Note: This post was first published in May 2020 and updated in July 2021.

The stock market is a complex beast.

This is not entirely surprising. In a way, it should even be expected.

After all, it’s a mechanism that allows retail investors like you and I take a tiny ownership stake in large multinational corporations like Microsoft and Amazon.

In other words, it’s bound to be complicated.

The good news is that you don’t need to understand it to take advantage of it.

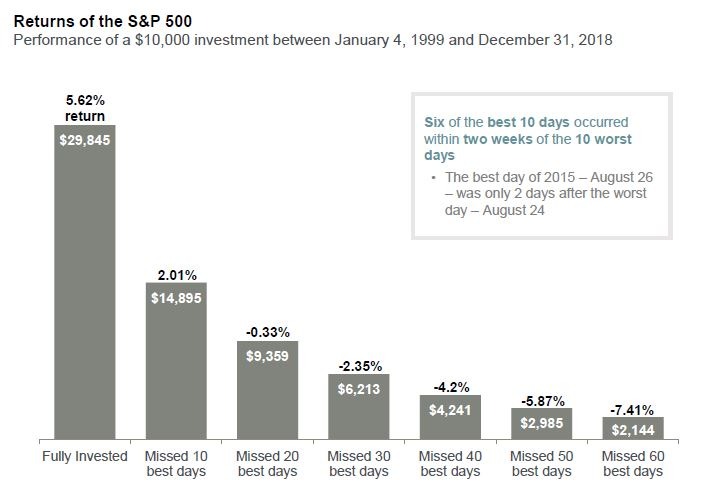

Much like an airplane in the hopefully soon-to-come post-Covid days, you just need to take a seat, strap in and enjoy the ride.

Yes, there may be some turbulence along the way.

However, it’s still the best way to get from A and B, provided you don’t freak out and do something silly, like trying to bail when things get shaky:

That being said, it’s not unhelpful to know how long your journey will take, what with those comfy economy seats, slightly annoying masks, and recycled air.

It’s the same with your investing journey.

As much as you might enjoy it, you probably want to reach financial independence sooner rather than later. And along with your savings rate, stock market returns are the most important determinant of how long it will take.

But what exactly is it that determines stock market returns over time?

With the stock market behaving like a rabid dog all most of the time, I can’t blame you for thinking there’s some kind of a random number generator at work.

In the short run, you are absolutely right. There’s simply no rhyme, rhythm, or reason.

In the long run, however, there is a broad set of principles that guides the market’s performance – and helps explain just how quickly your portfolio will grow in size.

Deconstructing Stock Market Returns

At the most basic level, there are three core components that determine stock market returns over long periods of time:

- Dividend yield

- Earnings growth

- Valuation multiples

If you are like most people, coming across this kind of terminology probably makes your eyes glaze over.

But it doesn’t have to be this way.

No, it doesn’t have to be this complicated

So before I reach for the defibrillator, let me try using a real-life analogy most people can relate to: real estate.

Not because I happen to like real estate as an asset class – but because it’s the most intuitive way to think about it.

So let’s go with the flow and imagine for a moment that you buy a rental property for 100k.

You pay for it in cash and rent it out with a long-term (say ten years) horizon in mind.

Let’s see how this simple operation jives with what goes on in the stock market:

Return Component #1: Dividend Yield

Assume that once all the expenses are accounted for, you clear 4k in profits every single year, which you promptly use to fund your family’s annual holiday to Mexico.

You can think of the 4k as your dividend. The dividend yield on your investment is 4%, calculated as 4k divided by the 100k cash investment.

The stock market works the same way. If you buy 100k worth of shares that have a 4% dividend yield, you’ll clear 4k in dividends every year.

And unlike real estate, you won’t have any operating expenses except for taxes.

So far, so good.

Return Component #2: Earnings Growth

As it happens, you notice the rents in the neighbourhood going up 3% per year.

Despite being a nice and agreeable person (and ignoring whatever The Guardian might tell you), you realize that increasing your own rental rates by 3% is also fair and square.

As a result, your 4k of profits increase by 3% every year, enough to pay for a nice dinner and a few extra margaritas in that beachside cafe on the Mayan Riviera.

You can think of this annual increase as earnings growth.

As your rental profits grow, so does the value of your investment.

When you originally bought the place for 100k, you essentially paid 25 quid for every dollar / pound / euro of net profit (i.e. 100k divided by 4k).

Now that the rental income has gone up to 4,120 (i.e. up by 3%), you should be willing to pay 103k for it.

Yes, that’s a 3% increase – in line with earnings growth. And that is exactly why stock markets tend to go up with time.

