Note: This post was first published in July 2020 and subsequently updated in October 2021

When I first moved to the UK about ten years ago, I remember being mightily confused by the concept of a self-invested personal pension, also known as a SIPP.

I ended up parking my mental questions on the topic when I realized that as a corporate employee, I was eligible for a workplace pension, one of the most powerful wealth-building tools in the world.

That being said, there are many people out there who don’t qualify for a workplace pension.

If you are one of them, a SIPP should rank very highly, if not at the very top, of your list of weapons of wealth accumulation.

So perhaps it isn’t surprising that over the past few months, I’ve received numerous inbounds via email and blog comments, asking me to spend a bit more time covering SIPPs.

With today’s post, I hope to clear up some of the confusion around the topic – and to explain how you can use a SIPP to grow that nest egg of yours.

To begin with, a few basic definitions are in order.

Self Invested Personal Pension Explained

At its most fundamental level, it’s quite simple:

A SIPP is just like a workplace pension – without the employer match.

Yes, there are some other nuances, but this is the critical difference. Which conveniently brings us to the next big point to remember:

You will always be better off in a workplace pension than a SIPP – courtesy of that very same employer match.

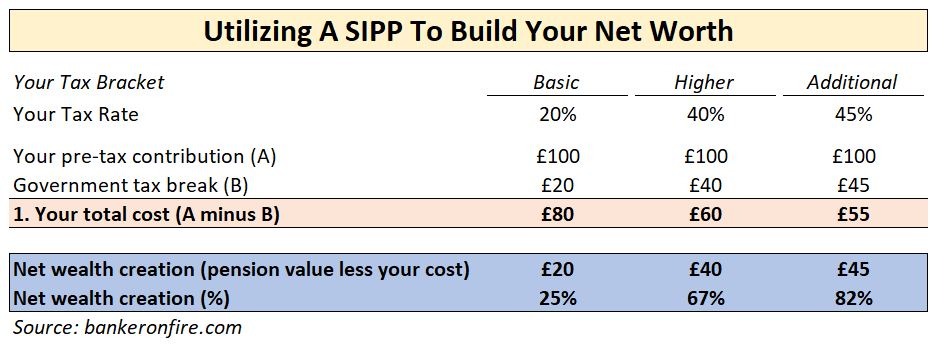

To see why, just have a look at my favourite table showing how workplace pension contributions lift your net worth:

And here is one showing the impact of the same contribution made through a SIPP:

Clearly, there’s a meaningful difference in your net wealth creation across every single tax bracket. In other words, you don’t say no to free money.

Now, this is obviously a moot point for most people. If you haven’t got access to a workplace pension, you don’t get to benefit, right?

Well, it’s not that simple. On multiple occasions, I’ve heard of people opting out of workplace pensions (or keeping their contributions to a bare minimum), because they aren’t happy with their employer’s pension provider.

Best Of Both Worlds

I have A LOT of sympathy for the sentiment above.

Sure, the asset management industry has come a long way – mostly a function of a surprisingly decent job done by the regulators.

That being said, we are not in the clear yet – and so you must watch out like a hawk to avoid getting ripped off by your workplace pension provider.

And while there are plenty of strategies to protect your hard-earned money, opting out of your contributions should not be one of them.

Instead, there’s an option not many people know of our use. It’s called transferring your workplace pension to a SIPP.

Yes, it’s possible (in the vast majority of cases). No, you don’t need to wait until you change jobs.

Once you’ve gotten that employer match and the money has been deposited into your workplace pension account, you can go ahead and transfer it out to a SIPP account.

Sometimes, depending on the amounts transferred, you may even score a transfer-in bonus (Hargreaves Lansdown run them once in a while and I think AJ Bell might too).

It is true that some providers will only allow a transfer out once a year. Even then, getting the employer match is totally worth it.

With that, let’s go back to the topic at hand and see how a SIPP stacks up versus other tax-efficient investment vehicles.

