The last four months of the year is a funny time period. One day, you are on a beach somewhere, enjoying that well-deserved holiday. The next, you are plumbing the depths of despair as you come back to the office and question your entire existence.

Hopefully a few days later, you are back in full swing and making grand plans for the remainder of the year. And then a funny thing happens.

You wake up one day looking down the barrel of the Christmas holiday season and it’s time to copy-paste all your ambitious plans into next year’s resolutions.

Let’s face it – the inevitable year-end time warp means that if you haven’t gotten something done by the end of September, your chances of getting it done at all decline exponentially with every single day.

With that in mind, below are five things you need to tick off your list ASAP if you are serious about accelerating your journey to financial independence.

1. Reallocate Your Cash Holdings To Higher-Yielding Accounts

With a highly uncertain economic backdrop (remember that stock market wobble in August?), chances are you have been reluctant to put some (or all) of your savings to work.

Staying out of the market for extended periods of time is generally not a great idea. It does, however, make sense to over-allocate to cash if you are saving for a down payment, approaching retirement, or simply want to ride out the near-term volatility.

Unfortunately, these things always take longer than we expect them to. You need to make sure your cash continues to work for you while you wait. At worst, you want it to maintain its purchasing power in the face of inflation.

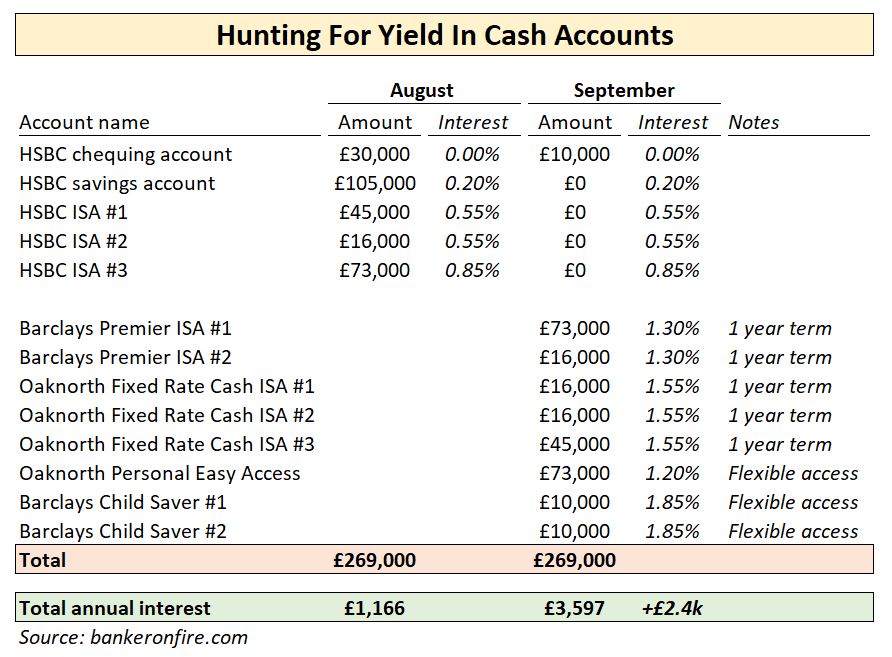

Over the past couple of weeks, I have done some financial housecleaning of my own. I think getting ~1.3% on my money is embarrassingly low, but at least I will clear an extra £2.4k of interest income over the next 12 months. Not bad for a few hours’ work – and feels really good to finally get rid of the loyalty penalty by HSBC.

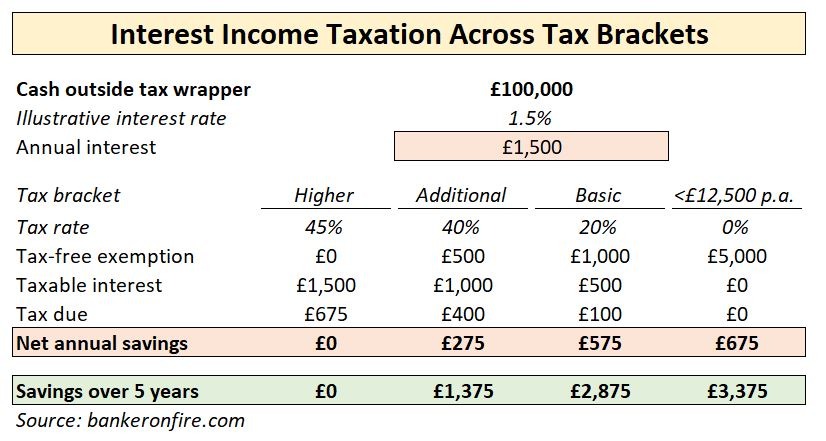

2. Consider Taking Advantage Of Your Spouse’s Lower Tax Bracket

As the title suggests, you will need a spouse in a lower income tax bracket for this one. If that’s the case AND you happen to have considerable cash sitting outside a tax-efficient wrapper, you may want to consider whose account that cash sits in.

