In the personal finance community, you will struggle to find a set of people more vehemently disliked than active money managers. Yours truly certainly shares the sentiment.

There are exceptions, of course. Star managers who haven’t (yet) fallen from grace. The rare species who manage to deliver truly superior risk-adjusted returns for their investors.

Ultimately, their success does little to appease us. Which is just as surprising, considering that that active investing is the cornerstone that makes our financial independence dreams possible in the first place.

Imagine…

… a world in which all active investors disappear overnight.

When the stock markets open the following day, you will struggle to tell the difference, other than perhaps a reduction in trading volumes.

Passively run index trackers will step in, buying stocks at current market prices, and according to pre-determined investment criteria. Life will chug on as before… or will it?

Let’s assume for the moment that this is the day when Microsoft chooses to report its quarterly results.

As ever, some areas of the business will do better than expected, some others perhaps worse.

Unfortunately, there won’t be anyone out there to hear Satya and Amy deliver their speech.

Institutional research analysts will have stayed home, licking their wounds and looking for a new job.

And millions of individual (i.e. “retail”) active investors worldwide won’t even bother to open the investor presentation, occupying themselves with more exciting endeavours.

As a result, the Microsoft share price will likely stay where it was before the results call.

Wait, say you. Wouldn’t it move as a result of broader economic changes, such as a nasty spike in jobless claims?

The answer is no. With everyone gone fishing, there won’t be anyone out there to pay attention to any of the macro data either.

The new president (finally) chooses to close down some corporate tax loopholes? No impact on the share price whatsoever.

A possible reduction in the value of the US dollar, making the company’s overseas earnings much more valuable? It won’t matter.

And neither will a myriad of other factors that impact the amount of earnings and cash flows attributable to the company’s shareholders.

Almost immediately, the Microsoft share price will become disconnected from both macroeconomic and company-specific fundamentals.

The same will happen to the prices of all the other risk assets out there.

Well managed companies won’t get the credit they deserve. Poorly run ones will renew their lease on life.

Pretty quickly, high-quality managers will realize they no longer have the incentive to work as hard. And without a declining share price to keep them to account, the less qualified ones will stick around for much longer.

It will be like the stock market version of communism, inevitably leading to a deterioration in economic growth and output… incidentally something communism is well known for.

The impact will be felt far beyond the stock market. Sure, some risk assets (like currencies and commodities) will continue to react to the shifts in supply and demand.

However, no one will be taking forward-looking bets on specific currencies on the back of policy changes. And the impact of secular trends (electric cars, anyone?) won’t be reflected in the price of commodities until demand falls off the cliff – or supply rockets through the roof.

In the meantime, us passive index investors will be none the wiser. We will continue to “VTSAX and chill” – and ultimately end up acquiring a bunch of mispriced assets.

Bucking The Trend

Now, let’s imagine for a moment that while everyone is otherwise occupied, a brave active money manager reappears on the scene.

Quickly spotting the opportunity, she loads up on the well-managed companies while shorting the hell out of the underperforming ones.

As the former grow their earnings and dividends and the latter eventually go bust, this money manager will clearly make a fortune.

Along the way, her buying and selling activity will result in (some) asset repricing, ultimately helping us passive investors get a “better shake” on Wall St.

Most importantly, this process will play out at zero cost to us. It will be the fund manager’s investors who will foot the bill through their investment fees.

They will, however, receive a handsome reward in the form of superior returns on their money, making the whole endeavour worth its salt.

A Problem Of Scale

The fundamental challenge of the active asset management industry today can be neatly summarized in just four words: it’s too damn big.

Hundreds of thousands of intelligent, hardworking people are ultimately trying to price the same universe of risk assets.

It’s hardly surprising that those assets tend to be (for the most part) accurately valued by the stock market.

I am not a believer in the efficient markets hypothesis – not in the strong form anyway. But it is fair to say that when mispricing does occur, the forces of the market correct it pretty quickly based on public information.

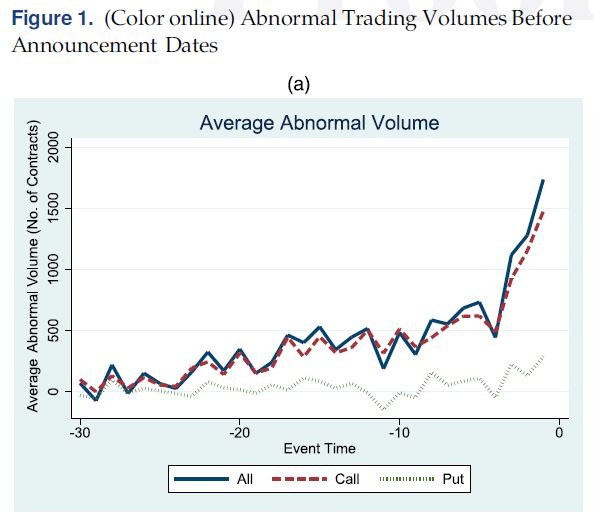

Sometimes, as the chart below illustrates, even the non-public information gets reflected in asset prices, thanks to those naughty inside traders.

But back to the topic at hand.

But back to the topic at hand.