Self Invested Personal Pension vs ISA: Which Is Best?

If you are contemplating using a SIPP, you should keep in mind some interesting implications for your investing strategy.

Firstly, due to the tax break, a SIPP is highly likely to beat an ISA.

Similar to workplace pensions, you don’t get to access your money until you are 55 (rising to 57 in 2028 and possibly even higher in the future).

And when you do get to access your SIPP, you will only be able to take 25% of it as a tax-free lump sum. The other 75% will be taxed as income.

But assuming your tax rate in retirement is lower than it is today (as is the case with most people), you are better off in a SIPP.

What About A SIPP vs A Lifetime ISA?

This is an interesting one with a few nuances.

If you are a basic rate taxpayer, a Lifetime ISA will always beat a SIPP.

Have another look at the SIPP table below:

The way the numbers work, a 20% tax break works out to a 25% uplift on the money a basic rate taxpayer contributes to a SIPP.

Well, guess what – that’s precisely the government bonus you get on your Lifetime ISA contributions. Except, of course, any money in a LISA is completely tax-free on the way out, whereas a SIPP will likely generate some form of a tax bill on the way out.

In contrast, higher-rate or additional-rate taxpayers will always be better off in a SIPP.

In addition, here are some other considerations to keep in mind:

Access Age

You can only withdraw from your Lifetime ISA upon turning 60. At the moment, you can access your private pensions (either workplace or a SIPP), a few years prior to hitting that golden age.

Contribution Age

Importantly, you can only contribute to your Lifetime ISA between the ages of 18 and 50 (and that’s only if you opened an account before you turned 40).

There are no restrictions of that sort in a SIPP.

Contribution Limits

Using a LISA will only allow you to contribute £4k a year (you get a maximum £1k bonus on top).

On a headline basis, SIPP contributions are capped by the lower of £40k or your annual earnings. That being said, you can carry forward unused contribution room for three years.

You can also invest in a SIPP in years when you’ve got no income. Pay in £2,880 per tax year – and get a £720 top-up from the government to the tune of £3,600 in total.

Using A Self Invested Personal Pension To Invest In Property

Every once in a while, I come across an article that claims it is possible to put your buy-to-let properties into your SIPP.

No need to worry about interest tax deductions – or any taxes for that matter. Hey ho!

Unfortunately, the reality is more convoluted than that.

Yes, you can use a SIPP to invest in property funds, but that’s very different than using it to invest in that two-bed flat out in Essex (if you still wanted to do that, given how the UK government has treated BTL investors recently).

That’s where it ends, if you happen to be a self-employed freelancer taking advantage of a third-party SIPP platform.

However, as one of this blog’s awesome readers pointed it in the comments below, it gets much easier if you happen to run your own company.

As it happens, many folks who take advantage of SIPPs do just that.

The corporation makes a contribution to the SIPP on the behalf of the employee.

The company that administers the SIPP then uses the money as it sees fit – which potentially includes acquisition of property.

Gravy On Top

For those who run their own company, there’s another very important tax benefit: corporation tax savings.

The contribution that the corporation makes into an employer’s SIPP vehicle is tax deductible. As such, a £40k contribution at a 19% corporate tax rate results in £7,600 tax saving.

And given the option to carry forward unused pension room, the maximum contribution could be up to £120k. In other words, a nifty way to minimize taxes in a bumper year, all while securing the owner’s financial future.

If that isn’t enough reason to read up on the most boring subject in the world, then I don’t know what is!

And now, let’s get ready for some FIRE fast food.

The Fastest Way To Save £100k

The graph below compares the time it will take to save your first £100k if you use a SIPP as opposed to an ISA or a LISA.

As you can see, for a basic-rate taxpayer, the headline numbers are the same whether you use a Lifetime ISA or a SIPP (until you get to taxes on withdrawals).

