In what is becoming a recurring theme, a long-time reader (let’s call him Bob) sent me a link to an article about passive investing the other day – and asked for my views.

The article itself was unremarkable, a thinly veiled shill for an active investing product. Hence, I won’t honour it with a link, as I did for the Sunday Times article last week.

The point is, once you’ve seen a few of these articles, you quickly realize they all follow the same recipe.

Start with some stats on passive investing. In particular, talk about massive inflows into passive products. Reference the “bull market in passives” and “valuation disparities”.

Sprinkle in a few out-of-context quotes by Warren Buffett and follow that up with stern warnings for passive investors. “The end is near!”.

Then, once the audience is primed, it’s time to go in for the kill start pitching your “hand-selected” active funds.

The ones “structured to thrive in a passively-dominated market environment”.

With investment strategies employing “highly convex positions”, “asymmetric payoff opportunities”, and “taking advantage of implied volatility”, whatever that means.

By the time you get to this point, if you know what’s good for you, you want to click on the “x” in your browser window and stop wasting your time (and possibly money).

Except that I didn’t.

The Sum Of All Fears

The reason I didn’t is that I could tell that Bob, while rightfully skeptical, was also concerned.

Concerned that there indeed may be a “bubble in passives”.

That the popularity of passive investing products may have “overinflated” the value of the index funds he was buying.

That, ultimately, his hard-earned money could be at risk as a result of some unseen, unexpected danger lurking around the corner.

But is that really the case?

Passive Investing – A Relentless Rise

Let’s start with the basics.

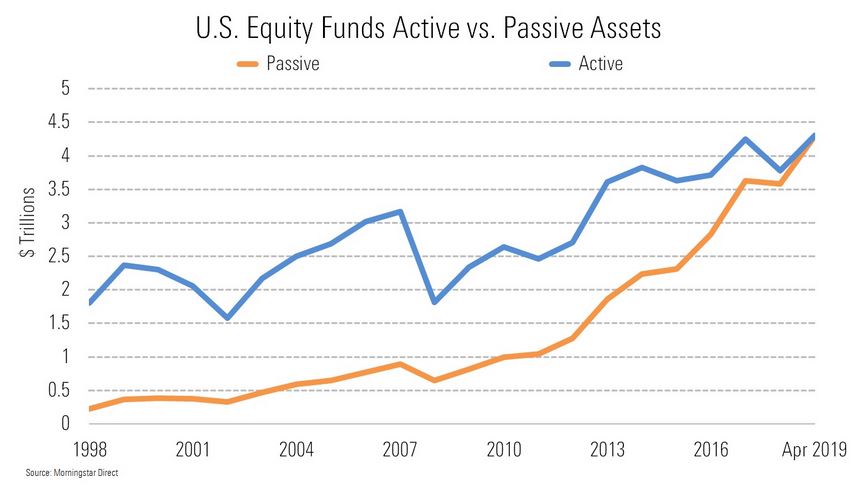

To be fair, the words “a bull market in passives” do have some truth in them. Their performance (bolding intentional) over the past 20 years has been nothing short of astounding.

According to Morningstar, as recently as 1998, active funds had more than six times assets under management than their passive brethren.

Two decades later, the two pools of capital are roughly equal in size.

So far, so factual.

And this is exactly why you should ignore factoids like:

“Over 100% of gross equity inflows are into passive vehicles”

Of course they are. It’s no secret that money has been flowing out of underperforming active funds and into index trackers.

“Most settled trades are between passive index participants”

What else did you expect? By default, index funds hold the underlying index. The composition of the underlying index changes constantly. Hence, index funds trade often in order to mirror the underlying index.

Back To “Performance”

It’s important to go back to the topic of “performance” of the passive products.

Any time you hear stats like the ones above, you need to note that this performance is all about assets under management.

In other words, it has ABSOLUTELY NOTHING to do with the actual price performance of the index products themselves.

Because, as we all know, the price performance of a well-managed index product mirrors the price performance of the underlying benchmark, less a minimal fee.

If you held the S&P 500 index tracker, you’ve done very well – just like the S&P 500 did.

If, on the other hand, you were invested in the FTSE or some form of a value index, not so much.

At any given point in time, the equity index fund you are holding is giving you proportionate ownership in all the stocks comprising the underlying benchmark.

Thus, the only way your index fund could be “overvalued” is if the actual underlying index is overvalued. Which, incidentally, brings us to the next point I would like to address.

Pinning The Blame

Sometimes, critics of index investing go beyond basic misinterpretation and start making truly egregious claims.

In the article sent to me, the author had the nerve to make the following statements:

“Passive investing is why the US stock market trades so highly”

“Passive investing is why small-cap stocks have had a historic period of underperformance”

And my personal favourite:

“The reason active funds have underperformed is because of price-insensitive passive funds” (!!!)

