If you have read this and this then you know that contributing to a workplace pension scheme is one of my favourite wealth-building strategies.

I have been focused on growing my pension pot for the better part of the past decade. As a result of those efforts, the Banker on FIRE household pension value now stands at about £230k.

Having changed employers and pension providers many times, I consider myself reasonably well-versed on this topic. Today, I wanted to share some of my favourite pension hacks that can help you maximize your pension pot value ASAP.

If you google it, 99% of the advice that you get on this topic will say something like: “you need to maximize your contributions and take advantage of employer matching”.

Well – thanks for telling me something I didn’t already know! There goes another five minutes of my life I will never get back.

If you are serious about using pensions to grow your net worth, you need to have a strategy that allows you to multiply the value of every pound you contribute into your workplace pension.

Listed below are simple hacks you could take advantage of today to get even more oomph out of the pension contributions you’ve been making. But first, a quick reminder of why pensions are an important wealth-building tool.

Do You Want To Be Rich? Then Pay Attention To Your Pension!

If you still aren’t convinced that contributing to a workplace pension scheme is a good idea, then consider the following: in the UK, there is a strong linear relationship between the size of your pension pot and your household wealth.

Take a look at the table below. As you go up the spectrum of wealth distribution, you will see that pension values account for an ever-increasing share of household net worth.

At the very top of the range, pensions account for ~55% of total household net worth.

Now, there are three ways to interpret the data.

The most obvious one is that contributing to a pension is key to working your way up the spectrum of wealth distribution.

A second interpretation could be that the older generation has been able to realize an outsize benefit from defined benefit schemes. Of course, this is now primarily a thing of the past. If you have one of those pensions, consider yourself lucky.

A third, more cynical read, is that the wealthy have been better than everyone else at exploiting all the benefits a pension can provide.

Regardless of which line of thinking you choose to follow, one conclusion holds no matter what: if you want to be wealthy, you need to understand how to maximize your pension value.

Five Easy Ways To Maximize Your Pension Value

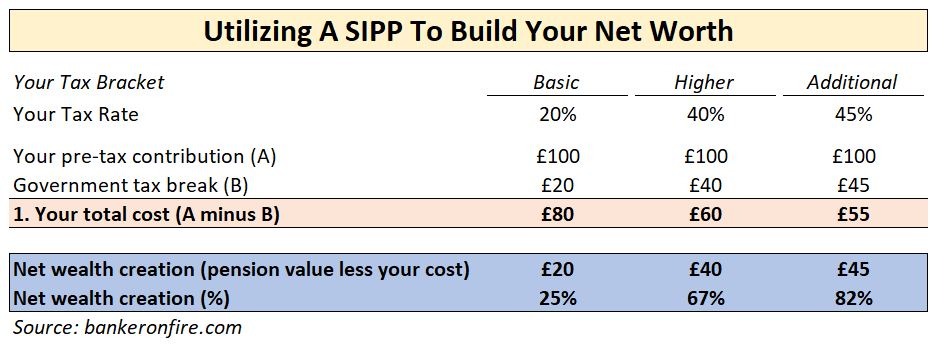

1. Take Advantage of SIPPs (Self Invested Personal Pensions)

Thankfully, workplace pensions are now the norm. However, not having access to a workplace pension scheme doesn’t mean you need to lose out on pension tax benefits. Opening a SIPP with a provider like Hargreaves Lansdown or AJ Bell allows you to take full advantage of tax relief on your pension contributions.

Note that if you do have a workplace pension scheme, you are ALWAYS better off using it for the initial contributions so that you can take advantage of employer matching.

More importantly, you can – and should – utilize a SIPP even if you have a workplace pension.

Most people don’t know that once you have taken advantage of your employer’s contributions, you can transfer a part of your pension pot to a SIPP. This will enable you to invest in a wider range of funds with better returns and lower fees.

I did a post recently about transferring an old workplace pension into a SIPP in order to maximize my long term returns. Just make sure you don’t lose any valuable perks when you do. Give your pension provider a call to find out whether that applies.

2. Get A Cash Bonus For Transferring Your Pension

Some SIPP providers will pay you a cash bonus for transferring your pension pot to them. As an example, Hargreaves Lansdown ran an offer recently where you could get anywhere between £50 – £500 (depending on the value of your pot) for transferring in your pension.

