When it comes to financial self-education, you can hardly do worse than spend one hour a year reading Warren Buffett’s annual letter to Berkshire’s shareholders.

Informative, entertaining and thought-provoking, Buffett’s letters are a far better source of information and advice than 99% of the financial media out there.

And unlike the financial media, Buffett’s advice remains consistent year after year. Instead of focusing on the most recent stock market developments, he takes a truly long-term view.

This year’s letter was published on February 22nd, literally the day before the stock market experienced its first meaningful decline.

That makes it an even more intriguing read – and its lessons even more relevant. Below are my top three picks from this year’s edition.

Predicting The Market

As it turns out, there is a way to predict the market. Just not the way most people think about it.

“Anything can happen to stock prices tomorrow. Occasionally, there will be major drops in the market, perhaps of 50% magnitude or even greater. But the combination of The American Tailwind, about which I wrote last year, and the compounding wonders described by Mr. Smith, will make equities the much better long-term choice for the individual who does not use borrowed money and who can control his or her emotions. Others? Beware!”

There’s more wisdom – and prescience – in the paragraph above than you will find in entire books on building wealth.

It’s worthwhile going back to the 2018 letter and reading up on Buffett’s definition of the “American Tailwind”. It is one of the most powerful arguments for a passive, broadly diversified, low-cost investing strategy (and there’s something there for the gold bugs too!).

It’s also a nice recap of how, despite the almost continuous undertone of doom and gloom in the media (remember – no one ever tells you it’s a good time to invest), the US stock market has been on an absolute tear for the past 100 years, and will continue to do so for the foreseeable future.

But the most important message in the quote above is that it’s not for everyone.

If you simply cannot control your emotions in times of market volatility, you will end up a loser. If you cannot control your emotions – beware.

Find someone who can stop you from hitting the panic button in challenging times – and let them manage your portfolio. Otherwise, you will miss out on one of the most incredible wealth-building vehicles of all time.

The choice is yours.

Profits versus Prices

“Charlie and I urge you to focus on operating earnings – which were little changed in 2019 – and to ignore both quarterly and annual gains or losses from investments”.

Some context is in order here.

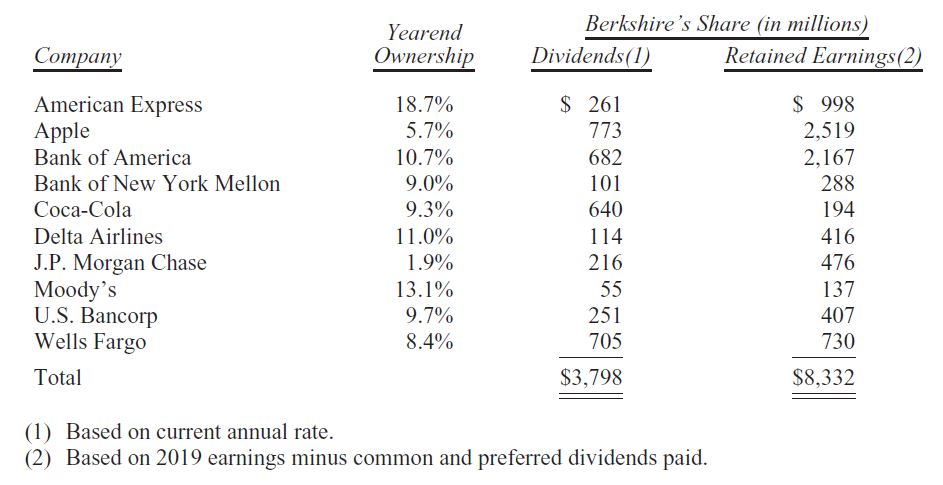

A big chunk of Berkshire’s portfolio consists of minority stakes in large corporates such as Apple, Coca-Cola and JP Morgan. Below is the full list:

The new accounting rules force Berkshire to recognize a profit or loss on those investments – based on their latest market value. If the past two weeks are any indication, they will show a material loss by the time Berkshire publishes its Q1 statements in a few months’ time.