For what is essentially a fast and simple hack, the savings can be meaningful.

3. Reinvest Those Dividends

If you have stock market investments without an active DRIP (Dividend Re-Investment Plan), you need to make sure the dividends are continuously reinvested back into the underlying securities.

Since trading fees are pretty much converging to £10/transaction these days, the optimal frequency to reinvest your dividends primarily depends on three factors:

- your portfolio size,

- the annual contribution

- dividend yield

I ran some pretty comprehensive analysis on this earlier in the year. To maximize returns on a £100k portfolio with a £10k annual contribution and a 2% dividend yield, you should reinvest your dividends either biannually or quarterly.

Feel free to play around with my dividend reinvestment spreadsheet to test the criteria for your portfolio – and reinvest accordingly!

4. Consolidate Your Pension Pots

Workplace pensions, as great as they can be, have one major drawback. Because you are forced to use your employer’s preferred pension provider, your pension investments probably aren’t working for you as hard as they can.

This happens because you are “guided” (i.e. forced) to invest into a suboptimal set of funds and/or take on excessive fees.

This is why, if you haven’t yet consolidated your workplace pensions from any previous jobs, you should do so now.

When I left my last job a few years ago, I was taking a performance hit of anywhere between 1 – 3% p.a. (net of fees). As a result, on a twenty year basis, I was about to forgo up to £280k of returns!

When it comes to large pots invested over long tenors, every basis point matters. Consolidate your pensions to make sure they work as hard as you do.

Note: Sometimes you can actually get a cash bonus for transferring your SIPP to a new provider. Hargreaves Lansdown is running one with a £50 – £500 bonus now (it technically expires today but they do it regularly). Either way, you may want to check with the SIPP provider you are considering to see if they will sweeten the deal for you.

5. Make Even More Money

It’s good to squeeze every last ounce of juice from your savings and investments. This is is what the four tips above are intended to do.

It’s even more important to make sure you continue feeding the piggy bank by continuing to maximize your income.

As it happens, September is the time of the year when many of us hit the runway for our annual performance review – and our annual bonus.

Therefore, if you haven’t yet started implementing a strategy to maximize your bonus, you need to do so pronto.

And if you think that you will get a good review and bonus by simply doing a good job and writing a good summary at year-end, you are wrong. Read this if you want to know why.

Here are three things you should do instead.

Understand the performance review process and create your stakeholder map

This is just basic career management 101. You need to know how your performance review process works, what criteria is being measured and when the performance ranking sessions take place.

Most importantly, you need to understand who the key decision makers are. These are the people who are typically in the room when performance grades are being assigned. They are also the ones with sufficient seniority and political capital to be able to influence the conversation and move employees between buckets.

Remember – simply relying on your boss to make your case is not the right strategy. Even if she is the most powerful person in the room and loves you to pieces, you need to make her job easier by cultivating a broad base of support.

Have a strategy for engaging your stakeholders on an ongoing basis

Once you’ve identified the key decision-makers, you need to come up with a strategy to make yourself visible to them – and make a good impression along the way. There are many ways of doing this.

For example, you could ask to join a cross-departmental project team or take on a role with a recruitment or charity committee (which are fun and rewarding to do in the first place).

Because you will naturally have fewer interactions with the stakeholders outside your department, you need to make sure you shine in every single one of them. Make these projects your top priority, add as much value as you can – and make it known.

Lobby for a good review ahead of performance evaluations

This is the simplest step – but also the most overlooked one. A week or two ahead of the annual performance review session, you should have a “soft” touchpoint with each of your stakeholders.

It doesn’t have to be complicated – just ask to go for a coffee with them. Then you can remind them of everything you’ve done over the past twelve months and the contributions you are looking to make going forward.

Mention that you know that the annual review is coming up and you are very hopeful that your hard work and efforts will be recognized so that you are in a position to make an even greater impact next year.

That’s it really. Most people will get the point. The ones who don’t (or choose not to), won’t have been pushing your case anyway. But just following the three simple steps above will leave you miles ahead of 95% of your colleagues when it comes to your pay and promotions.

So here you have it. It’s not a perfect and by no means a comprehensive list. Still, get these five items ticked off and by December, you will be way ahead of where you had started, with tons of momentum for the year ahead!

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

This is a great blog.

Wouldn’t gold give you a better return than the cash accounts?

Thanks John, glad you like it!

Gold could well give you a better short term return but it would be purely speculative. You don’t know where the price of gold will be in one year’s time, which is unhelpful if you are saving up for a down payment or prepping for retirement.

From an investment perspective, I subscribe to Warren Buffet’s logic of why stocks beat gold as an investment. These two links have a good explanation:

https://markets.businessinsider.com/commodities/news/warren-buffett-bashes-gold-2019-2-1027977003

https://www.businessinsider.com/warren-buffetts-lesson-on-gold-2013-3?r=US&IR=T