Corporations increase prices (have you seen how much the latest iPhone goes for?), which increases earnings, which in turn drives stock prices upwards.

Where it can get a bit confusing is that sometimes companies choose to hold on to some / all of their profits.

Hopefully, they do so in order to reinvest in the business and grow their earnings even faster.

An analogy would be you forgoing your annual holiday, using the 4k to refurb the rental property, and increasing the rent by 10%.

In that scenario, you are looking at a reduction in dividend yield (i.e. component #1 above) offset by a corresponding gain in earnings growth (component #2).

And so it all goes, fine and dandy… except that it doesn’t.

Because there’s a spanner in the works called:

Return Component #3: Valuation Multiples

This one can be a bit complex, so let’s lean on a wonderful analogy by Benjamin Graham to help explain the concept.

Suppose that at some point, a chap starts showing up at your door every single day, offering up to buy your rental property.

It’s all a bit annoying at first, but he is harmless in every other way and you are not obligated to transact with him, so you let him be.

After all, isn’t it nice to know how much your property is worth in case you do decide to sell it?

With time, however, you notice the fellow has got a bit of a manic-depressive personality to him.

Some days he’s bright and cheerful. Feeling optimistic about the world, he offers you 120k for the property.

But the following day, he reads a headline in the newspaper that throws him off. Perhaps something happened in the Middle East, or a certain election didn’t go the way he expected.

Upset and disoriented, he shows up at your door and blurts out a price – but this time far less than 120k. Let’s say it’s 80k.

By definition, manic-depressive patterns are quite unpredictable. So this behaviour goes on and on and on.

Some days, the chap is prepared to pay 30 quid for every pound of rental profits (120k divided by 4k).

On others, he barely gets to 20 times (80k / 4k).

Whatever the case, the price he is offering is often disconnected from reality – which is that you continue cashing in 4k (and growing) of profits every single year.

Well, the stock market behaves in precisely the same manner.

Sometimes it’s feeling optimistic and assigns a high value to corporate earnings. Other days it’s nothing but.

Take the S&P 500 as an example.

The ~500 companies in the index generate earnings, year in and year out.

According to folks doing God’s work over at GS, the combined 2021 earnings of the index (including those companies that will lose money) will land at about $193:

As of this writing, the S&P 500 index stands at roughly 4,347.

Thus, the implied valuation multiple is 4,347 / $193 or roughly 22.5 times for every dollar of underlying earnings.

For comparison, when the S&P went all the way down to 2,300 last year, stock market investors were only willing to pay ~16x (2,300 divided by $142 In 2020 earnings) for every dollar of earnings.

As you can see, there are two things that are happening here.

One is the variability in underlying earnings, which depend on economic conditions but ultimately go up in the long run.

The other one is the earnings multiple being assigned to those earnings, which oscillates widely over time:

