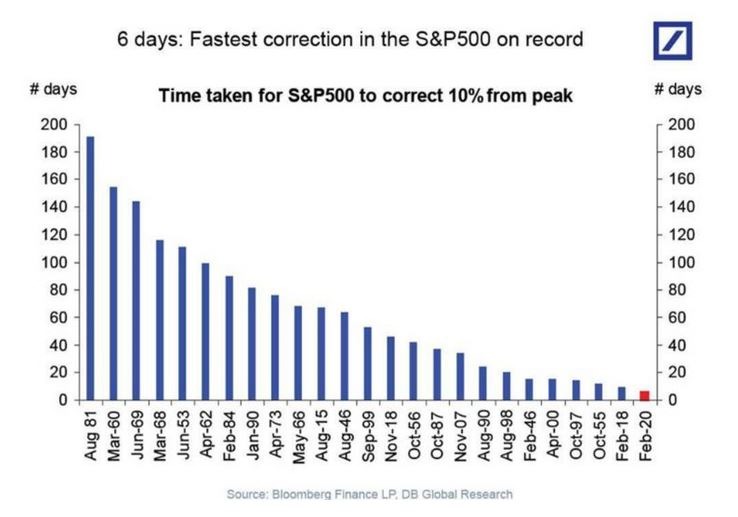

Admittedly, the speed of this decline didn’t help either. Apparently it was the fastest S&P 500 correction ever.

Blink and you will miss it

But fundamentally, the biggest problem when it comes to downturns is the lack of clarity.

Because we humans like clarity. We like to know what the future holds. And when stocks go up, we get perceived clarity that they will keep going up. Hey, 8% per year on average – that feels pretty good!

Of course, that clarity was never there in the first place – and any misconceptions you may have held disappear quickly when you are staring into the abyss.

But human nature is irrepressible. We like clarity – so we try to regain it. And the easiest way to do it is to jump off the donkey.

Yes, you will look silly in front of others. But selling the stocks and crystallizing the loss does provide clarity – because you won’t lose any more money.

At least that’s what you think. Because if there’s a sure way to lose money in the stock markets it’s to sell after a correction.

Today’s market performance is a textbook case study. Had you panicked and sold on Friday, you would have missed out on today’s ~5% gain.

Going For A Test Drive

At the moment, it’s too early to tell how things will shake out.

Last week could have been a harbinger of things to come – or an opportunity to act quickly and score some bargains in the market. Time will tell.

However, the true benefit of last week was the ability to gauge your emotions when going in the stock market finally gets rough. In other words, it was the benefit of introspection.

Ask yourself – how did it make you feel when the stock market went down 12.5% in just seven trading days?

Now ask yourself the following question: how will you feel when it goes down four times as much?

What if the value of your house goes down by 50% at the same time? And on top of that, you lose your job?

It has happened before – and it could happen again. Perversely, it would be the buying opportunity of a lifetime.

But will you really hold your nerve in that situation? Will you even contemplate clicking on “Buy” when visceral fear tells you to head for the nearest exit, no matter the price?

A Good Time To Invest

The unfortunate reality is that there is never a time when investing in the stock market seems like a good idea.

It wasn’t two weeks ago – because the markets were “too toppy”. It sure wasn’t last week – because it was too scary.

And it probably isn’t today – because who knows what’s going to happen next?

The numbers don’t lie – the prize in stock market investing is definitely worth playing for. But the only way to get it is to stay in the game. The best portfolio in the world won’t save you if you panic and sell in times of turmoil.

So the real opportunity last week wasn’t to lock in some gains before the market crashed – or to pick up some stocks on the cheap. It was to test your ability to stay in the game.

Because the next scary, bloody, gut-wrenching stock market correction is inevitable. But thanks to last week, you now have a good taste of what it feels like.

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

What’s your view on being fully invested vs having money on the side to buy the dip. I’ve got about 10k in cash which is really my emergency fund. Other than that I’ve got 11k in vanguard lifestrategy 40 which is there as first line of defence and for more short term things in say 5 years (replacement cars etc) other than that I’m 100% equities. Iive been very comfortable with the two dips so far last week and 2018 (and 2018 happened right after I lumped a 40k inheritance in one hit. Both times I reduced my emergency fund to add extra money as it went down.

I’m investing every month anyway and have as far as anyone can say a stable job but I do wonder whether I should be keeping more cash for opportunities. But then you miss out on the rallies. I think I’ve read basically the optimum is to be fully invested bar an emergency fund of 3 to 6 months but then how do you buy the dip other than smaller monthly amounts which are now a quote small % vs the amount invested

I think staying fully invested over time is the value maximizing strategy. Haven’t done the math myself but here’s a great read on the topic: https://www.personalfinanceclub.com/how-to-perfectly-time-the-market/

For people who are not 100% equities rebalancing from bonds to stocks in a downturn is the right way to go, but that doesn’t apply to you (or me as I’m also 100% stocks)

I’m not sure about my dad’s advisors. He said they’ve trimmed his exposure to stocks from 66% to 60 and will continue to reduce as market goes down Limits his downside slightly but to me that’s selling stocks and I thought the idea was to rebalance back up to his original allocation

That’s exactly the opposite of what they are supposed to do. If he has a certain % of his portfolio allocated to stocks and that % goes below the target, the idea is to sell other assets to get it back up.

I wonder how many advisors are doing this to their clients right now.