The other obvious observation is that if you compare the numbers for a SIPP versus a workplace pension in the original post, the employer match does go a long way in accelerating your wealth-building journey.

But there’s no need to get disappointed, because things get rather easier from there onwards.

Here’s how long it would take to save the second £100k.

Guess what – the gap is shrinking. And on a relative basis, it shrinks even more if you were to set your sights on that lofty goal of £1m:

It makes total sense. Once you’ve accumulated that first £100k, compound interest means that the money your money makes takes over and the employer match becomes less relevant.

Revisiting The Self Invested Personal Pension vs ISA Debate

If you are contemplating early retirement, using a SIPP will also affect the way you should think about balancing off your SIPP vs ISA investments.

I’ve previously done a comprehensive writeup on it. No need to repeat it – but I did update the SIPP vs ISA file to eliminate the workplace match.

Play around with the numbers to zero in on the right strategy for you.

Closing Thoughts

A few other things come to mind.

The first one is that with a workplace pension, you typically get the right level of tax relief automatically, regardless of your tax bracket.

It’s slightly different with a SIPP. For basic-rate taxpayers, the government will make an automatic adjustment.

Higher or additional-rate payers will need to claim the extra tax relief separately, usually through the year-end tax return.

Then there’s the salary sacrifice. The construct means an extra boost for salaried employees in the form of breaks on NI contributions.

However, most people opting for a SIPP wouldn’t have NI contributions to begin with, hence the playing field is actually pretty even.

At the end of the day, there’s nothing complicated about a self invested personal pension.

Know the nuances, pick a strategy that’s right for you – and you’ll be well on your way.

As always, thank you for reading – and happy investing!

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

Awesome write-up, it’s really clear and, as always, love the charts.

I started both my LISA and my SIPP last tax year after reading some articles on here. They have grown really nicely since then, the top-up/ tax back really helps.

Since I’m young and potentially looking to draw down before age 50, I do prioritise my ISA over the other savings vehicles though. The current plan is to invest in:

1. LISA (relatively small amount, but big reward)

2. ISA (not age-restricted, so great for early drawdown)

3. SIPP (in a good year, if the others are maxed out)

Thanks Kat.

Definitely. Given your trajectory, you are likely to have quite a few years to bridge before you can access your LISA and SIPP, which is when the ISA will come in handy.

By the time you do get to tap into your deferred vehicles, the top up will represent a very meaningful addition to your portfolio.

I think there is another way to get your money out of a LISA, and that is when you use the money to buy your first home. it seems to me that if this is on your agenda then a LISA is a great way to save up the money!

Indeed, if you are a first-time homebuyer, a LISA is an absolute no-brainer.

Sadly given where house prices are, this might only be relevant for those living outside London!

Hi, thanks for a great post, which I have found particularly helpful.

I contribute the maximum to my workplace pension which is quite generous at 5% employee and 10% employer. This is the maximum match they will do, but I also save into a vanguard sipp. My only slight concern is potentially capping out the pension lifetime allowance, which in recent years has been coming down rather than going up! I am trying to consider whether I would be better off investing some of my surplus money into an ISA rather than my pension. What I don’t want to happen is that I hit the cap before retirement age and then get taxed heavily for further pension contributions. I have used your excel ISA v SIPP spreadsheet and calculate with 7% returns and current contribution levels, I will potentially hit the cap by age 47, which still leave 10 years before I can access it!

I am making the most of the pension tax relief whilst it lasts, as who knows when it might go! But in the future I may look to contribute more to my ISA.

I would welcome your thoughts!

A

The order seems to be:

– pension up to employee match

– ISAs

– Pension

– GIA.

The LTA is meant to increase by RPI / CPI annually (not sure if you’ve factored that into your calculations?) but it is still subject to massive political risk.

@Genghis – I agree with that sequence, except I’m not sure what a GIA is?

@Alex – You’ve got the right strategy in mind. The thing about pensions is that there are so many moving variables.