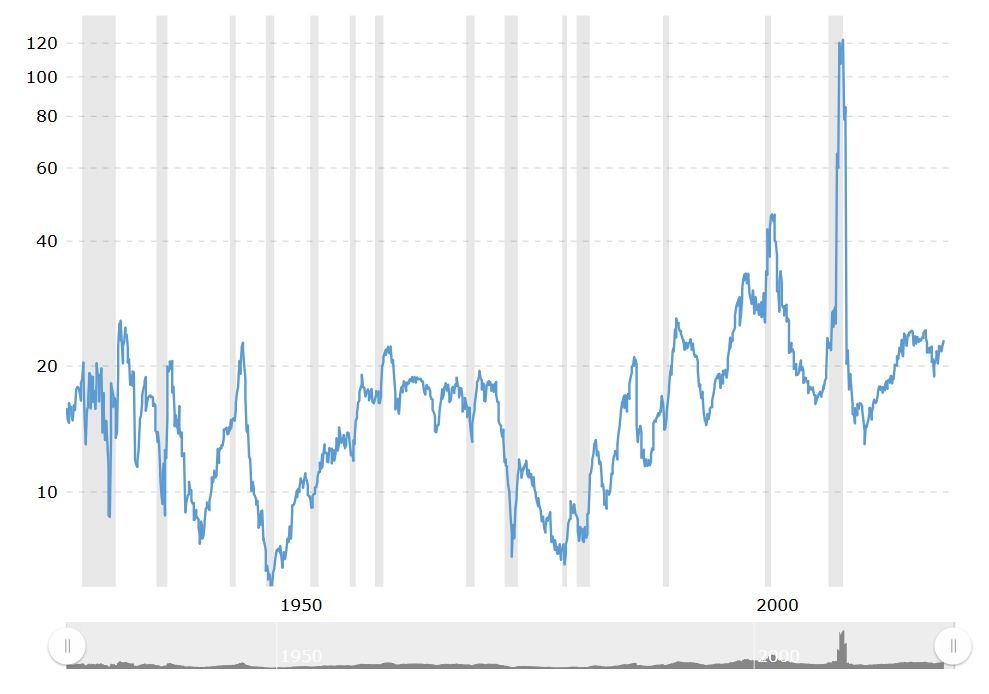

S&P 500 Price – Earnings Ratio For The Past Decade

When you zoom out and look at it over longer periods, you can see that the ratio fluctuates within a certain range, but fluctuations can be wide-ranging – and unexpected: Long-term Evolution Of The S&P 500 Price – Earnings Ratio

Long-term Evolution Of The S&P 500 Price – Earnings Ratio

Adding It All Up

You can see that if the chap in question stock market wasn’t so manic-depressive, figuring out your investment returns would be very easy.

Take the 4% dividend yield, add the 3% earnings growth and voila – you’ve got yourself a nice and respectable 7% return.

Unfortunately, in some years (i.e. 2019), the stock market feels absolutely exuberant.

Valuation multiples go up, the stock market rumbles ahead – and your return ends up being way ahead of 7%.

In 2020 other years, it’s the reverse.

The skies are dark, everyone is moody and valuation multiples tank. No dividend yield or earnings growth will save you.

Prices hit the gutter overnight, and you wish you never logged into your brokerage account to begin with.

And then, the clouds part, and the sun shines again in 2021.

Yes, there are nuances to the description above.

Both dividends and earnings growth fluctuate over time. And instead of going to Mexico, you’ve got to reinvest those dividends to buy more stocks.

Then there are the long-term secular trends that may cause valuation multiples to head in one direction or another for prolonged periods of time.

Part of the reason the US stock markets have knocked it out of the park over the past decade is the expansion in valuation multiples from c.14x to ~22x today.

Some of that has to do with market exuberance, in addition to the fact we have a much higher proportion of tech stocks in the mix these days.

But in the long run, it all averages out.

Dividend yields are largely dependent on the composition of the index you are investing in.

Indices that have more growth stocks (i.e. S&P 500) have lower dividend yields but higher growth rates.

Indices with a higher proportion of dividend-yielding stocks (i.e. FTSE 100) have higher yields – but lower growth as they reinvest a lower proportion of their earnings into the business.

But no matter the case, the answer stays the same: long-term stock market returns depend on dividend yields and earnings growth rates.

Yes, the stock market can lose its shit composure at moment’s notice, depressing the price-earnings multiple at a given point in time. But in the long run, it doesn’t matter.

No matter how helpful it may seem, successful investors learn to ignore that manic-depressive fellow showing up at their door every single day.

If you want to join them, you’ve got to do so as well.

Happy investing!

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

Thanks for all your efforts in writing a superb blog.

Do you search out markets with lower multiples to boost returns or do you stick to a strategic allocation?

Thanks for the kind words Stephen.

The discretionary part of my portfolio (i.e. excluding share awards me and my wife get from our employers) is fully allocated to US equities. This post lays out the reasons why: https://bankeronfire.com/the-case-for-a-100-us-equity-portfolio

However, I do have a chunk of that portfolio in US small-cap and value stocks. Reason for it is that I’ve actually met Eugene Fama and he’s convinced me of the merits of factor investing. That being said, this part of my portfolio has both underperformed the S&P 500 over the past 5 years or so AND has taken a bigger beating in the recent downturn.

I am confident the trend will revert but it may take years, if not decades. So… head in with your eyes wide open 🙂

This is great and really coherent – I’m really enjoying your content.

I’m fully agreed on the principles here. Invest for dividends and earnings growth rather than market valuations. This would also lead firmly away from investing in assets that don’t produce income such as gold, bitcoin etc as well as investing in companies where there is little inherent chance that they will ever be profitable in the longer term (e.g. Uber). In my mind this is the difference between investment and speculation and also points to investing in companies that have a strong track record of profitability and value creation over sustained periods of time.

With this in mind, is there a cogent case for investing in companies who are currently loss making based on the chances of future profit? I’ve made 1-2 picks where I think there is a strong business model that when fully realised will create strong profitability. Currently my portfolio has less than 1% allocated towards stock picking and is considered ‘fun money’ so I’m not betting the farm here, but keen to understand if this ever makes sense or I’m also speculating myself too.

Thanks Dave.

