Back in the heydays leading up to the global financial crisis, the same scene would regularly play out at the Deutsche Bank London headquarters.

On bonus day, a car transporter would pull up to the landmark yellow building at 75 London Wall. It would be loaded with Aston Martins – a sweetener reserved for top performers.

Make no mistake – this wasn’t a bonus. Rather, the car was an addition to an already sizeable, pre-crisis-level, investment banking bonus.

The size of individual bonuses is hotly debated but rarely disclosed. Not so much for the car, which can serve as a clear distinction between the people at the very top of the pecking order and everyone below them.

Thankfully (and yes, it’s a banker saying this), those days of greed and excess are now gone. So are many of the characters perpetuating the questionable culture of those days, making the finance industry a much more enjoyable and rewarding place to work.

However, the conundrum faced by investment banking managers back then is still very much alive and can be boiled down to the following question:

How do you make your employees work as hard as possible while paying them as little as possible?

Now, the words “as little” and “Aston Martin” hardly belong in the same sentence – but let’s come back to this concept slightly later.

The Never-Ending Battle

Back in business school, one of my professors argued that, theoretically, the best way to motivate employees was to pay them “unexpected amounts at unexpected times”.

Apparently, not knowing when the next paycheque will come – and how much it will be – is the most effective method to keep us office peons on our toes.

Luckily for all of us, it is also highly impractical.

After all, real life has things like regular mortgage payments, grocery bills, and car payments. Tough to motivate old Joe to keep showing up if his house gets repossessed and his kids go hungry.

Back to the drawing board for all the HR managers out there.

If you cannot vary the pay in an explicit way, might as well do so implicitly. In other words, keep your employees on the edge with the threat of firing them. Keep that sword of Damocles hanging over people’s heads.

Then again, fear and intimidation, effective as they may be, don’t exactly create a loyal workforce with a long-term perspective in mind.

So what’s the solution?

Our Worst Enemy

The good news for employers is that in the fight between capital and labour, capital has two big advantages.

The first one is inflation. Like it or not, price levels rise by 2-3% every year. Sometimes a little less. Sometimes much, much more.

Given that professions where pay rises are linked to inflation are disappearing faster than the white rhino, this means that employees typically start every year at love-fifteen.

They simply need that pay raise to just stay afloat.

However, being pretty damn good at self-sabotage, we then net another easy forehand. That unforced error?

Lifestyle Inflation

While monetary inflation pushes up the cost of living, lifestyle inflation supercharges it. If you get a 3% pay raise and inflation was at 3%, you don’t get to buy more stuff. But most people do.

Most people who have worked in investment banking (certainly on the advisory side) have probably heard of the book Monkey Business.

It’s a highly entertaining account of the short-lived experience two freshly minted MBAs had at one of the top Wall St shops back in the 1990s.

Suffice it to say that I thought it was funny before I got into banking – and absolutely hilarious when I read it again after actually spending a few years in the trade.

The authors got out quickly – and relatively unscathed. And yet, only a couple of years in, they had started to feel the gravity of the lifestyle.

Taxis everywhere (a luxury in pre-Uber days). Business-class flights. Pretty much unlimited expense accounts.

In other words, a pair of golden handcuffs that makes it all about the money:

If our counterparts at the other banks ended up making more than us, we figured that we might as well be kissing ass there. After all, at the end of the day it wasn’t like a DLJ ass was any tastier than a Morgan Stanley ass.

All of a sudden, you are down love-thirty. Good luck fighting your way back into the game. Back to kissing that backside.

Moving On Up

The interesting thing about this phenomenon is that it doesn’t really change as you move up the spectrum of incomes. While money loses some of its efficacy after a certain point, increasing one’s social status never gets old.

Consultants want to become partners. Associates want to become managing directors.

And guess what – managing directors want to become Goldman partners, the true aristocracy in the finance world.

The funny thing is that even Goldman partners also have a goal in mind. Do you know what it might be?

Not getting “de-partnered”. What the firm giveth, the firm takes away. But as with anything, losing something you already have hurts twice as much as getting it in the first place.

The process of losing one’s partnership is so painful, that such “de-partnerings” are never publicized. The intent is to free up some room at the top of the pyramid, not to eviscerate people in public and turn them into enemies.

Some folks are ultimately able to game the system in pretty astounding ways.