As a consequence of having so many people prowling the markets looking to exploit price inefficiencies, generating excess returns is akin to squeezing water from a stone.

When it does happen, the associated costs tend to make the whole affair unprofitable.

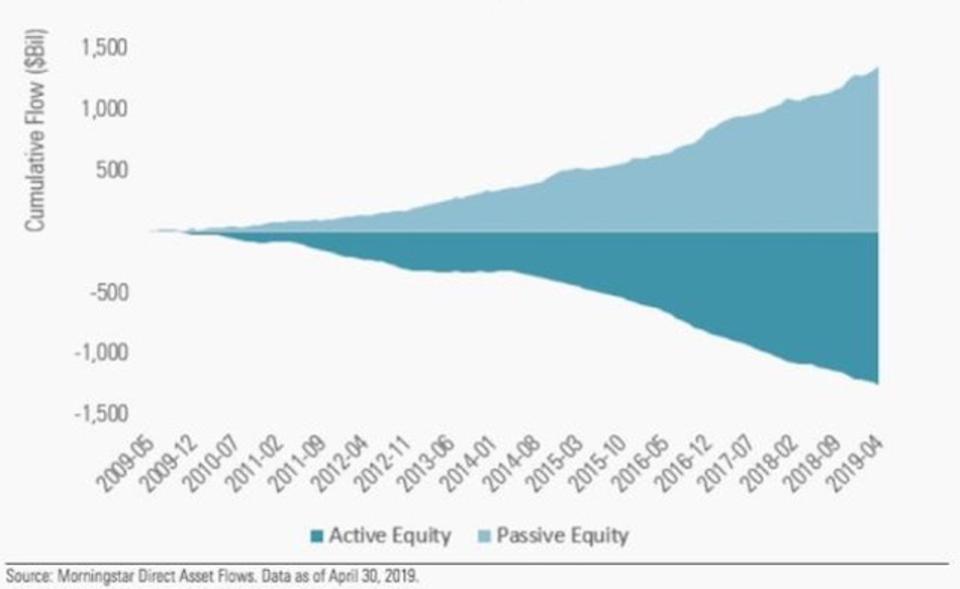

Investors are voting with their feet, leading to an ever-accelerating outflow of funds from actively managed vehicles.

The active management industry is shrinking. It may not be happening overnight, but the trend is clear. As the industry shakes out, two things should happen.

The first one is that only the most qualified and successful active managers survive.

The second is that they should find it easier to generate excess returns, which should ultimately make their business model economical again.

Let this process play out long enough – and we may well end up in a situation where active investing becomes a worthwhile endeavour.

A Word On Quants

In the recent past, a new investor class has been disrupting the active asset management industry, universally known as the quants.

Unlike their peers, they don’t bother with fundamental analysis. Instead, they scan billions of data points a second to identify and exploit stock market inefficiencies – and make a killing in the process.

The most famous of them all

One could argue that with the ongoing demise of the traditional active managers, the quants will capture an ever-increasing portion of the economic value in the investment management industry.

I disagree.

While data mining has loads of potential, it is unlikely to completely replace fundamental analysis.

As it happens, many of the data points analysed by the quants are actually generated by active managers. It may well be a more symbiotic relationship than anyone wants to acknowledge.

Ultimately, fundamental analysis will always find its place under the sun. Identifying trends, predicting human behaviour, betting on strong management teams, anticipating political developments – the list is endless.

One day, the machines might well be able to take over. But that day hasn’t come yet – and won’t for a while, still.

Active money managers certainly aren’t the flavour of the day. But make no mistake – us passive investors are getting a free ride on the coattails of their hard work, as well as the fees their investors pay.

There’s no need to join them, not yet anyway. The industry is still far too large and returns too sparse.

Equally, we should wish them all the success in the world. Our financial independence plans are riding on it.

Happy (passive) investing!

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

Hi BoF,

I have a question regarding your statement: “Quickly spotting the opportunity, she loads up on the well-managed companies while shorting the hell out of the underperforming ones.”

This is the case as long as there is significant capital in the actively invested funds, right?

Imagine the trend continues and more and more money is flowing into passive funds (which is definitely expected). At that point, those funds will keep buying Apple (and the other 499) which will just make it even bigger thanks to its already large weight in the index.

Imagine as well for a second that Apple cannot keep up with innovation, they start losing market share, people don’t buy their phones anymore, maybe they even become loss making. The share price needs to reflects this information. Passive investors, however, just keep buying it.

Your argument, that active investors, will correct the market, would mean that they would other overlooked stocks (such as small caps) and short “the hell out of” the underperforming Apple stock.

But capital held by active funds is now much, much smaller than those held by passive funds. So even though they start shorting it, the upside force is stronger.

Am I seeing this right? Do you see this happening in the future?

I am a HUGE proponent of passive investing, however, as you pointed it out it completely disrupts the efficient capital allocation process.

If capital keeps flowing into passive funds, there won’t be enough “active money” to have enough influence.

I think it’s a sensible analogy but I doubt we will ever get that far.

The good news is that active managers aren’t giving up the fight that easy.

The more money flows into passive, the easier it becomes for the remaining active managers to generate alpha, and attract more money. So we will always have this push-pull effect, keeping the system in balance.