Ahh, that good old topic of future market returns.

If I had a penny, or at least a dime, for every time I’ve heard people agonize over future market returns, I’d no longer have to put together M&A deals for a living.

I mean, if only we could steal a glimpse at what’s to come. Just one teeny weenie peak at the FT cover from 2035.

Will the decade-plus bull run rage on? Or are we in for an equity market equivalent of a nuclear winter?

Spend enough time and you could construct a compelling argument for each scenario.

Except that… it doesn’t really matter.

In today’s post, let’s deconstruct the “investment timeline” for someone who is pursuing FIRE – and the impact of a period of low stock market returns along the way.

To do that, we can break down the journey into four distinct stages.

Stage 1: Just Starting Out (10-15 years)

As the name suggests, this is the beginning of your journey.

You are just starting to nail down the basics of budgeting, saving, and investing.

In the beginning, there is no real nest egg to speak of. But by the time you get to the end of this first stage, you will have put together a solid foundation for financial independence.

Stage 2: Approaching FIRE (~10 years)

Things are really running on autopilot now, and your money might even be making more money than you.

At the end of this stage, you have reached the holy grail of financial independence. Time to kiss your cubicle goodbye and say hello to a life of freedom!

Stage 3: Early FIRE (~5 years)

This is the beginning of the rest of our life.

Your financial strategy has gone from accumulation to drawdown, allowing you to step back, decompress, and focus on the things that truly matter.

Stage 4: Retirement (40+ years)

You are now fully used to the financially independent, retired (whatever the word means to you) lifestyle.

Enough said.

The above isn’t intended to be dogmatic – many people will have a different interpretation, or vision, of their journey.

What’s important is that subject to just a few exceptions, there is very little low market returns could do to torpedo your progress.

Let’s have a closer look.

Low Market Returns In Stage 1

Let me be very clear, at some point in your life, you will hit a patch of bad equity market performance.

Well, this is the absolute best time to do it.

Your portfolio is pretty much non-existent, so it’s not like you will be taking a massive hit on day 1.

Instead, it is your contributions that are making the real difference here. More likely than not, your nest egg will be growing in size every year no matter how the market does.

If the market performs well – great! But if it doesn’t, you simply end up buying more shares at a discount.

Think of the people who started investing in 1999 – arguably the worst time in recent history.

Ten years in, the value of their portfolios was still below the value of their contributions:

And yet, those are the very same people who are now retiring in their early 40s. They are the ones who loaded up on cheap equities, realizing a massive benefit when the cycle finally turned.

Impact of Market Returns In Stage 2

If there’s ever a time in your life when you could benefit from a string of above-average returns, then this is it.

You’ve now built up a pretty chunky stash. Your investments are on autopilot.

And because you’ve been smart about your career, you are able to keep increasing your contributions every single year.

So what is the worst that could happen if equity returns come in below expectations?

By now, you are experienced enough to know not to sell in a downturn.

In fact, you probably realize the magnitude of the opportunity ahead of you as you continue investing at a discount.

Yes, a prolonged market drawdown will probably mean it will take you a few years longer to hit your “number”.

You will likely also be more cautious when planning for retirement, having seen the vicissitudes of the market up close.

But the flip side of that coin is that you won’t end up with a misguided sense of safety that comes after a record bull run. And that in itself may be the best attitude to start retirement with.

Hit Me Where It Hurts: Stage 3

Let’s be honest with ourselves here.

Just like Stage 2 is the absolute best time to experience a bull market, Stage 3 is the absolute worst time to run into a bear market.

The good news is that it’s not terminal, not unless you were predicating your retirement on hyper-optimistic assumptions.

Between a cash/bond cushion, a potential reduction in spending, working a part-time job, going back to full-time work for a period of time – or simply delaying your retirement, you’ve got options to combat even the nastiest market correction out there.

No, it won’t be pleasant – or at least it won’t be as pleasant as that mojito-in-hand start to early retirement you may have envisaged.

But do keep in mind that hitting a period of significant market turbulence just as you are about to pull the plug is exceedingly unlikely.

If it happens, you’ll deal with it – and move on with life once things stabilize.

In The Clear: Stage 4

If a period of market turbulence has broken your portfolio, you will know it by now.

More likely than not, the market has done what it always has and delivered a few years of decent, if not mind-blowing returns.

As a result, your portfolio has raced far ahead of where you need it to be to fund a relaxing, enjoyable retirement (once again, so long as you use the right SWR assumptions)

There are many things you should focus on in life.

Your health. Your family and relationships. Finding an enjoyable career that allows you to make a good living.

Financially speaking, you should definitely worry about starting to invest as early as possible and growing the gap between income and expenses.

Market returns will come and go. Some years they’ll be great. In others – not so much.

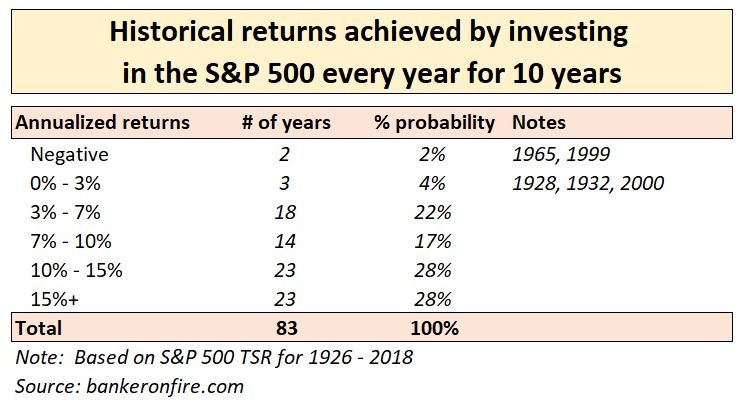

Still, as history shows, the likelihood the market will deliver a prolonged period of subpar (i.e. <3%) returns is exceedingly low:

Plan accordingly – but don’t spend more time agonizing over it than you should.

As always, thank you for reading – and happy investing!

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

Hi thanks for another good post. If I have 300k to invest in equitiesis it worth dca over the long term or should it be invested in one go?. Thanks

I would DCA over 6 – 12 months. Here’s why:

https://bankeronfire.com/lump-sum-investing

Which stage do you think you’re in?

I’ve decided to enter the decumulation phase this year, no matter what.

Definitely stage 2!

Just a simple thank you. Contriarian investing and due diligence always works well. Built an external scaffolding and follow your own path.

Indeed – and thank you!