But it doesn’t matter.

What matters is the underlying earnings those companies deliver. If Coca-Cola continues delivering the same profits it has before, it doesn’t matter that its share price is down 10%, 20% or even 50%. That price discrepancy is nothing but a short-term blip.

There’s a nuance here, of course. Chances are, the coronavirus will have an impact on corporate profits. Apple will ship fewer iPhones. Delta will fly fewer flights. JPMorgan will generate lower investment banking profits.

But ask yourself this, does a 20% reduction in this year’s profits warrant an equivalent reduction in these companies’ entire market values?

Sure, the next three, six or twelve months are important.

But unless you think the coronavirus (or whatever else happens to be roiling the markets next time around) results in a permanent impairment of corporate earning ability, you should be viewing the correction as a perfect buying opportunity.

Which segways neatly into the next point.

More Money More Problems

“We constantly seek to buy new businesses that meet three criteria. First, they must earn good returns on the net tangible capital required in their operation. Second, they must be run by able and honest managers. Finally, they must be available at a sensible price.

When we spot such businesses, our preference would be to buy 100% of them. But the opportunities to make major acquisitions possessing our required attributes are rare. Far more often, a fickle stock market serves up opportunities for us to buy large, but non-controlling, positions in publicly-traded companies that meet our standards.”

Some would consider having a cash pile of almost $130 billion (which is what Berkshire is sitting on at the moment) a high-quality problem to have. And perhaps it is.

That is, of course, until you consider inflation.

Assuming a 2% inflation rate, holding a £130bn of cash implies a loss of $1.3 billion per year. For the more mathematically inclined, that works out to ~$3.5 million per day. Ouch.

The moral of the story here is that in some ways, you are much luckier than Warren.

After all, you are able to do something he isn’t – which is to plow all your extra savings in the stock market as soon as they become available. All it takes is logging into your brokerage account and clicking a few buttons.

As for Buffett, I would be shocked if he isn’t licking his lips at the moment, salivating at the opportunity to add a few more crown jewels to his portfolio – at knockdown prices.

So if you happen to be sitting on some cash as well, you would be well-advised to do the same.

And if you enjoyed reading Buffett’s letters, you may want to give the ones by Jamie a glance as well. A bit more specific, perhaps slightly less entertaining – but nonetheless an excellent use of time.

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

My goodness. For one moment I thought Buffett was referring to Terry Smith. But no – Edgar Lawrence Smith. Anyhow, both Smiths champion the idea of putting profit back into the business to make more profit – the real compounding of investing.

Hah. Don’t think Terry Smith is up there on Buffett’s radar. Not yet anyway.

I’m down to about 3 months cash in my emergency fund so won’t be buying anymore other than my usual monthly amount. I’m not that brave and there’s every change we could go into a recession from this (something to my mind that has been kicked down the road from the financial crisis and is overdue ). In a weird way seeing how much my pensions gone down helps me stomach my isa drop . My pension has fallen from 220k to 180k in under a week as my bonus went in right at the peak typically. it’s amazing the size falls when you have a decent amount in there . It’s probably good most people never look at their pensioners! In contrast my ISAs are probably about 15k down . I’ve been really pleased with the way I’ve handled these falls with no worries at all .like you say this isn’t going to impact earnings permanently . I’m betting on this all being a distant memory by August

This has been one of the most eventful weeks at work in recent memory – my phone has been ringing off the hook as people try to make sense of the carnage. Based on what I am seeing and hearing so far, it might not be over as quickly as everyone (myself included) expected just a few days ago.

I definitely wouldn’t dip into your emergency fund anymore – it may well be there’s a severe recession, with weaker companies going bankrupt and causing a domino effect. Keep up your regular contributions and make sure you’ve got enough cash to last you through some tough times. Anything in excess of that can go in the market, but be ready for a rocky ride.

Yep that’s the plan. On the plus side I couldn’t have picked going interest only on my mortgage better lol. 10k emergency fund another 12 k in a 60% bond fund and essential spending of between 1500 a month.