You may change employers and end up with a less generous program. For some people, there’s a stint of unemployment – or they knock it out of the park and get tapered down. More likely than not, the rules change and become far less generous.

All of the above points to the fact that you should take advantage of the employer match/tax break now as it might not be there in a few years. That’s when you can turn to your ISA.

Sorry. GIA = General Investment Account, ie a taxable account. Still really worthwhile especially up to £2k pa dividend allowance and to annually harvest capital gains, now £12,300, though requires much more record keeping.

Got it. Yes, fully agree with you – don’t want to miss out on the tax-free allowances.

Great article.

Some thoughts on workplace pension vs SIPP:

I’m an employed HRTP with a decent workplace pension scheme (0.12% OCF all in) and can invest in a globally diversified portfolio. I’ve no need for a SIPP currently. Every £100 in the pension costs me £58, or £38 (and even less given childcare benefit) on the element I earn over £100k.

My wife, a part time employee, is a BRTP with a more expensive workplace pension (0.5% OCF). She has a SIPP. But the workplace pension is in a salary sacrifice set up. She saves 12% employee NI and her employer gives her half of the 13.8% employer NI into the pension. So £106.90 in the pension costs her £68 or to equalise it £100 in the pension costs £63.61. This contrasts to paying into a SIPP for her as a BRTP where £100 in the pension costs £80. So putting the cash initially in the workplace pension and then transferring annually to a SIPP, she’s much better off. There is some “time out the market” risk (takes about a week to transfer) given no in-specie transfer available but for us it’s a risk worth taking.

Thank you.

What you lay out above is exactly the right logic to follow. Figure out your “effective cost” per £100 of pension value. Start off with the lowest cost vehicle and then move money around once you’ve got the initial top up.

The time out of the market bothers me as well, but it has never been more than two weeks in the past, so something I am happy to live with.

Hi Banker On FIRE, I’m really enjoying your postings. I’ve made my way through from start to finish over the last couple of weeks. Keep up the good work.

The concept of partial transferring a workplace pension to a SIPP is an interesting one. My workplace pension has good developed market index funds but really expensive Emerging Markets and bond funds. I was looking at doing a partial transfer to a SIPP to benefit from a wider and cheaper fund selection. However I was scared off by my workplace pension raising that I would lose some Protected Tax Free Cash (PTFC) rights.

I haven’t been able to find out much online about this and the information as to how much this would be worth to me was really sketchy. I assume there are disadvantages to transferring out where the rights lost would cost more than the fees saving in the SIPP? But without all the numbers it’s difficult to know whether to go ahead with a partial transfer or not.

Thank you.

Your question is a tricky one and unfortunately I haven’t got enough information about your specific pension plan or the topic of PTFC to form an opinion. It may well be better to stay put and avoid losing some potentially valuable benefits.

However, a safer strategy may be to prioritize the developed market index funds in your workplace pension and allocate your ISA investments (if you have any) to EM and bonds?

You can also raise the topic with your pension provider and see if they would be open to adding lower-fee EM and bond funds to their selection. Sometimes they are surprisingly amenable to suggestions (even though they can take a bit of time to act on them).

Hope this helps!

Thank you. Yes I have spoken to the pension provider but they unfortunately weren’t interested in adding lower fee funds. Some of the funds have fees as high as 1.3%!

I had also thought of using my ISA to balance me out a bit but ideally my ISA is there to help me retire early, and I wouldn’t have a way of de-risking the pension pot prior to accessing it. I will keep digging, but thanks for your reply.

Would be great to know how you get on.

Am sure others are in a similar boat so please do share a solution if / when you find it.

Excellent post as always, keep it up.

I think you are missing an important advantage of SIPPs, corporation tax savings.

Let’s make the broad generalisation that people with a SIPP are more likely to run their own company. I know I am.

