About a year ago, I changed jobs and left my old employer for a competitor. The place I used to work at had a pretty decent pension plan with a generous baseline level and good employer matching program. There are few things I like better than getting free money from the government in the form of a tax break. I signed up for the pension the day I started and by the time I resigned, my pension pot had grown to about £120k.

My old employer used Standard Life as their pension administrator while the new one uses Aviva. Because I had other things to worry about when I started (like not getting fired during my probation period), I had left my old employer’s pension sitting in the Standard Life account – until now.

While doing my financial spring cleaning earlier this year, I decided to take a closer look at my pension investments. I wanted to answer three key questions:

- Is my pension money working as hard as possible?

- What are the fees I am paying?

- How can I create the maximum amount of wealth in my pension pot?

It took me about an hour to answer these questions. By the time I was done, I realized that I could increase my wealth by anywhere between £70k and £280k. All I needed to do was switch my SIPP (self invested pension plan) provider and re-invest my pension into a brutally efficient, high return index fund.

Read on to see how.

Are Your Pension Plan Investments Working Hard Enough?

As I quickly found out, mine weren’t. While Standard Life has a great, user-friendly platform, the choice of investment funds is unfortunately quite limited. For someone like me, who is still relatively young and has a growth mindset, long-term capital appreciation is key.

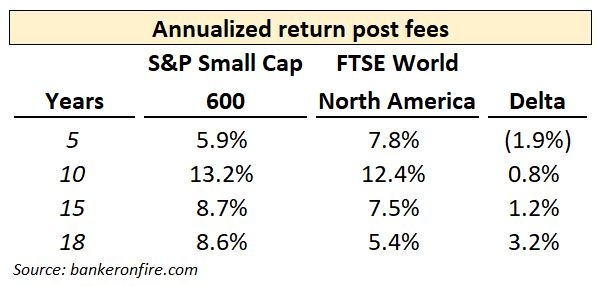

The best investment option I had with Standard Life was investing in the FTSE World North America index. While over the past 5 years it has returned about 8%, it’s long run performance since 2001 is far worse at 5.7%.

Being a massive believer in market efficiency and index investing, I cross referenced the returns above with those from one of my favourite index funds. The S&P Small Cap 600 has returned c.9% since inception in 2001. On a shorter, 10-year time frame the return goes up even higher to a whopping 13.6%.

I discount the performance over the past decade given it happens to encapsulate longest bull market in history. The FTSE World North America has also performed well over the past 10 years. That being said, the long term outperformance of c.3.3% per year is incredibly compelling.

Unfortunately, the S&P fund was not available in the Standard Life wrapper. Luckily, it is available under the iShares ticker (ISP6) in the Hargreaves Lansdown SIPP. This is when I started considering switching my pension provider to HL.

Wait, What About The Fees?

The one thing I hate about just as much as I like getting free money is paying excessive money management fees. I have dealt with a lot of asset managers in my life. Some of the are truly hard working, talented individuals who have your best interests in mind. Unfortunately most aren’t.

I work hard for my money so I’m not about to let someone charge me an excessive fee just so they can buy another Ferrari. What I did really like about Standard Life is that they didn’t (yet) try to screw me on fees since I converted my company pension into a SIPP.

As a matter of fact, I got a discount of 0.7% on the fees charged by the FTSE World North America fund I was invested in. The headline MER on it was a punchy 1.02%, but after the Standard Life rebate it worked out to a respectable 0.32%.

The MER on the ISP6 with Hargreaves Lansdowne is 0.4%. In addition, HL will charge you an annual platform fee of £200. On my current portfolio value of c.£120k, it works out to another 0.2%, bringing the total annual fee to 0.6%.

Given that I hope my portfolio will grow in size and index fund fees continue declining, I can expect the 0.6% to decline over time. For now though, Standard Life beats Hargreaves Lansdown on the fee front.

Performance Net Of Fees Is What Matters

Despite the fee advantage, the FTSE World North America index just can’t match the return generated by a diversified portfolio of US small cap stocks.

Over the past 18 years, the post fee return differential works out to 3.2% annualized. If you shorten the time period to 10 or 15 years, the small cap stocks have returned c.1% more per year.

The only time period over which the small cap index has underperformed is the past 5 years. Over this time, the FTSE World North America index returned 1.9% more after fees.

