Conventional wisdom dictates that you should always look to maximize your income. Unfortunately, conventional wisdom is also often wrong.

Instead of maximizing your income, you should be optimizing your income. You should also expand the definition of income to capture all household income as opposed to just yours.

Today, I want to explore how quitting your high paying job and taking up a lower-paid one can be beneficial to both your finances AND your life.

Intrigued? Read on to find out more.

If you are the typical high earner in the UK and especially if you have children, chances are that your spouse is a stay at home parent.

No one argues that having someone who can focus their efforts on looking after the children and managing all the household chores is incredibly helpful.

Unfortunately, the way our tax system is set up here in the UK means that a family set-up where only one parent works very often leads to a severe tax disadvantage.

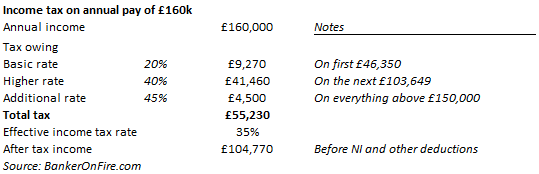

For purposes of this article, assume you are that high earning individual – let’s say with annual pay of £160k.

This level of earnings means there’s a high probability you are working 60+ (if not 70+) hours a week, with weekends and holidays fair game for work-related disruption.

Moreover, given the way our tax system is set up, there’s a 100% probability that you have used up your entire personal tax allowance of £12,500.

In addition, you have also and have triggered the 45% additional tax rate on income above £150k. And to top things off, you have also lost £5k of your annual £40k pension allowance.

When the time comes to file your taxes, you are looking at a whopping tax bill of £55,230 – a 35% income tax rate – and that’s before National Insurance and other deductions.

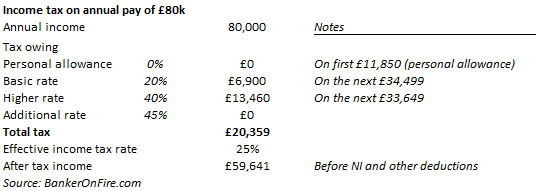

Now let’s take a look at the tax bill for someone working a £80k job.

While this can still be considered a high paying job (even though it might not feel like it, especially if you live in London), the tax burden is dramatically different.

At the end of the year, this person is only paying a 25% tax rate – c.28% lower than the 35% rate in the example above.

So what if you decided to resign from your high flying, stressful, yet high paying job with the intent of you and your spouse/partner/significant other both getting jobs at 50% of your previous income?

Well, guess what? Courtesy of our tax system, you would increase your cash flow by almost £15k per year! That’s right – your total pre-tax income would stay the same, but your combined tax rate will decline to 25%.

That is some serious money – almost enough to cover off private school tuition for one child. But that’s not where it ends.

Let’s run through the reasons to quit your high paying job:

1. More money due to lower cash taxes

This one’s a no-brainer. Not only you are saving c.£15k in cash taxes every year for the foreseeable future, but you are also going to reclaim a portion of your pension allowance – a valuable tax benefit in itself.

2. Even more money due to lower spending

That’s right. Let’s not forget that having a job that gives you more free time can lead to considerable additional savings.

Why? Because now that you have time to help with the children you may finally be able to swap that expensive nanny for a nursery.

Because now that you no longer have to live as close to your office (to actually get some sleep on the days when you work past midnight) you can get a nicer place in a cheaper area further out.

Most importantly, because now that you are no longer constantly pressed for time you can stop making so many suboptimal / impulse purchases.

3. Better quality of life

This one speaks for itself. More time for working out, more time for your children and family.

Most importantly – more time to spend with your husband/wife/partner, mitigating that nasty prospect of divorce down the road because you have grown distant while you spend all of your waking hours in the office.

4. More time for a side hustle

You better believe it. You will be impressed at what you will be able to achieve once you are used to working 80-100 hour weeks and then transition to a “regular” job.

If you ever wanted to start a business or a side hustle, you will finally be able to do it. Let’s not forget that in addition to pursuing something you really care about, a side hustle can give you very tangible tax benefits (but this is a topic for another time).

As with anything in life, there are drawbacks.

Below are the reasons NOT to quit that high paying job and stay in this modern indentured servitude for a while longer:

- Your partner isn’t able to get a job that will keep your combined income unchanged

- You are on partner/MD/C-suite track and expect your compensation to increase further still

- You will miss the fast pace/excitement/challenge of your current job

- You think you won’t be able to add as much value around the house as you can in your job

- You won’t enjoy spending more time at home (believe it or not, I’ve met many people like that)

- Perhaps you just like paying extra in taxes while being away from your loved ones?

Readers – what do you think? Would you switch to a lower-paying job to save money AND improve your quality of life? I would love to hear from you in the comments section below.

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

Great article and so true. i think that people don’t realize the effect of taxation, even in a relatively low taxation country like the UK.

Thanks Colin. Indeed – no wonder that working can sometimes leave people feeling like they are spinning their wheels without really getting ahead financially.

PS: You’ve got the distinction of leaving the very first comment on the very first post of this blog!

anywhere you’d recommend for decent tax advice/optimisations?

I’ve got an accounting background and my wife used to be in tax, so we just pick up the latest tax guide.

If you haven’t got a background in accounting/finance and don’t feel like learning from scratch, it may be best to consult with a decent tax accountant, at least at first.

It may cost a few hundred quid but savings, compounded over the years, will likely outweigh the expense by a stretch.

Interesting read Banker on Fire. Surprising how quirky our tax system is but definitely food for thought.

Some countries have spousal tax deductions, but not the UK. There are some things you can do at the edges to minimize your overall household tax bill, but it’s nearly not as flexible as the US tax system.

That being said, while the UK system isn’t perfect it actually isn’t that bad compared to most of the other G-7 countries.