The company (which I own) pays the maximum of £40K into the SIPP (or whatever figure works for you). As a result the corporation tax for the company is reduced by £ 40K as pension costs are pre-tax, a saving of 19% = £ 7600. You’ll see this saving back when you exit the company (minus CG tax). No personal tax to pay, no NICs to pay on either the personal side or company side.

There is no personal pension contribution, the company pays it all.

How does this scenario change your tables?

Thanks Jay, appreciate it.

That’s a great observation. Admittedly I’m less familiar with the corporate tax implications of SIPP contributions but they are clearly meaningful. Not everyone runs their own company but the tax benefits are a very strong point in favour of incorporating.

Perhaps a topic for another post, once I sharpen my pencil on corporate taxation here in the UK.

You also have your carry forward pension allowance. I recently did exactly what you say above. Company makes a “contribution in its own right” (an important term)

Your company can potentially use up all the current and previous 3 years pension allowances (if you have not contributed at all (160k each for you and wife)

The accountant did warn the government can question it but it is within the rules.

I don’t really contribute that much to my SIPP as I hope to be financially independent long before.

I am 22, so obviously a big concern for me is how much tampering the government can do with the withdrawal age before I get there.

The opportunity cost of using an ISA instead is missing out on the tax relief which will obviously have a HUGE impact over the long term.

Great post, stay safe!

Your logic is sound but the reality is that you will need a certain level of income after turning 60.

Using a SIPP or a workplace pension is a great way to “de-risk” those golden years and then start working backwards, filling up your ISAs and chipping years off your retirement age.

If only I was 22 again! 🙂

Great article – I think an under-utilised benefit of a SIPP is that people who run their own businesses can use their fund to buy commercial property, so they effectively pay rent to their own pension fund. I understand they can even borrow an additional 50% of the fund for the purchase (weird sort of mortgage I guess).

Whilst we can’t buy residential property using a SIPP, I think you mentioned you bought an overseas BTL (presumably from non-pension funds). Would you consider writing an article about that? My crappy BTL is doing nothing and it’s very difficult to find value opportunities in this country atm.

Thanks Rob. I wasn’t aware of the option you reference – always intriguing to explore the various options that exist even within the relatively rigid UK tax code.

On BTL – yes, I’ve actually got something in the works on that. Might take me a few weeks to get over the line but watch this space.

In general I agree with your sentiments re workplace pensions/SIPP’s. However, it is always worth closely examining your individual details and any potentially looming issues such as the LTA (mentioned by Alex above). An interesting case in point is documented at:

https://gentlemansfamilyfinances.com/2018/10/11/pay-less-into-your-pension-to-retire-early/

pay less into you pension to retire early is a fantastic post – excellently written and a veritable masterclass in financial blogging – so thanks for posting it.

However, a few things to point out. I’ve put a lot of money into my pension with salary sacrifice to the point of being paid a notional minimum wage for a few years in my old job.

All the while my monthly outgoings were higher than the family income meaning that we were well off for pensions but poor for pre-pension money (which you need to FIRE in any sense of the word).

I think that what BOF says is largely correct and pensions (SIPPs not your workplace crap) are the way to go but it does rely on you taking money from earnings and putting it into the pension. If you (like me) have excess funds outwith of tax-free wrappers – different circumstances apply. As too when you are a company director and you can choose between salary, dividends, pension…

Finally on transferring out of a company pension – I used to do it every few months or so when there were bonuses for transferring. People seem to think that you are stuck with your provider but that it definitely not the case (but the providers don’t make it easy for you to leave no – and why would they?)

https://gentlemansfamilyfinances.com/2020/02/28/bye-bye-aegon/

GFF, thanks for amplifying/clarifying

I think that makes sense. The way I look at it, once you’ve got a fair stash in your pension vehicles and are in a position to retire before pension age, you’ve got to start loading up on your ISAs.

If not, you’ll need a different strategy to “bridge the gap’.

Enjoyed the two posts from GFF, thanks for sharing!

No problem.

