Updating your net worth spreadsheet can be an exciting affair.

Nothing quite like getting a dopamine rush as you watch the numbers tick up, bringing financial independence firmly into focus.

Another dollar, another step closer to leaving the cubicle behind.

There is no doubt the absolute number is an important starting point. So is analyzing the way it has changed compared to the last time you ran the numbers.

Is it up? (yay! )

Down? (dang!)

How much? (who-hoo!)

However, if you want to get the most out of your next net worth update, focusing on the bottom line is just one part of the exercise.

There are other, equally important observations you should be making that can help you optimize your investing journey.

To that end, here are five questions I ask myself every time I calculate our family’s net worth.

Question 1: How Much Money Have I Contributed To My Portfolio?

Imagine you have a $100k equity portfolio and are contributing an additional $10k/year.

In a year when the stock market is up 30%, you’ll end up with $140k ($100k + $30k investment gain + $10k contribution).

Alternatively, if the stock market is down 30%, your net worth will land at $80k ($100k – $30k investment loss + $10k contribution).

The point here is that once your portfolio reaches a certain size, the way your investments perform will have a much bigger bearing on your net worth than your contributions.

And yet, it is your contributions that ultimately determine how much money you will end up with at the end of your investment journey.

In a perverse way, the change in your net worth number becomes a less relevant benchmark the further you are on the journey.

It’s easy to get complacent in the first scenario above. When asset prices are going up, people feel wealthier and inevitably end up spending more, with less money directed towards their nest egg.

And it’s equally easy to get frustrated when the stock market is going down and you are watching your “stash” decline despite all your hard work and dedication. What’s the point of saving all that money?

The bottom line is that once you’ve decided on your asset allocation, you have zero control over the performance of your investments. It’s highly unpredictable in the short term – and the market will do the heavy lifting for you in the long term.

However, the one thing you can control is maintaining (or ideally, growing) the contributions you make each year. Make this your focus area instead.

Question 2: Do I Have Enough Cash?

In his recently published (and excellent) book, The Psychology of Money, Morgan Housel writes:

“Say cash earns 1% and stocks earn 10% a year. That 9% gap will gnaw at you every day.”

“But if that cash prevents you from having to sell your stocks during a bear market, the actual return you earned on that cash is not 1% a year – it could be many multiples of that, because preventing one desperate, ill-timed stock sale can do more for your lifetime returns than picking dozens of big-time winners.”

This is probably the most eloquent articulation of why you need to have a sufficient cash balance on hand.

It may feel like you are leaving money on the table, but the last thing you want is to be forced into a fire sale.

The amount of cash you need primarily depends on two factors:

- Your monthly expenses – and the ability to reduce them in an emergency, and

- Your job security.

Those who own investment properties have a third factor to contend with – being able to sustain a period of non-payment by tenants.

Personally, I keep a cash buffer equal to 12 months of expenses and 6 months of rental income. It may well be a bit too much. I sure hope I never get to use it.

But with two young children and an unpredictable job, I’m happy to forgo some investment gains in return for peace of mind – and the ability to avoid large losses in a downturn.

Question 3: What Is My Debt To Equity Ratio?

Getting rid of debt is the core tenet of the FIRE philosophy. It makes a lot of sense – when it comes to high-interest, consumer debt.

For a variety of reasons, borrowing on the margin to invest in the stock market is also not a great idea.

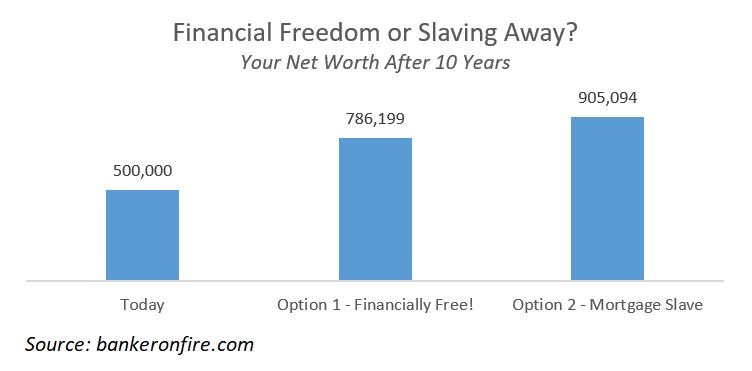

Mortgage debt, however, is a different beast entirely. In today’s low-interest-rate environment and subject to a reasonable LTV ratio, it can be a fantastic wealth-building ally.

Below is an example of how much of a difference remaining a “mortgage slave” can make to your finances:

At present, our household debt-to-equity ratio (i.e. our total debt divided by our net worth) stands at about 40%.