First of all, passive products are not limited to the US stock market or a specific sector.

There are literally gazillions of passive products out there covering every single asset class, industry, product, commodity, fixed-income instrument, geography, style, size, and a myriad of other factors.

So the argument that passive products somehow “overlook” sectors like the small-cap (incidentally, I own small-cap stocks – via an index fund), is pure lies.

But it is really the last argument, which looks to blame index funds for active fund underperformance on passive investing, that takes the prize.

In reality, index funds are an active manager’s best friend.

As more and more money flows into passive indices, there are fewer and fewer active money managers analyzing equities and other assets.

As I have written about previously, making money in a world with no active managers would be easier than shooting fish in a barrel.

Instead, the problem of the active investing industry is that it is still too big for its own good.

Put simply, there are too many people chasing the same limited universe of price inefficiencies. This is why, in aggregate, they underperform the market.

Layer in fees and competition from other folks who can actually beat the market and you see why active management, as of today, is a losing proposition.

The Truth About Passive Investing

Having said all of the above, there is one argument in the active-passive debate that I do buy:

Passive investing can contribute to market volatility.

When the price of an asset goes up, its relative weight in the index also goes up – at the expense of other index constituents.

Given index funds look to replicate the weightings of the benchmark index, they would buy more of the appreciating asset and sell a little of all other assets.

In markets with thin liquidity and many passive players, this can create a “melt-down” effect, where a decline in price becomes a self-fulfilling prophecy.

It can also go the other way and result in a “melt-up”, which is partially what happened back in August. Softbank made a massive bet on tech stocks, sparking a broad-based price rally until it corrected in September.

Is market volatility a problem? Clearly, not least because it can spill over into the real economy by inducing panic and impacting spending and investment decisions.

It is also a problem for those folks who get excited after a market run-up and buy at the top. Those same people typically get depressed after a market decline and sell at the bottom.

In other words, rinse and repeat until you are broke.

But for long–term investors, which is something we should all aspire to be, it’s much less of a problem than the financial press would like to make it out.

After all, if you buy on a weekly / monthly basis over a period of thirty-odd years – and follow that by gradually selling over the next few decades, the volatility will average out. Nothing to see here, moving on.

Sadly, alongside many hard-working, honest folks, the money management industry also tends to attract quite a few less than salubrious characters.

Sometimes, they will put forth arguments that sound compelling but don’t hold up to analysis. In other situations, they will simply lie. And often, it’s a combination of the two.

If you know what’s good for you (and your portfolio), you will ignore them and move on.

Happy (index) investing!

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

Interesting generally, thanks BoF.

One point stood out:

“ Put simply, there are too many people chasing the same limited universe of price inefficiencies. This is why, in aggregate, they underperform the market.”

Do you have any evidence for this comment? When I think about it, it seems to me that the aggregate of all active managers *is* the market. Some over-perform and some underperform.

Thanks William.

You are right, but in practice, it’s not just active managers influencing the market / setting asset prices.

There are quant funds, high-frequency players, and yes, those naughty insider traders as well: https://bankeronfire.com/the-people-who-beat-the-stock-market

The bottom line is that if there was just one active manager in the world, they would have no issue beating “the market”. But given there are millions out there, price efficiency is pretty high.

The sweet spot for active management is somewhere in the middle, where you make enough money to offset the fees you are charging.

Great read. One thing has confused me and I still don’t really know the answer is to do with price discovery. Active managers help find the market price of a share and then passive investors just follow. So as there becomes fewer and fewer active investors, price discovery becomes more difficult. Then we assume there’s no active investors whatsoever, what happens then? How do prices get discovered?

If there is no price discovery whatsoever going on, someone will work out that they have the keys to an enormous arbitrage opportunity, and lo and behold, I’d expect the issue to work itself out rather quickly.

You beat me to it.

That’s exactly it. With no active managers, asset prices would get disconnected from fundamentals very quickly, presenting a tremendous money-making opportunity for active managers.

I’ve written about it in detail here: https://bankeronfire.com/falling-in-love-with-active-investing

I did a similar bit of my own (informal and amateur) research about the ‘index fund bubble’ earlier in the year funnily enough. It appears that theories and speculation stems from an analysis written by Michael Burry (The Big Short anyone?).

Cue investment “gurus” and the wider “press” spinning a web and, in my opinion, misinterpreting (and potentially misrepresenting) the basis of Burry’s findings.

It makes interesting reading, much of it beyond my level of understanding, but one point I did look into was the the makeup of funds – namely ETFs. A primary concern appears to be based on synthetic ETFs, rather than those to which you allude above – physical ETFs.