These offers aren’t on all the time, so you will need to keep your eyes open for them. Running out of time to take advantage of the offer? No problem – if you email the pension provider they will likely extend the offer for you. HL did this for me last year by giving me a six-month extension.

To keep the cash bonus, you will likely need to keep your pension pot with the new provider for at least 12 months.

Of course, once the time is up there’s nothing to stop you from moving your pension pot to a new provider again – and cashing in yet another bonus. Assuming you’ve got a large enough pension pot and are willing to move it around, you can generate an extra £10k+ over a twenty-year period.

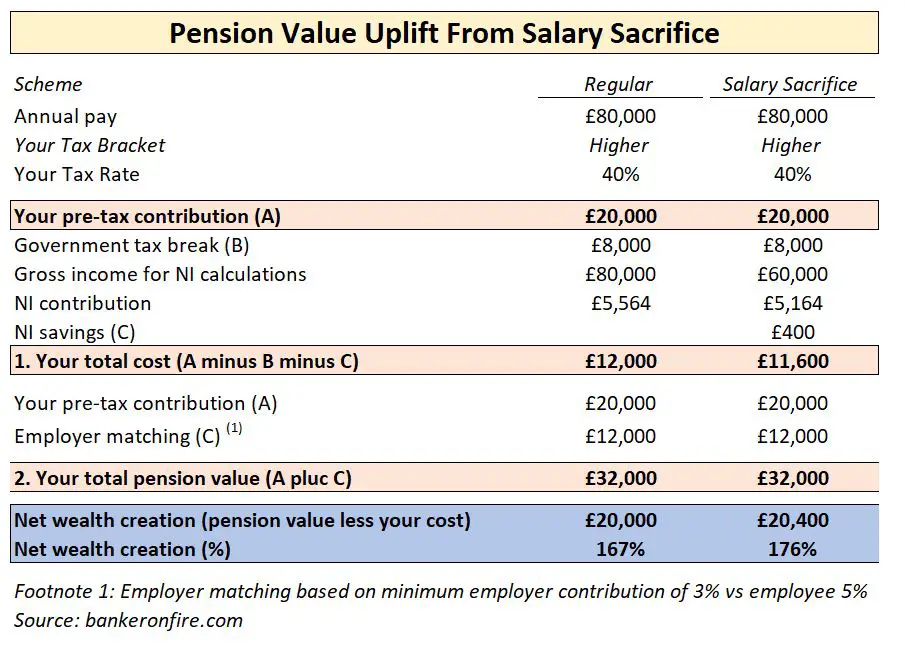

3. Check If Your Company Offers Salary Sacrifice

At its most basic level, salary sacrifice works by reducing your gross earnings on which income tax and NI contributions apply.

For example, if you are making £80k/year and contribute £20k/year into your pension through salary sacrifice, your gross earnings for NI purposes will actually be £60k (£80k annual pay less £20k pension contribution).

This equates to a £400 reduction in your annual NI bill. As a result, for every pound you put in your pension scheme, you get an additional uplift of 9% or 9 pence.

This isn’t easy to follow so see below for a worked example.

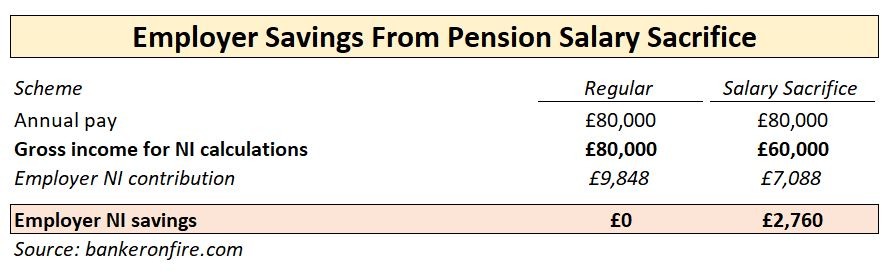

4. Ask If Your Employer Passes On Their Own NI Savings

In addition to the NI contributions that come out of your pay, your employer also makes NI contributions on your behalf. If your gross pay reduces through a salary sacrifice scheme, your employer will also save money.