The more mortgage-financed properties you own, the higher this number is likely to be. I certainly expect ours to go up if my plans to acquire more real estate work out.

There’s a fine line here. After all, one can make the argument that slowing down mortgage repayments in favour of stock market investing is the same as borrowing to invest.

To me, that’s semantics. Unlike margin loans, mortgage debt isn’t callable. And no one forces you to put money in the stock market. Many people choose to buy additional properties instead.

The key is to find a level that’s comfortable for you – and make sure you’ve got enough cash on hand to fund any emergencies.

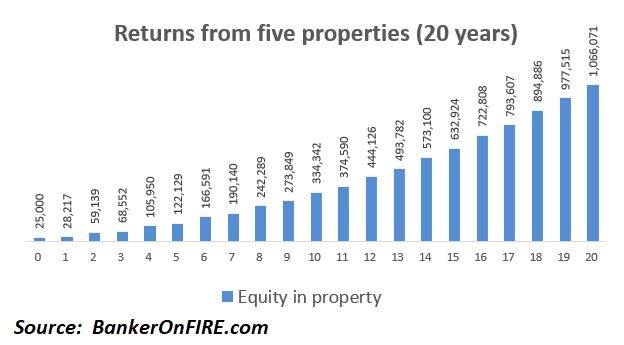

Question 4: What Is My Allocation Between Equities and Real Estate?

Some people love the stock market. Some prefer real estate.

I happen to like both. That being said, I certainly wouldn’t want to be too heavily skewed towards one asset class over another.

At present, our property investments (net of mortgages) represent only 25% of our net worth, significantly below stocks. Therefore, I am focused on adding at least one (and ideally two) more investment properties over the next 12-18 months.

Despite what many people would like you to believe, real estate investing isn’t as easy as it seems. But, provided you acknowledge the challenges, it can also make you rich.

If you happen to like real estate as an asset class, you’d be well advised to come up with an allocation that works for you – and make sure the pendulum doesn’t swing too far in either direction.

Question 5: Are My Investments Properly Allocated Between Deferred and Accessible Investment Vehicles?

The earlier on you are in your journey, the more attention you should pay to investment vehicles like your workplace pension and your Lifetime ISA.

Allocating your investments to these two buckets can give your net worth a very nice boost in the form of government tax breaks and employer matches.

The catch, however, is that you cannot access any of the money until you are well into your late 50s – and that goalpost may well be moving further away.

It makes perfect sense to think of your golden years first. That was certainly our logic when my wife and I started maxing out our workplace pensions in our early 30s.

However, once you’ve built up a certain balance in your pension and LISA accounts, you may want to let time and compounding do the rest of the work – while you refocus on your ISAs.

Overshooting the target in your pension pot is a high-quality problem (as long as you don’t exceed the LTA). There are many ways to “bridge the gap” of a couple of years.

That being said, you don’t want to be in a situation where you are ready to pull the plug at 45 – but cannot afford to do so because all of your money is tied up in deferred investment vehicles.

Next time you run the spreadsheet, take all the time in the world to pat yourself on the back for the progress you’ve made.

Then, take the time to ponder the questions above. Thinking through them may well make your journey shorter – and more enjoyable.

Happy investing!

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

Really good advice bof particularly the pension vs isa debate. And especially for high earners. It’s not all about tax there’s a wonderful feeling of contentment to knowing you could live without a job for several years by having a good slug in Isas despite the tax hit

Yes. At the moment, 95% of our equities holdings are within our pension plans. Cash, on the other hand, primarily sits in ISAs.

We use the cash to acquire property (and an emergency fund) but going forward, the focus will shift to scaling up the proportion of equities in ISA vehicles.

Agreed – possibly a topic for future article. When to switch the focus from Pension to ISA and bridging the gap rather than looking at total net worth.

I’m approaching that tipping point myself and I’m finding it difficult to swallow the tax hit even though I know if I continue for many more years as I am I’ll likely break any LTA’s which exist in 25 years when I come to draw from the pension pot.

The recently finished Monevator series on Bridging the Gap is worth a read if you’ve not seen it already. I’d also be interested in BoF’s take on it, however.

I’ll likely hit the LTA projecting it out 25 years (subject to heavy change) when I can retire, but I’ll be upping my allocation to bonds when hit my 40s, which will go into my pension to lower the likelihood of a breach.

Separately, I used to fill in my spreadsheet on a monthly basis but I’ve decided to only do it once a year now when I run through my Finance checklist (checking credit reports, closing accounts no longer needed, using capital allowances etc etc). I don’t think it’s that value adding keeping your face in the spreadsheet.