The makeup of synthetic ETFs show worrying similarities to the CDOs that were arguably a large part of the 2008-09 crisis. From my understanding, they’re not asset backed and exist in this “second market” space – as did the packaged CDOs. This has many complicated effects, not least the possibility of inflated or unsustainable valuations.

My knowledge starts to fade at this point and I’ve likely vastly oversimplified, but I get the gist – I did more reading and gave myself an idea of what to look out for. Thankfully synthetic ETFs are less prevelant (especially on UK markets I believe) than physical ETFs, but they still exist.

The conclusion I reached was fairly simple. Funds which are physically backed (i.e. Those that own the actual asset they track) are as safe as that fund’s criteria (whether it tracks an index, an industry, a commodity, or whatever else). Fund criteria is a discussion for another day but the more specific the greater the risk, I suppose.

Even if it’s not the right conclusion, it feels far safer for me as an amateur DIY investor than existing in an investment space that is made up of financial instruments and derivatives that only experts and institutions utilise and understand.

I agree with your post entirely, BOF, and although there might be an argument for those concerns, they exist in isolation within a tiny proportion of the fund market – which as you’ve said, is still less than the active fund market.

If nothing else, it hammered home the point of “DYOR” – the devil really is in the detail.

I think that is indeed the point Burry was trying to make.

When you get to secondary and tertiary bets on underlying physical ETFs, you are quickly finding yourself in a situation that amplifies volatility, much like the CDOs did in the lead-up to the financial crisis.

And while volatility is bad, it doesn’t need to decimate your returns – as long as you are willing to ride it out.

However, many folks have instantly picked up on Burry’s arguments as a way to sell their crappy active products to anyone who will listen.

BoF – thanks for your excellent write up. As always you write some very interesting points/commentary. Out of interest though I assume your favourable comments for passive investing versus say buying direct shareholding in individual companies (which I assume given your day job you would be more than skilled at doing) is based on risk management principles or is this also reflecting your personal circumstances i.e I assume you may have to comply with some compliance guidelines which make it difficult, or at least delay buying equities? Also, could the case be made in certain circumstances to buy some actively managed funds in certain circumstances – for example Investment Trusts (not OEIC’s) trading on a discount with a reasonable fee level etc?

Thanks for the kind words.

It’s true that I am not exactly at liberty to buy individual stocks at the moment.

By way of my job, I have a ton of price-sensitive information and while my employer has a pre-clearance process I can follow, I choose not to take any risk and thus don’t trade individual stocks.

That being said, I simply don’t see myself buying individual stocks / active funds even after I leave investment banking behind. Fundamentally, there is too much evidence that shows active investing over long periods of time underperforms passive (not least due to fees). Nothing personal, just business.

as far as buying ITs at a discount – my (somewhat simplistic) view is that the market always knows something we don’t. There may be situations driven by mispricings, but there’s always a risk with fundamental value.

Hi BoF

I’m not sure you’ve got this but quite right:

“ When the price of an asset goes up, its relative weight in the index also goes up – at the expense of other index constituents.

Given index funds look to replicate the weightings of the benchmark index, they would buy more of the appreciating asset and sell a little of all other assets.”

The index doesn’t buy more of a constituent if it goes up in value and sell a little of all other constituents. The change in value of those constituents just means you own more / less of each. The whole point is that the passive fund just buys the constituents at the time and that’s it. There is very little trading / turnover of the portfolio. There will be a little turnover for changes in constituents of index as shares get added or removed, but this will be small.

However, perhaps the point you were trying to make is that if you are buying a passive fund then you will be buying more of those constituents that make up a larger weight (which may have recently gone up in value) and less of those which may have just gone down in value (as they will reflect a lower weight). But again, the whole point of passive investing is that you just take the market price as being the right price to pay. You have no knowing of which stocks will go up or down.

Thanks James. You are spot on and have explained it much better than I did!

As you suggest, point I was trying to make is that as a price of an asset goes up (relative to other assets), it’s weighting in the index also goes up. Thus, when you buy the index fund, you end up getting more of said asset and so forth.

Those who have bought the index fund previously end up owning the same stocks, but their prices will have changed.

Another great post BoF!

The data clearly indicates that passive investing is the right strategy for almost all investors. S&P puts out annual active vs passive scorecards that show 90% of active funds underperform passive funds, excellently summarized by Larry Swedroe here: https://www.advisorperspectives.com/articles/2019/11/18/the-surprising-results-from-s-ps-latest-spiva-analysis

At some point, as passive funds continue to see massive inflows, there will likely be an equilibrium between passive and active managers. However, I’d be surprised if we get there in my lifetime.

Thanks MM!

Given the velocity of flows into passive vehicles, I actually think we might get to an “equilibrium point” at some point over the next decade.

Once we do get there, I suspect that it will take some convincing (and time) for the majority of investors to start believing in active investing again.