Plenty of fantastic companies out there that used to be loss-making at some point, so nothing wrong with that.

Real trick is figuring out which business models will prevail. I remember everyone falling over backwards for Uber’s “network effects” proposition. As it turned out, switching between apps is real easy, both for riders and drivers. A lot of VC money burned, and even more will be as they fumble around in the food delivery space.

On the other hand, Spotify, Amazon and many others did incredibly well. Who knows what the future holds…

And nothing wrong with active investing – as long as you keep it to a small part of your portfolio and head in with your eyes open 🙂

Really wish I knew and understood this years ago- rather than the past 3 or so when I’ve only really properly started on my path to FIRE. My parents lost some in the stock market crashes- I never really understood the fact that you can just wait it out. Still, it’s not too late for me, just going to take me a couple more years to get to FIRE.

Yes. In the absence of a more formal investing education as part of the high school curriculum, most people are left to discover it on their own.

Really too bad and a massive missed opportunity by the government.

Hi BoF,

Thanks for another great post. I am also a big Graham (and Buffet) fan, so it was great to read the Mr. Market analogy a bit differently.

You’ve often mentioned that you mostly invest in S&P500 ETF (VUSA). May I ask how are you investing in the market / what strategy are you using (for ex: dollar-cost averaging)? Do you ever look at SP500 valuation when buying?

I find it difficult to decide if I should just buy the VUSA every month regardless of the price (of SP500) or consider valuations too (when buying). Of course, the latter would be timing the market which I cannot and don’t wish to do. But still, this time I just really cannot grasp what the stock market is doing. I took a big advantage of the 30% dip, but to see where markets are back today just seems very very unreasonable. Not sure if I should wait till the next correction (which I think will come, but may not happen at all).

What do you do in times like this? Do you keep investing a fixed sum each month or wait it out?

Thanks and enjoy the rest of your Sunday 🙂

I typically invest as soon as possible, which means maxing out mine and my wife’s ISA / LISA allowance on April 6th of every year. Pensions are obviously quite different as they follow the cadence of the paycheque.

I think it’s fair to say that no one is finding it easy to wrap their heads around this crisis. Have a look at this post where I lay out our household’s current investing strategy: https://bankeronfire.com/how-i-am-investing-money-through-this-crisis

The Dollars and Data blog also has some excellent posts on why market timing doesn’t work. Worthwhile having a look.

nice article. I tend to invest monthly and at the start of the tax year in lump sums and as / when bonuses are received. The key to remember is that there are loooong periods of time when the stock market will do nothing. That’s the price of admission to what has historically been (and probably future too) the biggest wealth creating opportunity there is. The last 12 years have been no guide here – 2007/08 – flash in the pan. Ditto 2020 even though the % of decline was the swiftest ever recorded. One needs to read back to stock market history to fully appreciate this. mid 1960’s to early 1980’s – US index does nothing. That’s 15 years of watching your investments grow by considerably less than inflation. I wonder how many people will have lost the faith with VUSA by then the next time that happens saying index investing is dead! Ditto the 1930’s to mid 1940’s zero growth notwithstanding the US economy grew substantially. You need to mentally lock away that money for decades knowing that when you retire the likelihood is it will have grown substantially if you have say a 30 year time horizon – 5 years / 10 years is short term. Equally historically even though there’s been decades of zero nominal / materially negative real growth circa 4% withdrawal has been ok – I question whether anyone could handle that 15 year suck out. It would be mentally serious taxing. There is no cure really except (a) saving a ridiculous number (b) spending 1 / 2% per year – same as (a) (c) saving 10 years in cash – which is likely a very sub-optimal investing strategy (d) mentally becoming a vulcan. Which in a nutshell is why I haven’t pulled the pin. Real estate could be a good option though – we have a few BTL in the UK but the govt has done it’s best to make this a sub-optimal investment. How much do you think your performance in real estate is done to cap rates squeezing generally or good asset selection?

I think the FIRE community is in for a serious reckoning when the returns stagnate again, which they ultimately will.

As you say, takes a LOT of mental fortitude to keep the faith while watching your portfolio erode in real terms. Will also differentiated between the folks who have done their homework and the hail mary’s.

As far as real estate goes, it’s a tough one. I’d like to say it’s been more than just the cap rate compression (which has clearly been a massive tailwind).

That being said, a property investment thesis (as well as above-average management, especially when it comes to commercial tenants) can take 5-10 years to really prove out. It’s still early days here, though we’ve had some great wins in terms of repositioning properties / doubling lease rates / managing vacancy etc.

Pingback: Investing 101: Asset Allocation