Fairly recently Monevator penned a multi-post series (that is yet to conclude) on this subject, see

https://monevator.com/how-to-maximise-your-isas-and-sipps-to-reach-financial-independence/

Thank you – I think Monevator’s work on this topic is some of the best I’ve seen.

I actually referenced it as required reading in my own post on pensions vs ISAs: https://bankeronfire.com/pension-vs-isa-settling-the-debate

IMO, Monevator is one of the very best blogs in this field. The posts are generally to a very high standard and often the comments are so useful that they too become essential reading.

Of course, BoF is pretty good too!

The Monevator post you reference is a straight pensions vs ISA post, whereas the one I called up is on how to use them together in the event of wanting to “pull the plug” before an individual is eligible to access his/her pension.

Not sure whether I’m missing something here, but with the employer match in a workplace pension, the table lays out your contribution of £100 and then has the employer match at £60. This would have the employer matching 60%(!) of your contribution, and not the 3,4,5 etc% they actually match. Have I spotted an error, or am I missing something?

Not quite. I think you are mixing up contributions and earnings. Here’s a breakdown:

Employee contribution usually works out to 5% of earnings (4% out of pocket and 1% tax break assuming a basic tax rate).

Employer contributes 3% of earnings. This works out to 60% of your contribution (3% divided by 5%).

So if your monthly contribution is £100, the employer’s contribution is £60.

Hope this helps!

Hi BoF,

I recall reading elsewhere that you are a dual UK/US citizen. Would you mind sharing how this affects your ability to invest within an ISA and SIPP? My wife is a US citizen, UK resident (and, hopefully, UK citizen in a few years), and we’re looking into the best ways for her to invest.

I’m aware that ISAs are not recognised in the US, so there’s probably no point making use of her ISA allowance. Looking online, workplace pensions appear to be safe, and I’m seeing mixed opinions on SIPPs. Have you encountered any problems when trying to open a SIPP?

Thanks,

Dr F

Hey Dr. F.

There are some nuances there which I would rather not share on the blog in public. The short answer is we are able to make full use of ISAs and SIPPs, but you probably need to consult an accountant.

Shoot me an email if you want to talk through in greater detail.

Good article, I’d advise people to ensure that if they are 40%+ taxpayers then that is being handled by their workplace pension – my workplace scheme doesn’t, so I need to mention it on my tax return. Don’t just hope for the best.

Very interesting and good point. Definitely worth a double take.

Great post well worth another read.

You’ve demonstrated really powerfully a key strategy that I think a lot of people miss when planning for FIRE. That we should try and view our working lives as a whole rather than from year to year, when planning to optimise tax and investment strategies.

For Example. I am of the opinion that individuals that are currently basic rate tax payers but in all likelihood are on course to become higher rate tax payers shouldn’t be making AVC’s into their pension. Instead they should be saving into ISA’s / LISA’s. At the point they become higher rate tax payers they should start increasing the AVC’s to maximise the benefit of the tax relief, particularly so for Sal Sac contributors.

There are also nuanced strategies for parents whom can control their taxable income via pension contributions to maximise child benefit payments. I currently implement a strategy of 2 years minimum pension contributions (just sufficient to receive the employer match) where I don’t receive child benefit. Followed by a 3 year period maximising the carry forward allowances to reduce my salary to a point where I do receive child benefit. This also has the happy side effect of reducing cost for any other taxable benefits such as private healthcare by moving yourself from a higher to a basic rate tax payer.

Thanks Rosario, and I fully agree with you

Quite a few other possible scenarios there as well, such as:

– Tax planning at the family level. If one spouse is in a higher tax bracket, much better to “route” AVCs into his / her pension to max out the tax break

– The trade off between utilising ISA and pension room. You have 3 years to catch up on pension contributions (and the associated tax benefit), but once the ISA limit is gone, it’s gone for good

– Defusing capital gains on your shares but taking advantage of the CGT every year

– and so forth

Problem is most folks find tax mightily confusing (and it sometimes is, partially by design). As a result, a lot of money lost to the taxman…

Yes lots of avenues to explore.