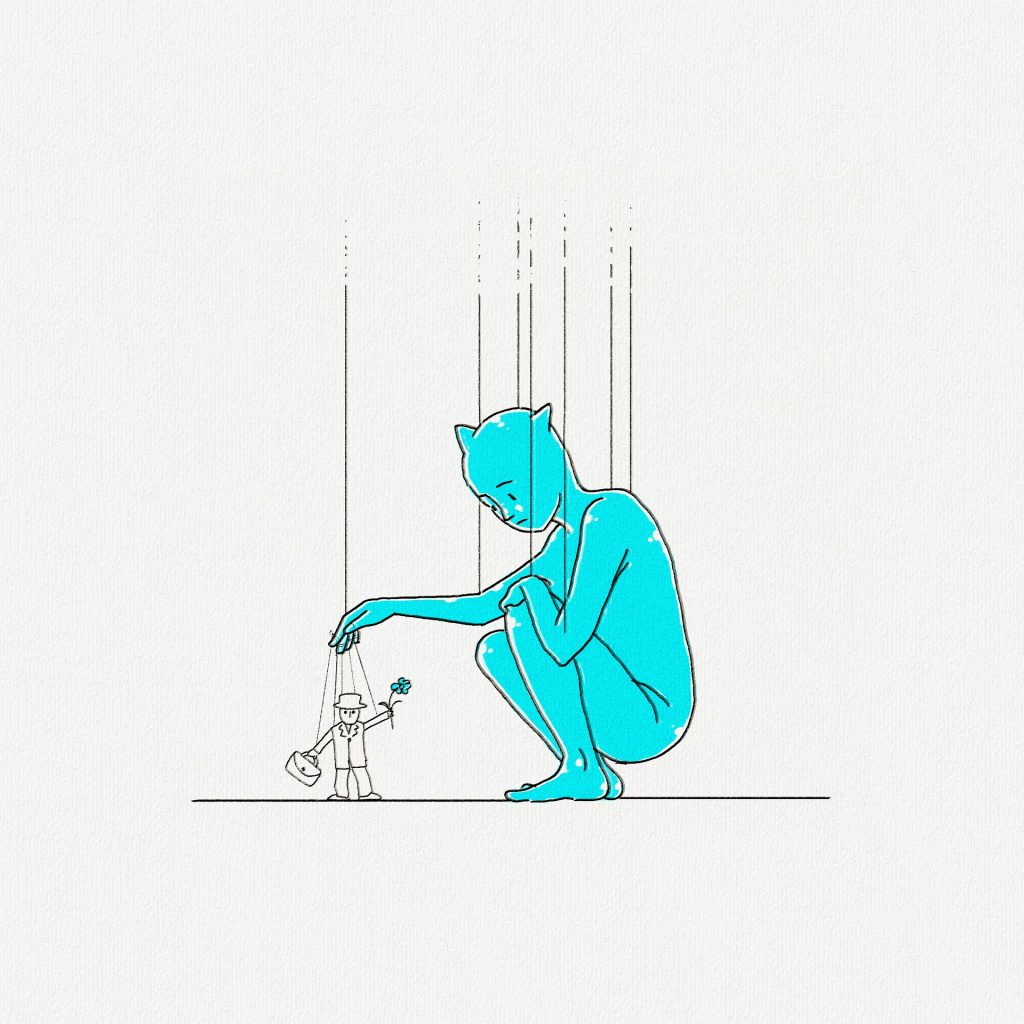

The man who mastered the corporate game

For the vast majority of us, this isn’t the game we will ever win. That is, unless we change the whole premise of the game, which is to allow ourselves the financial and career flexibility that allows us to cut off the puppet strings in the first place.

No, that fancy title isn’t the be-all and end-all.

You’ll be just as happy in economy as you were in first (trust me, I tried it).

Yes, the ability to control your schedule will bring you far more joy than an extra zero on your bonus slip ever could.

The reality is that for most people, the path to wealth lies through paid employment.

So if we are going to spend 60,000+ hours working for “the man”, might as well figure out how to get a proper ROI on that investment of time. And the first step in that direction is to recognize the techniques and pressure points your employer uses to get the upper hand in your relationship.

As for those readers who are talented (and brave) enough to become entrepreneurs themselves? Well, here you have it – the guide to squeezing as much juice as possible out of your employees.

Until they read this article, that is.

Happy working!

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

Extreme bonuses have always seemed to fly in the face of so called “hygiene factors” and the two-factor theory. That is, money is not the prime motivator at work.

I do not wish to cast any further aspersions, but the implications of this apparent paradox have always made me smile!

There’s always another, more expensive thing you can spend money on. And when that runs out (if it ever does), vanity takes over.

Once you get to the partner / C-suite level, the impact of that social capital being taken away might well hurt more than losing the money.

I’ve always detested the method in which the promotion/bonus culture is applied and this was a major reason why I started contracting fairly early on into my career. The subsequent 11 years were wonderful. I got to negotiate my rate and worked my ass off for my clients. I built-up a brilliant roster of contacts who called me back for repeat business. I wasn’t cheap but the clients knew that they would get 110% out of me and I knew that I would be rewarded handsomely. Some prospective clients balked at my rates and that was absolutely fine, we both were able to move on.

And then came the IR35 reform. The uncertainty around it basically decimated my client-base, that coupled with COVID has meant that I’ve had to close my business down. Yes, IR35 reform has been delayed for a year but HMRC’s guidance around it is just as woolly as it is today as it was a year ago. Clients just don’t know how to navigate around the legislation.

And so I now find myself back in permanent employment earning about 60% of what I used to earn (pre-tax). But now I have to play the game, a game that I haven’t had much practice in over the last 11 years. I have friends from uni who are now VPs and Directors and my job title is the same as what it was before I started contracting in 2009. There is nothing that I detest more than those puppet strings.

Two things that I am very grateful for:

1) Finding a job during the pandemic.

2) Having the fortitude to save a sizeable percentage of my earnings when the going was good and paying off my house.

Sorry to hear that. Nothing like some extra government regulations to throw a wrench in the whole setup.

Incidentally, I have quite a few clients who have been impacted by IR35 and their feedback is v. much consistent with yours. Everyone trying to play it safe given unclear goalposts.

On a bright note, you’ve dialed up your earnings in the years when it really mattered (i.e. early on). Congrats on paying off your house – am sure many of your VP / D colleagues aren’t in the same boat. And while a 40% haircut sounds steep, at least it’s coming off a high base.

Hopefully things normalize in a way where you can go back to self-employment at some point!

Pingback: Full English Accompaniment – Embracing change – The FIRE Shrink