Ironically, I actually benefited from being invested with Standard Life over the past 5 years. That being said, 5 years is far too short to be statistically significant. My investment horizon is at least 20 years, which means that transferring my pension portfolio to Hargreaves is the right decision.

So How Much More Wealth Will I Build?

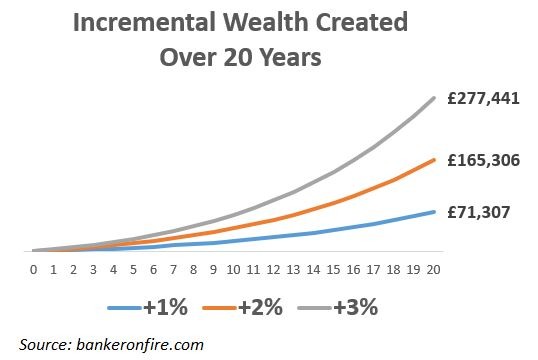

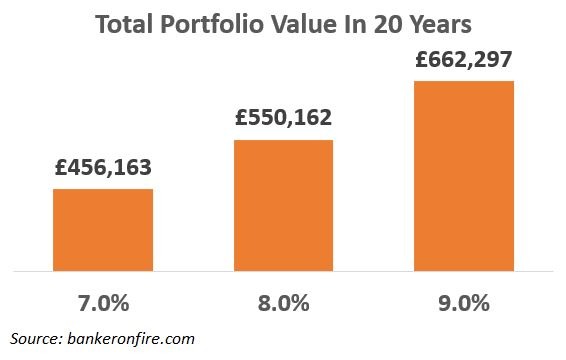

So what is the upshot of all this analysis? For fun, I created an excel template which forecasts my expected portfolio performance with Standard Life and Hargreaves Lansdown.

I made the conservative assumption that a well-diversified index portfolio will generate a total annualized return of 6% over the long run. Based on the table above, I would expect the small cap stocks to outperform it by anywhere from 1% to 3%.

Over a period of 20 years, these incremental returns add up in a massive way. Getting an extra 1% a year increases my expected portfolio value by £71k. If the 3% outperformance holds, my portfolio will be worth an extra £277k in 20 years.

If I showed you the chart above and asked you which portfolio you would like to own in 20 years, I am pretty sure I know what the answer would be. £277k over 20 years works out to about £13k per year or about £1,100 per month. Talk about a decent ROI for an hour of research!

Keeping A Close Eye On Your Pension Matters

Many of us (including myself for the past year) do not pay nearly enough attention to our workplace pensions. As my example proves, it is an oversight that can cost you dearly.

Below is a recap of key things you need to do to stay on top of your company pensions.

- Consolidate all of your workplace pensions. Your current employer is unlikely to let you choose a platform for your company pension. That does not, however, prevent you from putting all of your previous workplace pensions under one roof. Pick a low-cost SIPP platform like HL that offers a wide range of index funds at competitive fees.

- Keep a close eye on your fees. Once you leave your old employer, you may lose valuable rebates on the fees charged by your SIPP platform. This can decimate your wealth over the long run. Be an absolute hawk when it comes to the money others are charging you to manage your pension. Every basis point matters, do not let others take advantage of you.

- Choose investments that maximize performance post fees. Slighly lower fees cannot, and will not, compensate the subpar performance of your investments. Pick an index fund like the S&P Small Cap 600 that is proven to generate solid long term returns and stick to it. It will massively juice your returns over the investment period and your 55-year old self will thank you for it.

Readers, what has your experience been with workplace pensions with your old employers? Are you leaving money on the table or are those investments working as hard as possible for your future?

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

Hello BOF, could you please explain the calculation behind this:

The MER on the ISP6 with Hargreaves Lansdowne is 0.4%. In addition, HL will charge you an annual platform fee of £200. On my current portfolio value of c.£120k, it works out to another 0.2%, bringing the total annual fee to 0.6%.

I looked at HL charges and yeah they cap their platform fee at £200. £200 on £120k is 0.166%, my guess is you rounded it up to 0.2% but I think a deal analyser like you would prefer it be precise which means i’m missing something here. Where is that 0.2% from?

You’re not missing anything – I did round up. Sometimes it’s better to solve for simplicity 🙂