Agreed on the confusing design. It doesn’t help that the government often takes different approaches depending on whether they’re taking (individual) or giving (jointly as a couple) in order suit themselves.

You’re right there is a lot of waste (money lost to the taxman) in personal finance but that also means there is a lot of opportunity. Speaking from my own experience I’ve found the return on time invested here can be huge.

Another great post, BOF!

I’m glad you pointed out workplace pension transfers as that is a neat trick I discovered earlier this year. I’m extremely lucky in the fact that I get a 12% employer matched contribution and benefit from employer NI savings into my monthly pension payments.

I decided to do a partial transfer into II, so effectively paying 0.1% on my contributions (considering both SIPP and ISA values) compared to 0.6% in my workplace pensions. This saving will be fairly large over my investing horizon so well worth considering. Rinse and repeat every 6 months.

Another advantage of this is giving you access to a much wider variety of investment choices (Index trackers of course!) compared to some workplace pensions. Mine for example is fairly average compared to the likes of II or HL.

Cheers,

Dan.

Cheers Dan. I agree, you get meaningful savings in terms of fees and a much better selection of investments.

Compound this over a 30+ year working career and the differential can be massive.

One wrinkle, however, is that not all employers allow you to do this. Out of the three companies I worked for, two allowed me to transfer the pension out. The third one took a real stand to say that I can’t transfer out as long as I’m an active participant of the plan.

My employer does not offer a match, only the min required. As such, I pay the min amount into the work place pension, and any extra I pay into my SIPP.

I’ve enquired with the pension provider in the past (Now Pensions) and they always tell me that I cannot transfer funds from them without closing the scheme. Is there anything to be done here?

I doubt it. I had this issue with one of my employers, who were running some kind of a peculiar scheme that prevented me from transferring my pension out for as long as I was an employee.

Was quite annoying but I never had the time to look into it and properly challenge them. Thankfully it only happens in a minority of cases.

@Banker, I’d love to understand in some more detail how you see the Lifetime Allowance and where this factors into pension planning. I’m a while off currently (£200k in pensions, 39 years old), but based on all the projections I can run, I’ll shoot a long way over.

My current thinking is that it is still worth taking the employer match/employer contribution, but when hitting it becomes inevitable cutting to the minimum personal contributions. Maybe something to think about in a future blog post?

@ Dave

So we are in a similar boat. I’m 40 with c.£250k in my pension, my wife is a few years younger with £200k.

I am sadly tapered down to £4k a year, so chances of blowing through my LTA over the next 17 years is slim.

My wife has more room and continues contributing. However, she will probably leave her job at some point to spend more time with the family, so I don’t think she’ll hit the taper either.

Most importantly, we’ve got aspirations of retiring early. Now that our pension years are de-risked through pensions / real estate, the focus is on bridging the gap and hence we are channeling more money into ISAs and some more property investments.

And yes, the question you raise is one I’ve been mulling over. Too many ideas, too little time!

Hi, Banker on FIRE!

I have a question about the SIPP, and I’m not sure whether this has been covered anywhere.

This tax year, I will be a higher rate tax payer for the first time. I know that I need to claim back the tax from my SIPP contributions when doing my self assessment. But how do I actually access the money? Is it just deducted from the total tax I have to pay, or is it sent to me or credited to my SIPP?

Apologies if you’ve already covered this. I couldn’t find the answer here or on other sites.

Hi there – it’s actually pretty straightforward

“If you pay higher rates of tax, you’ll usually need to complete a self-assessment tax return to claim higher-rate tax relief. Then the money will be paid to you personally and not into your pension.”

See: https://www.hl.co.uk/pensions/tax-relief

There’s a link there for more information as well

Thank you very much. That’s helpful!