While there is absolutely no requirement to do so, some companies choose to pass this saving on to employees.

Using an example above, an employer would save £2,760/year in NI contributions – and pass those savings to you.

5. Don’t Forget That You Could Also Be The Employer

This isn’t exactly a way to increase the value of your own pension pot. Instead, it’s a way to protect your own bottom line if you happen to be an employer in addition to being an employee.

In April 2019, the pension auto-enrolment minimum has been increased to 8%: 5% by the employee and 3% by the employer.

However, for those on net pay agreements, the entire 8% pension contribution is typically borne by the employer. If your employee negotiated a contract whereby she is paid £12/hour, she expects to receive that pay, regardless of any changes in pension regulations.

One category of employees who are often on net pay agreements are nannies, so you need to be mindful of their pension contributions.

Take a look at an example below to see how you could be out of pocket.

Assume you hire a nanny to work 8 hours a day, 5 days a week, 52 weeks a year and pay her £12/hour net (standard going rate in central London at the moment).

Your nanny’s net annual pay will be £24,960. As those of us who employ nannies on net pay arrangements know well, the cost to you as an employer is going to be much higher. You need to pay about £37k/year in order for your nanny to receive £25k/year net of tax.

All of a sudden, your £12/hour nanny become a £17.8/hour nanny. And of the £12k extra cost, about £1.9k/year is due to pension contributions you are liable for. On an hourly basis, the pension payments account for about 90 pence of extra cost.

For the avoidance of doubt, I think contributing to your employee’s pension schemes is absolutely the right thing to do. Just make sure that you are aware of your responsibilities and understand the amounts involved in order to ensure it doesn’t become an unpleasant surprise.

So here you have it – five easy hacks to make sure you get the maximum value for your pension contributions – and give a fair shake to your own employees.

Want To Get Even More Pension Value?

Are you wondering whether there are any other ways of hacking your way to pension wealth?

Well, if you are married, or are in a civil partnership, there is indeed much more you can do to get more out of your workplace pension. Then take a look at Part Two: More Easy Hacks To Maximize Your Pension Pot

About Banker On Fire

Enjoyed this post?

Then you may want to sign up for our exclusive updates, delivered straight to your inbox.

You can also follow me on Twitter or Facebook, or share the post using the buttons above.

Banker On FIRE is an M&A (mergers and acquisitions) investment banker. I am passionate about capital markets, behavioural economics, financial independence, and living the best life possible.

Find out more about me and this blog here.

If you are new to investing, here is a good place to start.

For advertising opportunities, please send an email to bankeronfire at gmail dot com

Very interesting chart on pensions and household net worth. A young person in the UK is going to put priority on buying a house, and pensions are increasingly being neglected. You often hear people saying “my house is my pension”.

I was also surprised to see pensions account for such a high proportion of household net worth.

It’s even more striking because house prices back in 2017 (which is when this data was collected) were pretty close to all time high.

Then again, it’s tough to beat wealth creation through pensions when you automatically get a ~175% uplift on your investment and it grows tax free for the next 30 odd years.

I find workplace pensions confusing. I’m a higher rate tax payer. I’ve increased my pension contributions so that I’m now putting 20k a year in – does the 40k annual limit include the employer contributions and NI benefit I’d be betting on top of that? If I want to use any unused carry forward allowance from last year do I need to complete a self assessment form or any other documentation to claim this cary forward?

I wish pensions were clearer! I’m not in finance and am trying to get more clued up on personal finance. Your blog is the reason I increased my contributions!! So thank you very much for all you do.

Thanks for the kind words!

It’s quite confusing indeed. Let me give this a shot.

The 40k limit is the sum of your contributions AND your employer’s match.

Income tax / NI breaks aren’t included so in effect the 40k is a gross number (ie even if there was no employer match your net contribution would always be lower due to the tax break).

As far as your second question – when my allowance got tapered down to 10k a few years ago I simply figured out how much carryover room I had and contributed that amount. Didn’t fill out any forms.

Hargreaves Lansdown has a nifty calculator that helps you work out the carryover allowance. Let me know if you cannot find it and I’ll dig up a link.

Clearly this isn’t professional advice but hopefully a helpful steer.

Thank you so much – very helpful. Will check out the HL calculator Many thanks!