Thanks Genghis, yes I’ve read the Monevator post, interesting and I appreciate their content but always good to read several perspectives.

Interesting concept of holding different asset classes within different vehicles. I can see the logic of holding bonds in ones pension to reduce the risk of exceeding the LTA. Presumably this would mean higher exposure to equities in ones ISA though, and unless you’re holding a large cash position, would this not increase your sequence of returns risk? Best to draw from bonds in the event of a bear market which you can’t do if locked in a pension.

Interesting point on the sequence of returns Rosario.

I would argue it also makes rebalancing more complicated as you typically want to sell off some bonds and load up on equities in a downturn, but – hello LTA once the market recovers.

Genghis – I also use my net worth update as a way to check in on all of my accounts (many of which I don’t touch / check otherwise). So the added advantage of the net worth update is guarding against fraud and just general housekeeping.

I might do a post on bridging the gap. Challenge is that as a general principle, I don’t like to double-up on well-covered topics and Monevator has done a great job on this one.

Thanks for the guidance on allocation to bonds as you approach the LTA Genghis. I’m very likely to be in breach of LTA so could always switch it at some point so pension becomes a more bond-heavy investment whilst ISAs are primarily equities. That way I could still balance across my investments but slow the pension growth.

Thanks for that as not an option that occurred to me!

For some high earners it’s not a choice as if you are tapered down to 4k then it’s really only ISA

I’m in that boat myself, but I often remind myself that I probably won’t always be in the taper zip code.

Career moves / sabbaticals / periods of unemployment can open up additional pension contribution room.

I’ve decided to do both equally if it helps I can get contribute 40k into my pension as not a super high earner. So I put 2k a month including employer’s contributions and a further 2k in Isas. With another 400 in saye and sip schemes. I have over twice in my pension what I have in Isas so this feels about right

It leaves things a bit tight sometimes but especially atm there’s naf all to spend it on anyway

Means I have 220k in a pension and about 130k in Isas and company schemes (100k in s and s Isas). For me this feels about right. I should be near the lta but keep enough outside pensions for life events and to make a dent in the mortgage with the yield. Keeping capital intact ( 270k currently) .

Great points on Question 1, I never thought about it in that way, but contributions definitely determine future returns, even if they sometimes get ‘swallowed up’ in a market downturn. I keep track of both my net worth and also my contribution each month.

Your cash holdings sound sensible, I currently have 6 months but would like to eventually get that up to 12. Might seem excessive for a single person with no dependents, but I think it’d feel relaxing to know I can go a year without working at all.

I think it depends on your overall investment level. I used to carry about 12 month’s when it was lower but now down to about 5 or 6. My jobs stable and I have several years in investments so even if I had to pull a bit out during a downturn it wouldn’t be the end of the world. That’s my viewpoint anyway

At the end of the day, it’s about finding a sweet spot that works for you.

With a volatile job, two kids, and a wife on maternity leave, 12 months is what helps me sleep at night.

And if you have an investment pot you are happy to fall back on despite the downturn, that can obviously figure into the equation.

Great points from both of you. Same here fatbritabroad, at this point I have a few years’ worth in investments, but they are all in pensions or ISAs and ideally, I don’t want to draw money out of my ISA as I can never get that allowance back.

That said, I’ve just gone through a pandemic as a self-employed person, losing 50% of my income for several months, and I didn’t have to dip into my emergency fund, so it’s unlikely that I’ll ever need more than 6 months. I think it’s all just about peace of mind for me, not an actual, ‘real’ risk. I’m more of a planner than most.

Slightly off topic – but FYI.

Further to our chat about spending trajectories back in August, the following [US based] paper has just been published:

https://cdn.ymaws.com/dciia.org/resource/resmgr/resource_library/DCIIA-RRC_RightSizing_091020.pdf

The paper is co-authored by one of the better known SME’s and covers a lot of familiar ground. However, the paper has some new research into whether reduced spending during retirement is as a response to constrained means or otherwise. The authors use “fundedness” as a key metric and I found the results very interesting.

Hope you also find the paper interesting?

Very interesting indeed, thanks for sharing. I’ve got to admit, I never gave much thought to the impact of financial constraint on spending patterns in retirement.

I can see how for people who are “forced” to retire (health issues or even something as unfortunate as age discrimination) impacts their thinking about money.

Yet another reason to save more rather than less. No guarantees it won’t happen to us.

Yup, as I read somewhere recently:

“The more general takeaway for white-collar workers is save, slow and steadily, as if you were going to retire early, because one day you may have to.”

Pingback: A retirement simulator you have to see - Apex Money

Pingback: Saturday Linkage – 39 Months